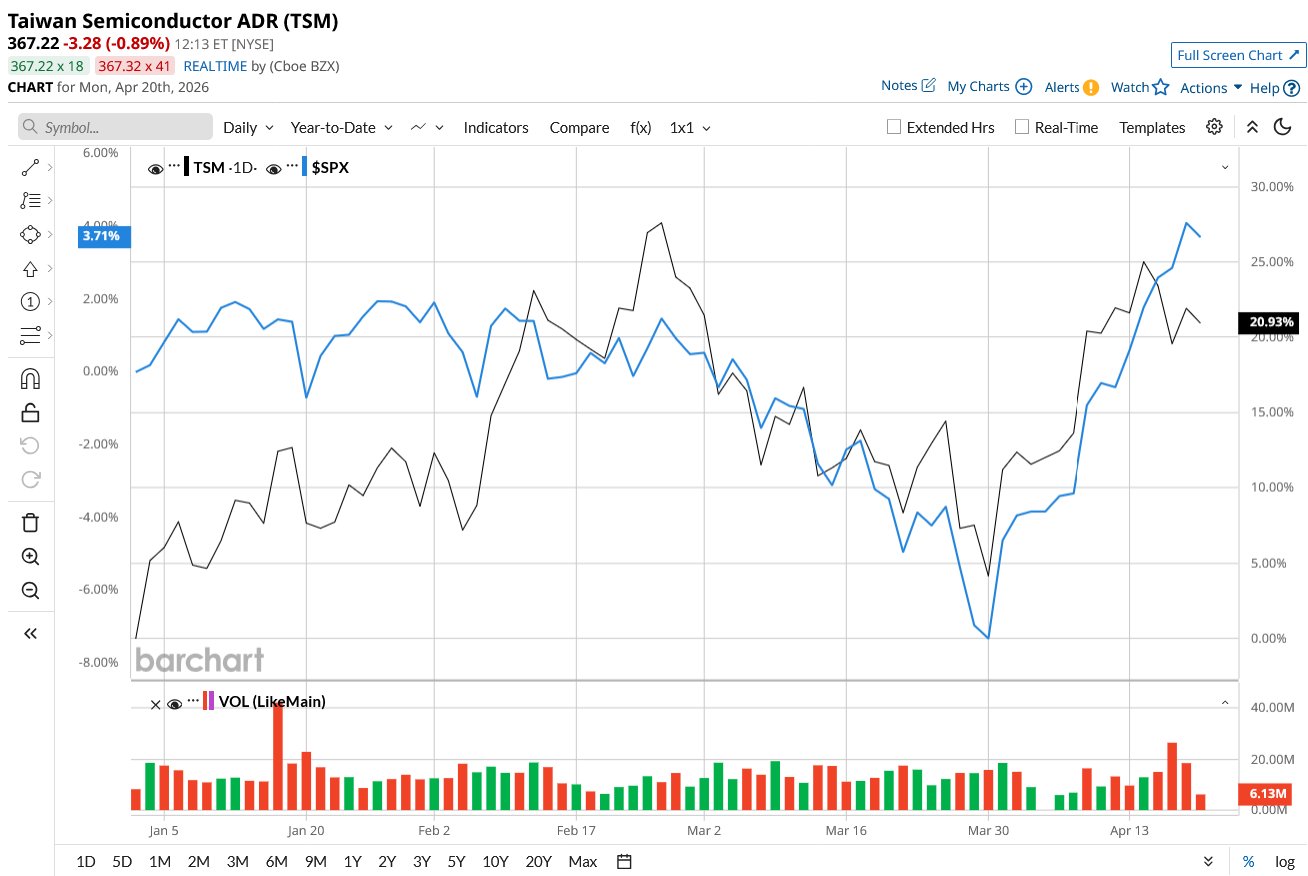

In a market still grappling with macro uncertainty, Taiwan Semiconductor Manufacturing Company's (TSM) Q1 report indicated that the company is strong enough to outweigh cyclical weakness elsewhere. TSMC delivered a powerful start to 2026, reminding investors why it sits at the heart of the global semiconductor ecosystem. TSM stock is up roughly 21% year-to-date (YTD) and 142% over the past 52 weeks, outperforming the broader market gain of 4% YTD.

Let’s dig into its Q1 earnings to determine three reasons that make TSM stock a buy now.

AI Demand Is Fueling a Multi-Year Growth Cycle

The sheer strength of AI-driven demand, along with TSMC's dominant position in advanced chip manufacturing, led to a strong start to 2026. The transition from generative AI to more complex "agentic AI" systems is significantly increasing processing demands. This, in turn, is driving demand for advanced chips. As AI models grow larger and more sophisticated, the need for cutting-edge nodes like 3nm and upcoming 2nm technologies will only intensify, precisely where TSMC dominates.

High-performance computing, which includes AI workloads, surged 20% sequentially in Q1. It now accounts for 61% of total revenue, which rose 40.6% year-over-year (YoY) to $35.9 billion, beating consensus estimates by $404.5 million. Management emphasized that customers, particularly cloud service providers, continue to signal strong and sustained demand.

Advanced Technology Leadership Remains Unmatched

TSMC's competitive edge comes from its ability to constantly lead in advanced process technology. Even leading players like Intel and Samsung struggle to match TSMC’s scale, yield, and consistency, making it the default partner for the world’s leading chip designers. In Q1, advanced nodes (7nm and below) accounted for 74% of wafer revenue, reflecting the company's transition towards higher-value products. Furthermore, the 3nm process alone accounted for 25% of revenue, with 5nm contributing 36%. The fast adoption of cutting-edge nodes highlights both strong customer demand and TSMC's execution capability.

The company is already ramping up its 2nm technology, which began high-volume production in late 2025. The next-generation A14 process is also on track, promising significant improvements in performance, power efficiency, and chip density. This technological edge has translated into pricing power and customer loyalty, keeping TSMC’s long-term prospects intact.

Margin Expansion Signals Operational Strength

TSMC is betting big on its future with aggressive capital expenditure plans, with plans to invest between $52 billion and $56 billion by 2026. The company is expanding its global footprint, with new fabs planned in Taiwan, the U.S., and Japan. It is also increasing the capacity of its 3nm technology to accommodate rising AI demand.

What has worried semiconductor companies of late is that capacity constraints are limiting growth. But, with this expansion, TSMC is positioning itself to capture as much demand as possible. With regards to AI stocks this year, higher capital spending has also been another major concern among investors. But TSMC has ensured its bottom line shows it is as strong as its top line. Gross margin rose to 66.2%, while operating margin reached 58.1% in the quarter, owing to higher capacity utilization, cost efficiency, and a favorable product mix. Earnings per share (EPS) rose 58.3% in Q1.

This indicates that TSMC is extracting more value from its massive investments. Even as the company ramps up new technologies like 2nm, it expects to maintain strong profitability through operational excellence and scale advantages.

Is TSM Stock a Buy Now?

TSMC’s outlook further strengthens the bullish case. The company expects Q2 revenue between $39 billion and $40.2 billion, representing over 30% YoY growth at the midpoint. Given the ongoing macroeconomic uncertainties, including geopolitical tensions and rising input costs, this upbeat outlook is impressive.

The company expects AI demand will continue to drive growth throughout 2026, with full-year revenue expected to increase by more than 30%. The semiconductor industry is cyclical. This level of growth in a cyclical industry highlights TSMC’s dominance in advanced chip manufacturing. Analysts remain equally optimistic and predict a revenue increase of 35% in 2026 to $163 billion, along with an earnings increase of 45.9% to $15.54 per share. Revenue and earnings could further increase by 24.7% and 23.5% in 2027. Given the level of growth anticipated, TSMC stock is still reasonably valued at 19x forward earnings.

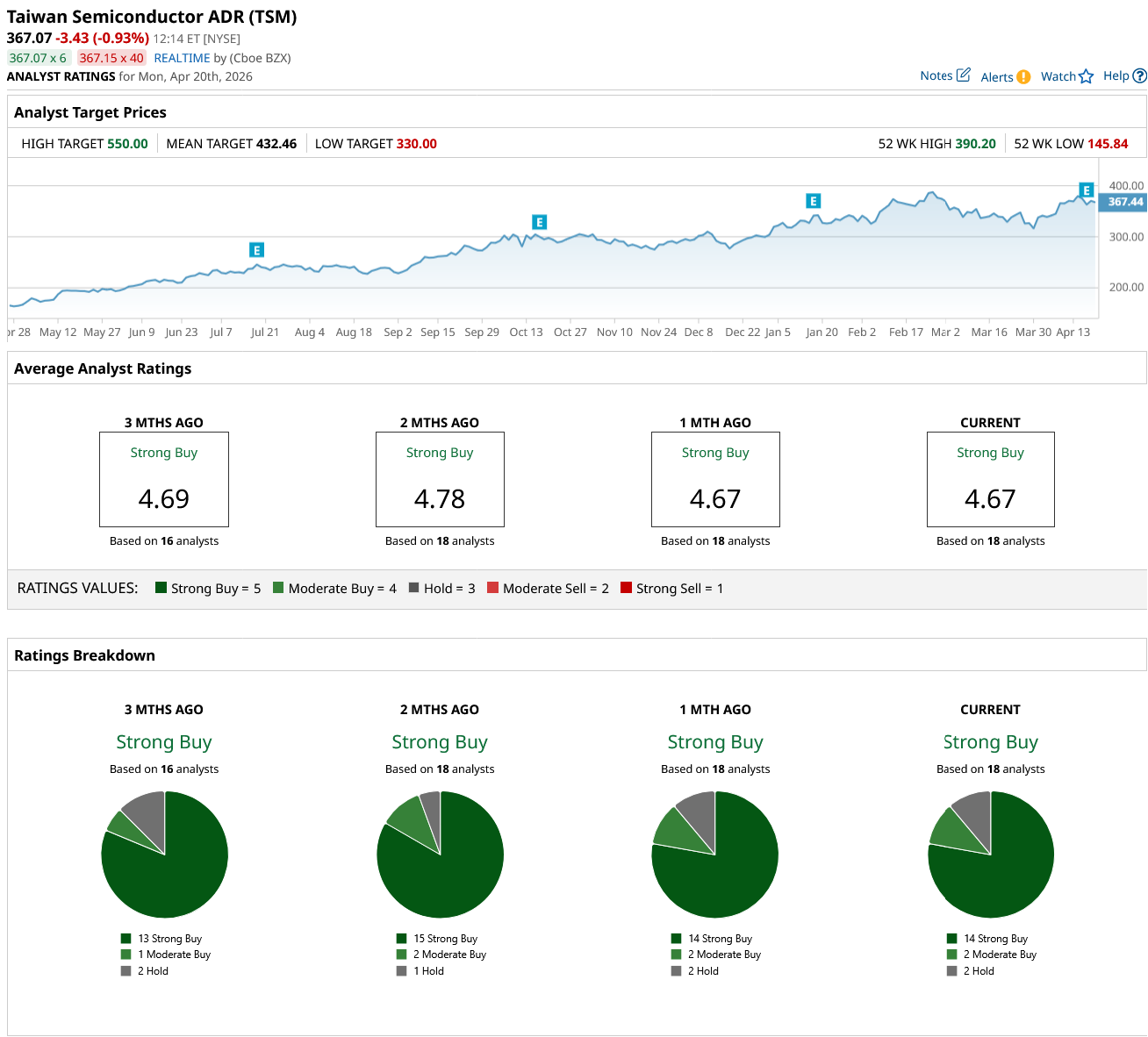

Its strong Q1 report and an upbeat outlook made Wall Street hold on to its consensus “Strong Buy” rating. Out of the 18 analysts that cover the stock, 14 rate it a “Strong Buy,” two say it is a “Moderate Buy,” and two rate it a “Hold.” Based on the average price target of $432.46, the stock has an upside potential of 17% from current levels. Plus, its high target price of $550 implies a potential upside of 48% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Tilray Stock Pops on New Trump-Driven Cannabis Hopes. Should You Chase the Rally?

- Tim Cook Is Stepping Down as Apple CEO, AAPL Stock Dips in After-Hours Trading

- Save This Psychedelic Stock Watchlist After Trump’s Latest Executive Order

- BlackBerry Stock Is Soaring on a New Nvidia Deal. Does That Make BB a Buy Here?