Corning (GLW), best known for making the glass on iPhone screens, saw its shares rally by 12% in yesterday's trading session after it bagged a deal from chip giant Nvidia (NVDA) to enhance the latter's fiber-optic connectivity. Moreover, the deal will involve the companies jointly building three new manufacturing plants in North Carolina and Texas, with the potential to generate more than 3,000 jobs.

Commenting on the development, Corning's President and CEO, Wendel Weeks, said, "What NVIDIA is doing is nothing short of extraordinary, not just for the future of artificial intelligence, but for the American advanced manufacturing workforce. Their commitment is directly fueling the expansion of our U.S. manufacturing footprint and creating more than 3,000 new high-paying jobs for American workers. This partnership is proof that AI is not just a technology story. It is a manufacturing story, and it is happening here in the United States. Together with NVIDIA, we are ensuring the critical technologies powering AI are invented, engineered, and built in America."

About Corning

Founded way back in 1851, Corning is an American institution. It is a specialty materials and glass technology company known for innovations in optical fiber, Gorilla Glass, display glass, semiconductor materials, and life sciences products. The company has reinvented itself several times over the years with its presence in industries as varied as AI infrastructure and environmental technologies.

Valued at a market cap of $139.5 billion, GLW stock has more than doubled this year, growing by 105% on a year-to-date (YTD) basis. The stock also offers a dividend yield of 0.70%.

Why Corning?

I will answer this question in a dual manner. One, with respect to Nvidia, and the other with a broader perspective in the context of the company's products and offerings.

First, Nvidia needed a partner capable of delivering optical connectivity at a scale that virtually no other company on earth can handle, and Corning fits that role better than anyone else in the industry.

Corning invented low-loss optical fiber and has since built a reputation as the foremost innovator in glass science and optical physics across the globe. For a company like Nvidia that is assembling AI factories running thousands of GPUs at the same time, having a partner with the credibility and technical depth that Corning brings is critical.

The engineering reality behind this deal is fairly clear to understand. Present AI workloads depend on thousands of Nvidia GPUs, and those GPUs in turn place staggering demands on high-performance optical fiber, connectivity infrastructure, and photonics to shuttle data at speeds and volumes that were unimaginable just a few years ago. Copper wiring, which served data centers reliably for decades, simply cannot meet those demands anymore. Nvidia appears to be moving toward replacing copper with Corning optical glass fiber in its AI rack-scale systems through an integration method known as “co-packaged optics,” something Nvidia CEO Jensen Huang described as indispensable to the broader AI buildout when he addressed attendees at the GTC conference in 2025.

This is because copper cables top out at roughly 10 Gbps and begin to lose signal integrity beyond about 100 meters in high-performance settings. Conversely, fiber optic cables can sustain speeds of 100 Gbps and well above that across distances measured in kilometers, all without needing any signal regeneration along the way. That advantage has only grown more pronounced recently, with certain fiber optic transmission configurations now reaching 800 Gbps and a 1.6 Tbps threshold already within reach. There is also a specific distance constraint with copper that becomes especially damaging inside AI environments. At approximately 200 Gbps per lane, passive copper connections begin to fall apart after only two to three meters as signal integrity collapses.

Copper is also vulnerable to crosstalk and electromagnetic interference, which erodes signal quality and forces engineers to add shielding that adds cost and complexity. Optical fiber carries no such vulnerability because its non-metallic composition makes it entirely immune to electromagnetic interference, delivering consistent and stable transmission even in environments saturated with electronic noise.

However, what gives Corning genuine and durable pricing power in this space is its proprietary Contour fiber technology. Contour fiber allows twice the number of fiber strands to fit inside a standard conduit and consolidates what would normally be 16 separate connectors down to a single unified connector. That simplifies installation considerably for hyperscalers while cutting down the number of potential failure points throughout the network. CEO Wendell Weeks holds the patent on this technology personally, which means no competitor can simply replicate it by throwing capital at a new factory and waiting for production to scale.

The March partnership with US Conec to license PRIZM optical ferrule technology added another layer to Corning's positioning as well. That approach uses microlenses aligned precisely to the fiber rather than placing fibers in direct physical contact with one another. For data center operators preparing to scale their AI infrastructure both vertically and horizontally, the practical outcome is faster deployment, more reliable contamination management, and a lower total cost of ownership over the life of the installation. Corning also used the 2026 Optical Fiber Conference to announce the launch of new multicore fiber, microcables, and specialized connectors designed with dense AI networks specifically in mind.

Beyond the AI opportunity, the wider footprint of Corning's business tells its own story about the company's reach and resilience. Gorilla Glass is embedded in more than 8 billion devices worldwide, and Apple (AAPL) committed $2.5 billion to source all cover glass for iPhones and Apple Watches from Corning's Kentucky manufacturing facility. On the energy side, management projects that its Solar Market Access Platform will grow from approximately $1 billion in revenue in 2024 to around $2.5 billion by 2028.

Thus, across every one of these industries, the pattern remains the same. Corning manufactures things that other companies cannot produce, and it does so at a scale that other companies cannot match.

Financials on a Strong Footing

Over the past 10 years, the company has grown its revenue and earnings at CAGRs of 6.26% and 13.29%, respectively. Although it may seem modest, the ensuing AI infrastructure buildout presents Corning with an opportunity to accelerate on both these fronts.

A glimpse of that was offered in the company's numbers for the most recent quarter, Q1 2026.

Core sales for the quarter grew by 20% from the previous year to $4.34 billion. Optical communications and the solar segments were the glistening stars as they grew by 36% and 80% in the same period to $1.85 billion and $370 million, respectively. However, its second-largest revenue segment of Glass Innovations, which includes its most famous Gorilla Glass, witnessed a rise of just 1% year-over-year (YoY) to $1.42 billion. This is a bit of a surprise considering iPhone 17 sales were quite strong.

Meanwhile, earnings rose by 30% from the prior year to come in at $0.70 per share. Not only was this higher than the consensus estimate of $0.69 per share, it was also the eighth consecutive quarter of earnings beats from the company.

Overall, Corning is expecting revenues of $4.6 billion and EPS to be between $0.73 and $0.77. This is comparable to the Street's expectations of revenue and earnings of $4.63 billion and $0.76 per share, respectively.

Q1 2026 also saw the company substantially grow its net cash from operations to $362 million from $151 million in the year-ago period. Overall, Corning closed the quarter with a cash balance of $1.76 billion, higher than its short-term debt levels of $1.26 billion.

However, valuations remain an issue, as the stock trades at a sizable premium to both its respective sector median and its 5-year average. Notably, GLW is trading at a forward P/E, P/S, and P/CF of 51.11, 7.36, and 40.67 compared to the sector medians of 24.08, 3.27, and 18.69, respectively.

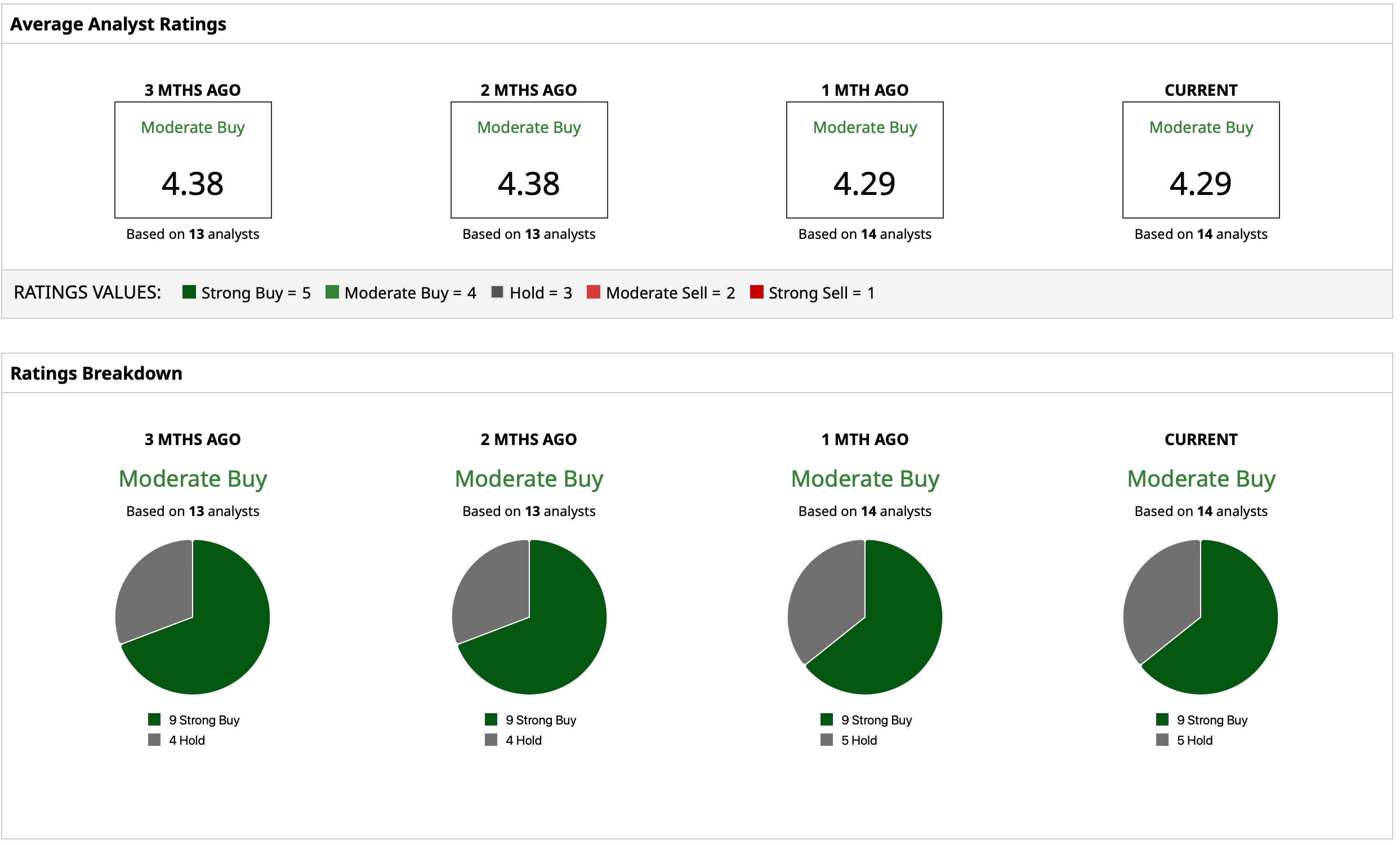

Analyst Opinion of GLW Stock

Taking all of this into account, analysts have deemed GLW stock a consensus “Moderate Buy” with a mean target price that has already been surpassed. The high target price of $200 indicates an upside potential of about 11% from current levels. Out of 14 analysts covering the stock, nine have a “Strong Buy” rating, and five have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- CHRN Stock Just Started Trading as Applied Digital Spins Off ChronoScale. How to Play Shares Here.

- If You Are Bullish on Agentic AI, Western Digital Is a Top Stock to Buy

- A $100 Billion Reason to Buy Apple Stock Here

- ‘Every Company Is an AI Company Today,’ Billionaire Bill Ackman Says. Here’s What’s Driving Pershing Square’s Big Bet on Meta Platforms.