Target (TGT) is not operating in an easy retail environment right now. Consumers are still cautious, discretionary spending is uneven, and the company is already trying to rebuild momentum after a rough stretch of sales pressure and activist backlash tied to last year’s DEI rollback. Now, Target is facing another reputational hit. The American Federation of Teachers (AFT) says it wants its 1.8 million members to avoid Target for back-to-school shopping, a move aimed at the company’s response to federal immigration enforcement actions in Minneapolis, Minnesota.

That is not automatically a business-altering event, but it does add another layer of noise around a stock that does not need much more of it. The key question for investors is whether this will turn into a real sales problem or just another headline.

Why This Boycott Matters for Target

On one hand, Target is a giant retailer with 2,000 stores, a large online business, and a brand that still has real pull with middle-income shoppers. On the other hand, back-to-school is a meaningful seasonal window, and the union is trying to make the boycott broader by pushing similar resolutions elsewhere.

That matters because Target has already admitted that a prior boycott tied to its DEI shift hurt sales. If this latest effort gains traction, it could land at exactly the wrong time for a turnaround that is still in progress. Markets reacted cautiously to the news, with investors watching closely to see whether it affects traffic during one of the retailer’s key selling seasons.

What Does the Valuation Say About TGT Stock?

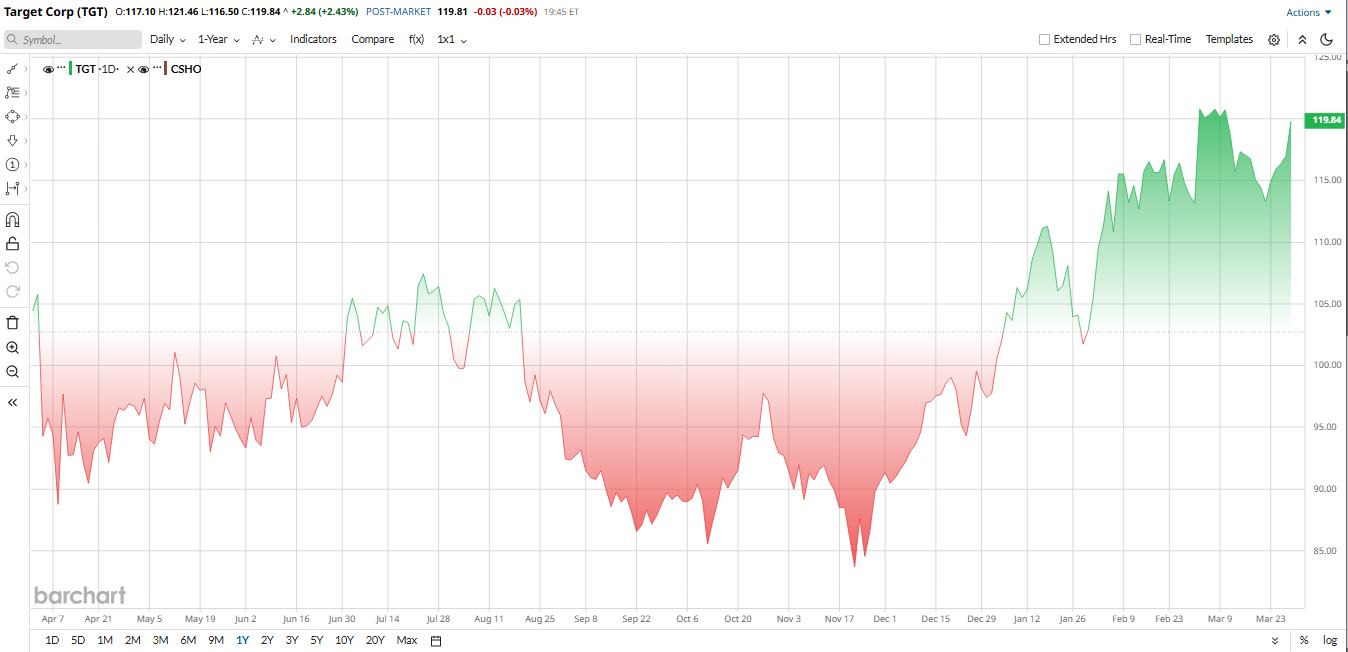

Despite the broader market pressure, TGT stock has soared in 2026, climbing nearly 22% year to date (YTD). These gains have come along with better-than-expected fourth-quarter earnings and a strategic turnaround plan.

From a valuation perspective, Target stock does not look extreme in either direction. Shares currently trade between $115 and $120. Target has a market capitalization of $54.2 billion. TGT stock trades at roughly 15 times trailing earnings, which sits almost in line with the valuation range for many general merchandise retailers. That suggests the market is not treating Target as a high-growth story anymore, but it is also not pricing in a severe collapse.

Target’s Business Is Still Large, But Growth Is Weak

Still, it is important not to overstate the near-term damage. Target’s latest quarter was neither pretty or a collapse. In fiscal Q4 2025, net sales came in at $30.5 billion, down about 1.5% year-over-year (YOY), while comparable sales declined roughly 2.5%. On a full-year basis, revenue slipped 1.7% to $104.8 billion.

That is clearly not the kind of growth investors want to see, but it also shows the business remains very large and capable of generating strong cash flow. Adjusted EPS of $2.44 actually beat expectations, and the company generated $6.56 billion in operating cash flow during the quarter.

In short, Target is still a functioning retail giant with the financial capacity to invest in its turnaround.

Management Is Pushing an Aggressive Turnaround Plan

The more interesting part of the story is what management is doing next. Earlier this year, Target outlined a new growth strategy aimed at resetting the company’s performance.

The plan includes roughly $2 billion in additional investment during 2026. About $1 billion will go toward capital spending, while another $1 billion will be directed into operational improvements. The company has already cut prices on thousands of everyday items and plans to upgrade stores, expand staffing, and deploy more AI tools across its operations. Target also expects to open more than 30 new locations this year “as part of its path to 300 new stores by 2035.”

CEO Michael Fiddelke has described the strategy as a “new chapter” for the retailer, focused on better merchandising, faster fulfillment, and improved in-store execution.

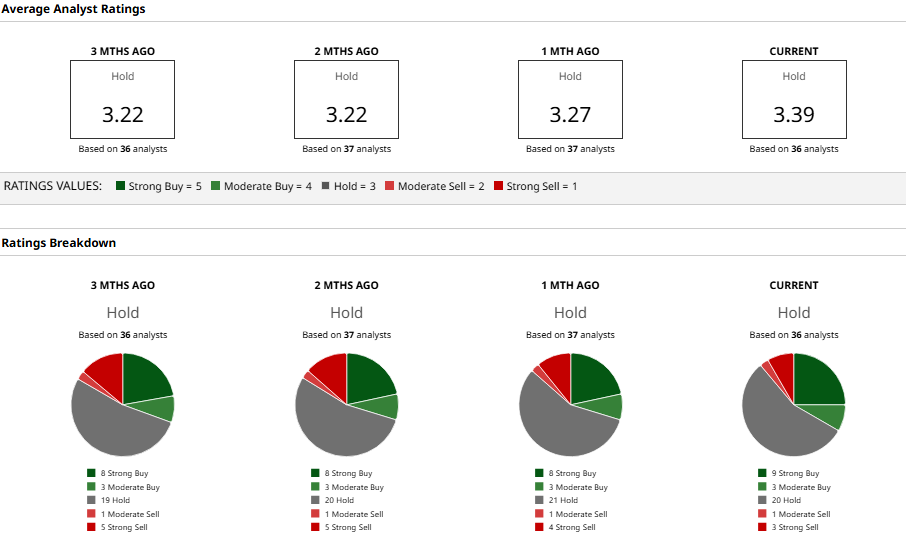

What Do Analysts Think of TGT Stock?

Wall Street is still somewhat divided on Target. Morgan Stanley rates TGT stock as “Overweight" and recently lifted its 12-month price target to $145, saying the company is taking the “right steps” to rebuild its merchandising strength.

Goldman Sachs is more cautious. The firm raised its target to $112 after the Q4 results but kept a “Neutral” rating, noting that TGT stock may already reflect optimism about improving comparable sales while competition and margin pressure remain concerns.

Other analysts are somewhat more upbeat. RBC Capital raised its target to $130, praising Fiddelke’s quick moves, including workforce reductions and a $2 billion reinvestment in merchandising and the supply chain. Wells Fargo also lifted its target to $135 following stronger guidance.

Even so, the overall view is fairly balanced. Target has a consensus “Hold" rating. The mean price target sits at $125.19, which is close to where TGT stock trades today.

In other words, analysts see some potential upside if Target’s turnaround strategy gains traction, but they also believe the company still has a lot to prove.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Apellis Pharma Skyrockets on Biogen Deal. Is It Too Late to Chase APLS Stock?

- Is GameStop Buying Best Buy? And If So, Does That Make GME Stock a Buy?

- Bank of America Is Betting That Billionaires Could Help Take TripAdvisor Stock 50% Higher

- GE Vernova Stock Outlook: Should You Buy the Dip in GEV or Wait?