With a market cap of $44 billion, Westinghouse Air Brake Technologies Corporation (WAB) is a leading global provider of equipment, systems, digital solutions, and services for the freight rail and passenger transit industries. Headquartered in Pittsburgh, Pennsylvania, the company develops technologies that improve the safety, efficiency, reliability, and productivity of rail transportation networks worldwide.

Over the past 52 weeks, WAB shares have climbed 27.1%, slightly trailing the S&P 500 Index’s ($SPX) 27.4% gain. However, in 2026, the stock has advanced 19.5%, while the broader index has rallied 8.8%.

Zooming in, the stock has outpaced the State Street Industrial Select Sector SPDR ETF (XLI), which has gained 20.7% over the past year and returned 9.9% on a YTD basis.

On Apr. 22, WAB shares rose 1.5% after the company delivered solid first-quarter earnings, supported by strong demand across its freight and transit businesses, margin expansion, and continued growth in high-margin services and digital solutions. Its sales stood at $2.95 billion, representing a 13% year-over-year increase, driven by higher Freight segment sales, increased service activity, and continued momentum in modernization and digital rail technologies. Its adjusted earnings per share rose to about $2.71, exceeding Wall Street expectations.

For fiscal year 2026, ending in December, analysts expect diluted EPS to grow 18.3% year over year to $10.61. Notably, Wabtec has exceeded EPS estimates in each of the past four quarters, which is impressive.

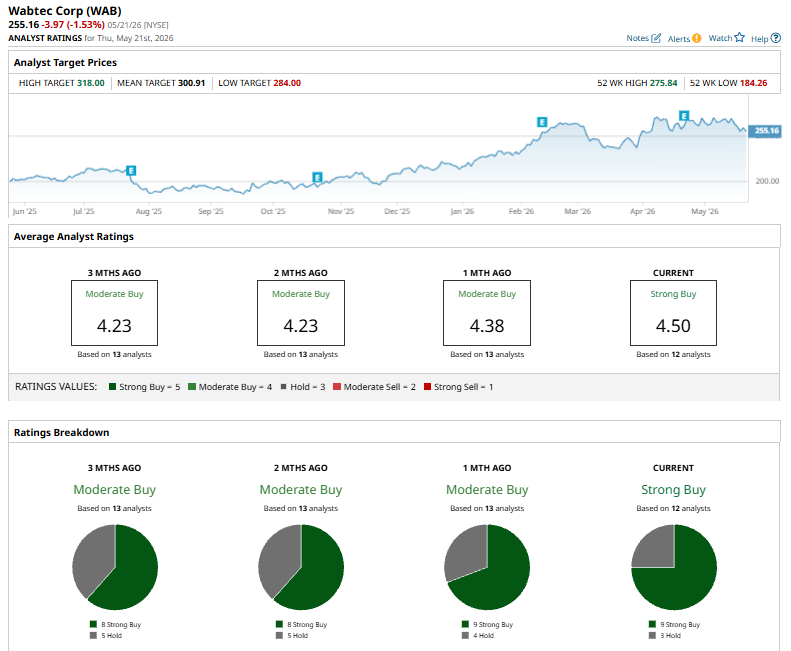

Wall Street continues to assign WAB stock an overall rating of “Strong Buy.” Of the 12 analysts covering the stock, nine recommend “Strong Buy,” and the remaining three suggest “Hold.”

Analyst sentiment has strengthened meaningfully from one month ago, when it had an overall “Moderate Buy” rating.

On April 23, Wells Fargo analyst Jerry Revich reiterated an “Equal-Weight” rating on Westinghouse Air Brake Technologies and set a price target of $284, reflecting a balanced outlook on the company’s near-term growth prospects and valuation.

WAB’s average price target of $300.91 represents potential upside of 17.9%. Meanwhile, the Street-high target of $318 suggests a potential upswing of 24.6% from current price levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart