Here’s a quick test to see if you act your age: Explain the “4% Rule” in investing.

If you are a Baby Boomer or Generation X member, you have probably heard of the gold standard for retirement planning. Specifically, that if you withdraw 4% of your initial portfolio value and adjust for inflation each year, your money should last 30 years.

For decades, this was a theory built on a volatile 60/40 mix of stocks and bonds. But as I write this in late March 2026, the bond market is offering a rare gift that turns this rule from a statistical hope into a mathematical near-certainty, at least on a pre-tax basis.

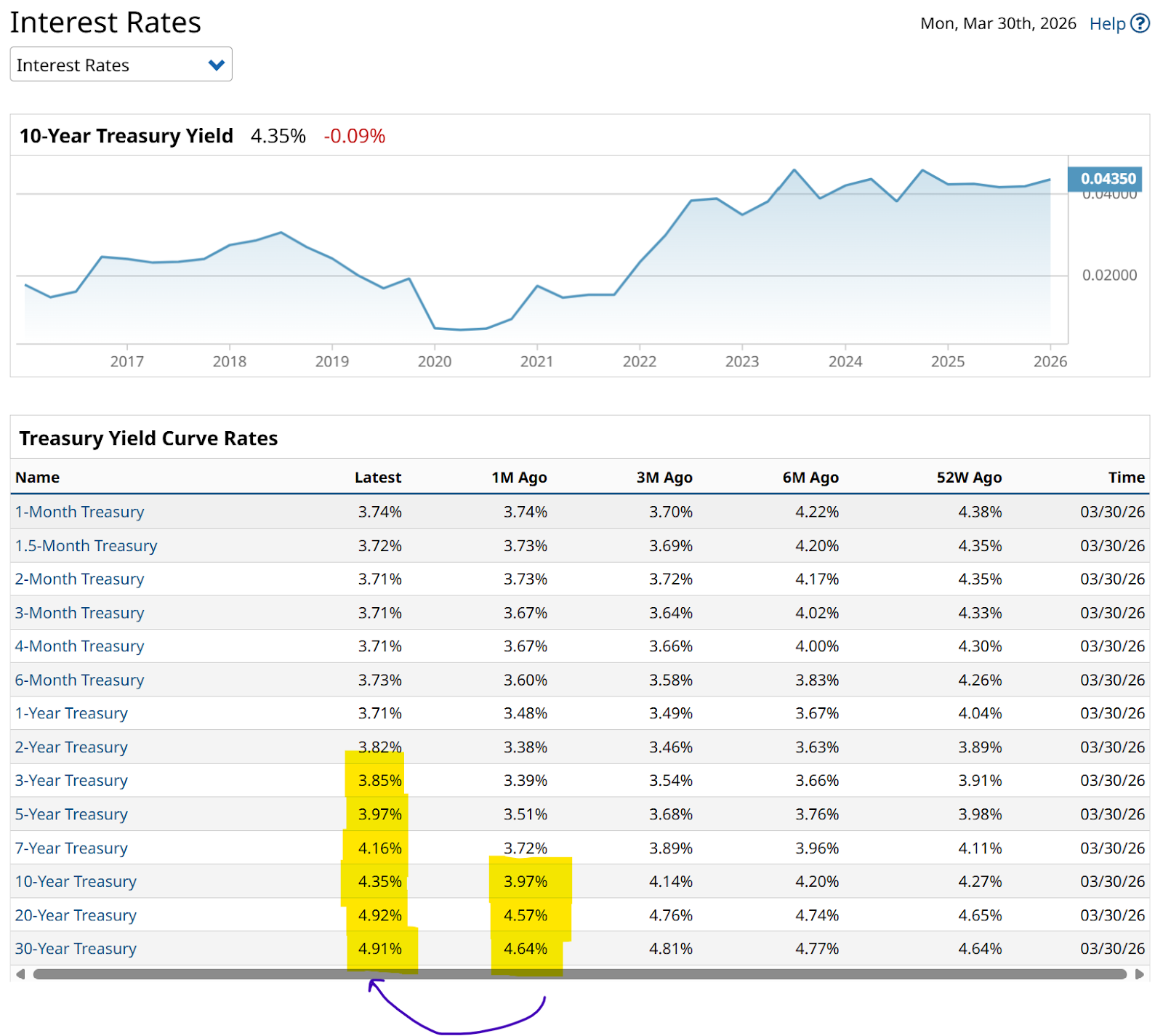

Here’s the yield curve and rate tables for Treasuries as of Monday’s market close. I see a lot more yellow now than just a month ago.

Instead of having to reach out 10 years to get that “magic” 4% yield, 3 years gets you in the neighborhood.

Another way to think about it is to blend different parts of the curve, known as a “bond ladder.” For instance, owning bonds maturing annually from 10-20 years to maturity would land your portfolio’s yield in the 4.65% range. A month ago it was closer to 4.25%.

With these rates, the 4% rule is effectively daring you to stop over-complicating your life and look at a pure fixed-income solution. Not as the whole portfolio, but for at least a larger share. I am living proof of that. My biggest account is not invested in stocks or ETFs. It’s a zero coupon Treasury Bond ladder. With active interest rate hedging.

How Long Does a 4% Treasury Yield Fund a Retirement?

When you can lock in a 4%-5% yield on a 10-year or 20-year Treasury, the math of retirement changes. In the traditional 4% rule, you were forced to own stocks to generate the growth needed to offset the years when bonds paid almost nothing.

Today, the yield alone covers the withdrawal. If you invest $1 million dollars into these Treasuries, they generate $44,000 dollars in annual interest. If your goal is a 4% withdrawal, or $40,000, you are actually earning more than you are spending without ever touching your principal.

Under this scenario, your retirement funds do not just last for 30 years; they theoretically last forever, provided inflation does not outpace your excess yield.

The reason this strategy is a dare rather than a consensus is the fear of the unknown. While 4.4% percent sounds like a dream compared to the 1% percent yields of the last decade, it comes with a catch. Inflation in 2026 remains sticky near 3% percent due to the ongoing energy shocks in the Strait of Hormuz and rising fiscal deficits.

If inflation averages 4% percent over the next decade, your real return on those Treasuries drops to zero. Your purchasing power would erode even while your account balance stays the same.

That notable risk aside, the dare is simple: Can you ignore the siren song of AI hype long enough to accept a guaranteed 4% return that could fund your lifestyle for the rest of your life?

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob's written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- The Bond Market Is Flashing a Warning. Most Investors Aren’t Watching.

- This Investing Strategy Dares You to Ignore the Siren Song of AI and Accepted a Guaranteed 4% Yield for Life

- There Is No Housing Shortage: What Legendary Investor Michael Burry Really Thinks Is Wrong with the U.S. Housing Market

- Stock Index Futures Rally on Prospect of End to Middle East Conflict, U.S. Economic Data and Fed Speak in Focus