BP PLC (BP) American Depository Receipts (ADRs) have been rising alongside higher oil and gas prices. As a result, BP call option premiums are now very high, worth shorting by value investors.

For example, a 10% out-of-the-money BP call option now has a 1.3% yield over the next month. This article will show the positive probability of making money with this play.

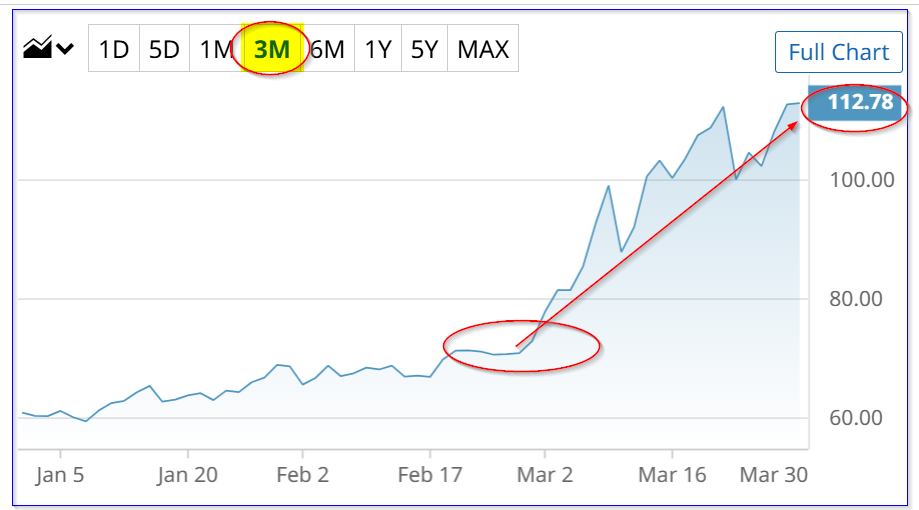

BP closed at $47.35 on Monday, March 30, up +21.85% from $38.86 at the end of February, when the Iran war started. It has tracked Brent crude oil rise, up +54.8% in the last month. The Brent May '26 futures price has risen from $72.87 to $112.78 on March 30.

Both BP stock and Brent May futures are at a peak. But will they stay there?

Target Prices for BP

Investors clearly expect the higher oil prices to benefit BP stock over the next six to nine months.

One problem with this expectation is that prices could quickly drop if the war ends. Perhaps because of that scenario, analysts haven't raised their target prices very much.

For example, Yahoo! Finance reports that the average target price (TP) of 19 analysts is just $42.62. That's well below today's price. Similarly, the Barchart mean survey price is just $41.99.

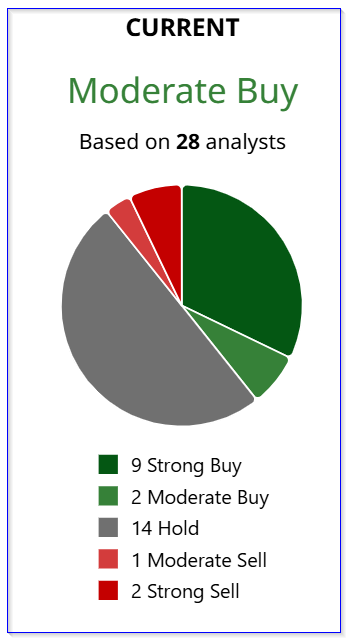

Moreover, Barchart shows that of the 28 analysts covering the stock, only 9 have strong buy recommendations. The rest are moderate buy, hold, or sell recommendations:

That's not really a ringing endorsement for BP stock. As a result, it might make sense, especially for existing shareholders, to consider selling BP shares.

However, there is a way to gain income from these higher BP prices without actually selling shares right away.

By selling covered calls, an investor can make a monthly income by setting a higher price at which they are willing to sell their shares.

This works well if done monthly, as call options tend to fall quickly in their last month. Shorting the one-month expiry call premiums benefits from this time decay phenomenon.

Selling BP Covered Calls

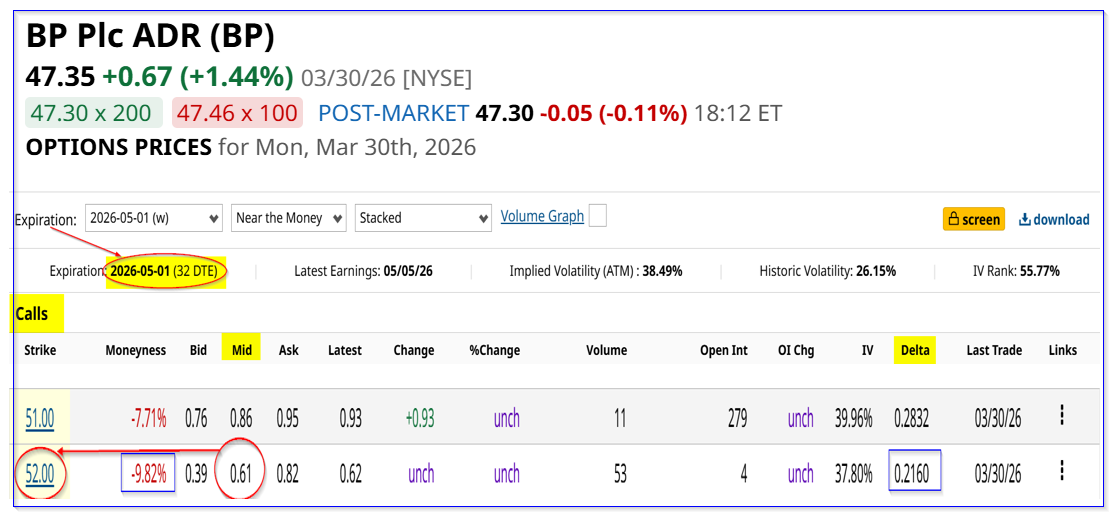

For example, look at the May 1, 2026, expiry BP call option chain. It shows that the $52.00 BP call option contract, which is almost 10% higher than Monday's close (+9.82%), has an attractive midpoint premium of 61 cents.

That means that an investor who buys 100 shares for $4,735 at Monday's closing price can enter an order to “Sell to Open” one call option contract. The account will then receive $61.00.

As a result, the one-month yield to this investor is 1.288%, or almost 1.3% in income ($61/$4,735).

The account is “covered” in case BP rises 9.82% to $52.00 or higher on or before May 1, as the 100 shares in the account will be assigned to be sold at $52.00.

As a result, if an investor can repeat this play each month for the next three months, the investor could accumulate $183. That works out to 3.87% yield over 3 months:

$183/$4,735 = 0.03865

Note, as well, that the delta ratio of 0.216 is very low. It implies there is less than a 22% chance BP will rise to $52.00 in the next month. In other words, the investor may not have to sell their shares at $52.00 and can keep the income.

Moreover, even if BP rises to $52.00, the capital gain accrues to the covered call investor. So, the total potential return over the next month is over 11%:

+9.82% + 1.288% = 0.111 = 11.1% total potential return

However, there are some potential risks as well. However, the risk/reward ratio seems favorable.

Risks and Ways to Mitigate Them

The greatest risk is that an investor buys BP shares at today's price and then the price of oil falls, taking BP along with it.

One way to mitigate this risk is to use the covered call income to buy out-of-the-money (OTM) puts. The problem is that there are wide spreads at lower priced put strike prices.

It's potentially possible to buy a $39.00 put strike price for 51 cents. That would leave a net credit spread income of just 10 cents (i.e., $0.61-$0.51). This lowers the one-month yield to just 0.21% (i.e., $10/$4,735 = 0.0021).

Moreover, an investor could watch and determine if the put purchase could be sold closer to expiration. If it appears the put strike price will remain below the spot price, the investor could redeem some of the original short income by selling the put.

Another way to mitigate the risk is to repeat this trade over a period of months. The accumulated income provides some downside risk. For example, if an investor can collect $1.83 over 3 months, the breakeven price lowers to $45.52:

$47.35 - $1.83 = $45.52, or 3.86% lower

A third way to mitigate the downside risk is to do a rollover trade at a lower call option strike price.

Let's say BP falls to $45.00. The premium might fall to $40 cents, and the investor could then enter an order to “Buy to Close” the covered call play. Then the investor might enter a new order to sell calls at $49.00 for 60 cents again.

The play would still be about 8% out-of-the-money (i.e., $45/$49 =-0.0816), and the premium collected might be 20 cents from the first trade and 60 cents in the second trade.

That works out to a gain of 1.689% (i.e., $0.80/$47.35). However, there would also be an unrealized capital loss of $2.35 ($47.35-$45.00), or -4.96%. So, the next return is -3.27%.

But think of it this way. Without selling the covered calls, the investor might be much worse off with a 5% loss. And the investor would still own the BP shares, allowing for future covered call plays to make up the unrealized loss.

Probability and Expected Return

Let's say there is a 70% chance of making income over the next month with a covered call play (i.e., a 1.288% income) and a flat BP price. Note that this is lower than the implied risk from the delta ratio (i.e., 1-0.216 = 78.4%).

Conversely, let's assume a 25% chance of a net 3.27% loss using the third mitigation play above. The net expected return is therefore positive. Here's why:

0.75 x 0.01288 = 0.00966 = 0.966%

0.25 x -0.0327 = -0.008175 = -0.8175%

0.996% - 0.8175% = 0.1485% (i.e., a positive return)

This shows that, on balance, there is a good likelihood of making money shorting 10% out-of-the-money covered calls, using probability analysis, and a mitigation strategy.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- A ‘Golden’ Way to Trade the Volatility in Gold Prices for Low Risk, High Reward

- Huge, Unusual Put Action in Robinhood Stock - A Sign That HOOD Has Bottomed?

- Bath & Body Works Jumps 11% Monday — Should You Make an Aggressive Buy to Bet on a BBWI Stock Rebound?

- Nvidia (NVDA) Stock’s Discount Could Get Even More Attractive for Patient Speculators