GE Aerospace (GE) will release its first-quarter 2026 financial results on Tuesday, April 21. Analysts are bullish on GE stock ahead of the earnings release. The bullish sentiment reflects the company’s strong operational momentum entering 2026, supported by sustained demand for aircraft engines and high-margin aftermarket services.

GE manufactures airplane engines and provides long-term maintenance and service agreements, generating recurring revenue. It is benefitting from a recovering commercial aviation market and stable defense demand. The company’s installed base is extensive. Its engines power roughly 50,000 commercial passenger aircraft and approximately 30,000 military planes worldwide. This large fleet supports a substantial aftermarket services business, which generates higher margins and durable cash flows throughout the life cycle of an aircraft engine.

GE delivered a strong performance in 2025. Total orders surged 32% year-over-year (YoY), driven by a 27% increase in commercial services orders and a 48% jump in equipment orders. Revenue rose 21%, reflecting a 26% expansion in commercial services alongside higher deliveries across both commercial and defense segments. This combination of strong demand and operational execution translated into significant profitability gains.

Operating profit increased 25% to $9.1 billion, while operating margins expanded by 70 basis points to 21.4%. The margin improvement was largely driven by increased volume and pricing in the commercial services business. GE’s earnings per share (EPS) climbed 38% to $6.37.

Given the solid operating momentum, GE Aerospace is likely to report strong growth in the first quarter.

GE Q1: Here’s What to Expect

GE Aerospace could deliver strong quarterly numbers. A large installed base of aircraft engines and strong demand across both commercial aviation and defense markets will support its growth. Its backlog has climbed to roughly $190 billion, up nearly $20 billion YoY, providing a solid base for revenue growth.

The company’s Commercial Engines & Services (CES) will likely deliver solid growth, led by higher deliveries and increased services revenue. Demand within the Defense & Propulsion Technologies (DPT) segment remains solid, supported by strong government spending and ongoing military aircraft programs. Higher engine volumes and improved pricing dynamics in defense contracts are expected to contribute to steady revenue growth.

Profitability trends also appear favorable heading into the quarter. Increased service activity, pricing strength in aftermarket parts, and a favorable revenue mix are likely to support margin expansion. However, management’s ongoing investments may temper margin improvement in the near term.

GE Aerospace has a solid record of outperforming expectations. The company has delivered earnings beats in each of the past four quarters, including a notable upside surprise of roughly 9% in the fourth quarter of 2025.

Wall Street currently expects first-quarter earnings of approximately $1.63 per share, representing YoY growth of about 9.4%. With commercial aviation demand continuing to recover and defense programs providing reliable support, GE Aerospace appears positioned to deliver another solid quarter.

Is GE Stock a Buy?

GE Aerospace is likely to deliver strong Q1 results, supported by robust demand, higher orders, and a larger backlog. The company’s performance continues to be anchored by its large global installed base of aircraft engines, which generates recurring revenue.

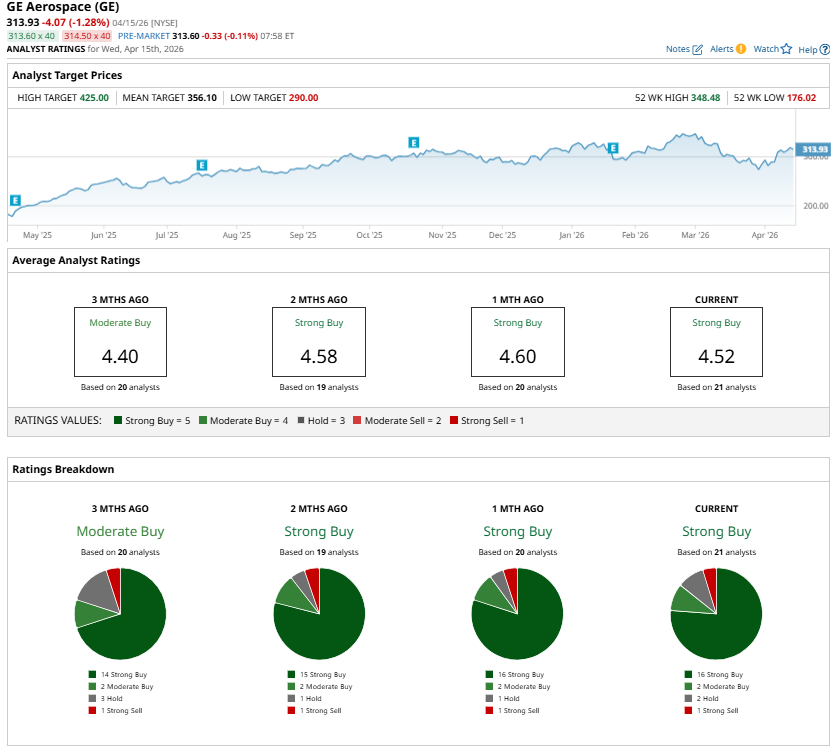

Wall Street currently assigns the stock a “Strong Buy” consensus rating heading into the company’s first-quarter earnings release. Analysts expect continued strength in services revenue, expanding margins, and stable demand.

However, GE stock’s valuation remains a concern. GE trades at a forward price-to-earnings ratio of approximately 41.95, which is high and suggests the positives are already priced into the stock.

Historical trading patterns also warrant caution. The stock has declined following earnings releases in three of the past four quarters.

Overall, while GE Aerospace remains fundamentally well-positioned within the aviation industry, the current valuation suggests a more cautious approach may be appropriate. Investors could benefit from waiting for a more attractive entry point that offers a better risk-reward.

On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart