Reiterates Belief That Shareholder Representatives are Needed on Repay's Board to Rectify Governance Shortcomings

Notes KUBRA Already Appears to be Underperforming Initial Expectations based on June 1, 2026, Guidance relative to the March 31, 2026, Deal Announcement Update Call

DALLAS, TX / ACCESS Newswire / June 4, 2026 / Veradace Partners L.P., collectively with its affiliates, a significant shareholder of Repay Holdings Corporation (Nasdaq:RPAY) (the "Company") with beneficial ownership of 8.2% of the outstanding Class A Shares, issued an open letter to the Company's shareholders.

The full text of the letter is set forth below:

Fellow Repay Shareholders,

Veradace Partners L.P. (collectively with its affiliates, "Veradace" or "we") is profoundly disappointed in the unwillingness demonstrated by Repay Holdings Corporation ("Repay" or the "Company") to work constructively with its shareholders to improve its governance and explore alternatives to the KUBRA acquisition. In light of the failure of Repay's board of directors (the "Board") to engage with our nomination in any meaningful way, we have withdrawn our nomination of candidates to the Board at the Company's 2026 annual meeting of stockholders (the "Annual Meeting"). We continue to believe urgent changes to the governance of the Company are necessary to prevent the further destruction of shareholder value, and to make this clear to the Board, we intend to WITHHOLD our votes from all current members of the Board at the Annual Meeting.

Our decision to WITHHOLD is not made lightly, but recent events, including the Board's rejection of Forager Capital's $4.80 per share acquisition proposal as "significantly undervaluing" Repay, have led us to conclude that we cannot in good conscience vote for any member of the Board. A board that refuses to entertain discussions with a potential buyer offering a substantial premium seems like bad governance to us. Consider that in the 12 days following the KUBRA announcement, 21.8mm, or 25% of the outstanding Class A common stock, traded for an average price of $2.69 with a high of $3.29. On the day of the Forager proposal, 25.1mm shares, or 29.2% of the outstanding, traded and closed at $4.11. Over 50% of the Class A common stock changed hands at significantly lower prices that the Forager proposal - shareholders are voting with their feet and selling shares.

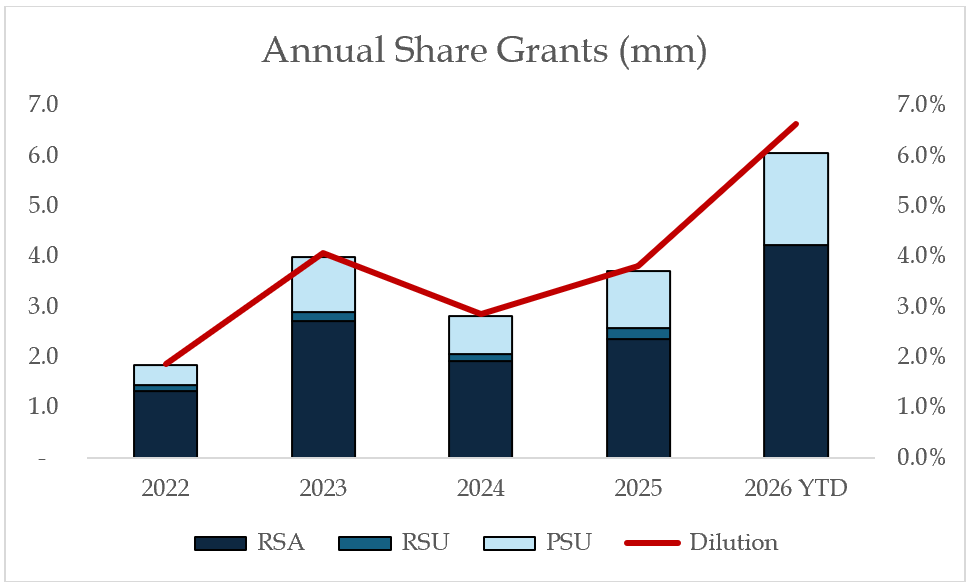

Further, a board that claims that a $4.80 offer significantly undervalues the company yet doubles the amount of dilution they grant to management at a stock price of $2.84 seems to us like a board that has complete disregarded its fiduciary duty. In Q1 2026 the Board granted employees 6.1mm shares or 6.7% of the Class A and Class V shares outstanding. This is more than double the trailing 4-year average dilution of 3.2% and comes after 19.3mm of shares (a whopping 27%) voted "no" in last year's "Say-on-Pay" vote. The majority of the grants are Restricted Stock Awards, not performance based, granted at a weighted average price of $2.84. The Company's proxy statement for the Annual Meeting claims the Board has received and responded to significant shareholder feedback regarding better alignment between pay and performance, but what we've seen suggests the opposite. Apparently the Board believes that doubling dilution to compensate management is the sort of pay structure that is aligned with a 52% decline in share price in 2025 and the first revenue decline year in company history.

Incredibly, while the ink is still wet on the KUBRA acquisition Repay already appears to be lowering expectations. Repay's updated guidance, issued on June 1, 2026, suggests an EBITDA contribution in 2026 of $27.5 to $30.0mm from KUBRA for the final 7 months of 2026.1 This suggests $47.1 to $51.4mm annualized over 12 months inclusive of 2026 synergies. On the KUBRA announcement call on March 31, 2026, management responded to an analyst question on growth suggesting growth in the "mid-single digit range." But that's not what the new guidance indicates:

The $47.1mm low end of KUBRA implied annualized EBITDA guidance is below the $49mm EBITDA KUBRA produced in 2025

The $51.4mm high end of KUBRA implied annualized EBITDA guidance is below the $51.5mm EBITDA one would expect with a 5% growth rate on 2025 EBITDA.

This range already includes an expected $8mm in run-rate expense synergies in 2026

Apparently, in the 3 months since the deal was announced, at which time the Board and management vigorously defended it, KUBRA has gone from an industry growth business to a no-growth to declining asset.

We are deeply concerned the current Board is not looking after shareholders' interests. We believe new, truly independent directors should comprise the majority of Repay's Board. We still hope to constructively engage with the Company to improve governance that appears severely lacking. Until then, we will let our vote speak for itself.

Sincerely,

Alex Vezendan

Founder and Chief Investment Officer

Veradace Capital Management LLC

General Partner of Veradace Partners LP

About Veradace Partners L.P.

Veradace Partners is a concentrated, long-term, public equity investment partnership that seeks to invest in high-quality businesses. Veradace takes a long-term and constructive approach to working with management teams. Veradace has a track record of working with companies to create long-term value.

CONTACT:

Veradace Capital Management

info@veradacecapital.com

1 $27.5-30.0mm implied KUBRA contribution: $168.5-176.0mm updated EBITDA guidance - $141-146mm prior EBITDA guidance

SOURCE: Veradace Capital Management

View the original press release on ACCESS Newswire