Physical corporate cards used to feel practical. Now they often slow finance teams down, hide spend until it's too late, and leave too much room for misuse.

If you manage budgets for a growing company, you need control before money leaves the account, not after the statement arrives. That shift is why more CFOs, finance managers, and founders are moving from plastic cards to virtual ones.

What makes physical cards hard to manage at scale

Plastic cards work well enough when a company is small and spending is simple. Once teams add more vendors, more software, and more employees in different places, that model starts to crack.

A physical card is a fixed object in a business that changes every week. Limits need updates. People join and leave. Vendors renew at odd times. Shared cards get passed around because they seem convenient, then nobody fully owns the spend.

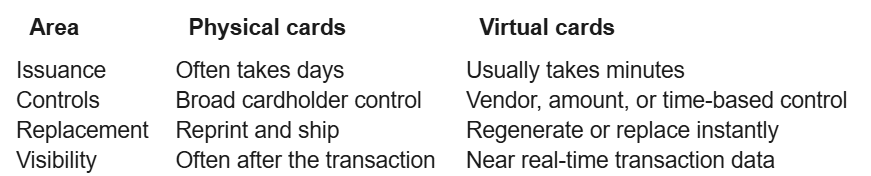

This quick comparison shows why the old setup creates friction:

For a modern finance team, those differences add up fast. A corporate card program should support centralized oversight, not create more loose ends.

The hidden admin work behind every plastic card

Every plastic card creates a trail of manual work. Someone requests it, finance approves it, the issuer prints it, and then someone waits for delivery. If the card is lost, expires, or the employee leaves, the whole cycle starts again.

Then there is the cleanup. Finance teams have to update recurring vendors, reset spending limits, collect receipts, and answer basic questions about who owns which card. Month-end gets heavier because the card itself doesn't carry much context.

Shared plastic cards make this worse. One card might pay for a design tool, a cloud bill, and a last-minute ad purchase. When the statement lands, accounting has to sort the mess out by hand. That isn't finance work with high value. It's logistics.

Why poor visibility turns into budget waste

Budget waste often starts with weak context, not big fraud. A card statement may show the vendor name and amount, but it rarely tells you who approved the purchase, which team owns it, or whether the charge fits policy.

That gap matters most with subscriptions. SaaS spend, cloud services, and online ads renew in the background. If several teams use the same shared card, duplicate tools and unplanned upgrades can slip through. By the time finance spots the issue, the money is gone.

Poor visibility also opens the door to shadow IT. A manager signs up for a tool on a company card. Another team buys a similar tool later. No one notices until renewal season. For CFOs who want tighter budget control, physical cards often create the opposite result.

Why virtual cards give CFOs more control and less risk

Virtual cards fit the way companies spend now. Most business payments happen online, through software vendors, cloud platforms, ad accounts, and remote teams. In that setting, a digital card is easier to control than a piece of plastic.

Physical cards still make sense for travel, in-person meals, and occasional face-to-face purchases. But for repeatable company spend, virtual cards give treasury and finance teams a better operating model.

Set limits by team, vendor, or subscription

The biggest win is precision. A CFO can issue one card for one vendor, one employee, one project, or one recurring subscription. That changes the whole control model.

Instead of handing out a general-purpose card, finance can set a spend cap, expiration date, and merchant rules before the first transaction happens. A recruiting tool can have one monthly limit. A cloud test project can get a short-term budget. A contractor can receive a card that stops working after the engagement ends.

That level of control reduces accidental overspend and policy drift. It also helps when a vendor tries to raise a renewal price without warning. If the card is capped or tied to a specific amount, the charge gets blocked or flagged right away.

Reduce fraud exposure with short-lived card details

A plastic card is reusable by design. If the number leaks, the fraud risk can stretch across many transactions and vendors.

Virtual cards cut that exposure. Some are single-use. Others are locked to one vendor or active only for a set period. If card details get exposed, the damage stays contained because the number isn't useful outside the approved context.

This matters even more for distributed teams. Remote employees, agencies, and contractors often buy services online. A short-lived virtual card is safer than sharing a long-term plastic number over chat or email. It gives finance tighter control and lowers the blast radius of a bad payment event.

Issue cards instantly instead of waiting on plastic

Speed matters in finance. A team may need to pay for a new software seat today, renew a cloud service before access is cut off, or start work with a supplier the same afternoon.

Virtual cards solve that timing problem. Finance can issue a card in minutes, without printing, shipping, or replacement logistics. If a card needs to be turned off, that can happen just as fast.

For scaling companies, this speed removes a lot of avoidable friction. The business keeps moving, while finance still keeps the rules in place.

How virtual cards help finance teams work faster every day

Control is only part of the story. The daily finance workload also gets lighter when every transaction arrives with clearer data.

That matters because most finance teams don't struggle with card payments alone. They struggle with reconciliation, missing receipts, unclear owners, and late visibility across departments.

Make reconciliation easier for accounting teams

A well-run virtual card program gives each transaction a home before it hits the ledger. The card can be tied to a person, team, vendor, cost center, or project, so accounting doesn't have to guess later.

Many platforms also sync card activity into accounting or ERP systems. That reduces manual matching and helps month-end close move faster. Instead of chasing down five departments for card context, the finance team starts with cleaner data.

Some spend tools also support receipt collection, read-only integrations, CSV uploads, and manual updates when needed. That flexibility helps companies clean up spend data without forcing one rigid workflow on every team.

See spending as it happens, not weeks later

Real-time visibility changes how CFOs manage budgets. When spend shows up as it happens, finance can catch unusual charges, off-policy purchases, and sudden vendor increases before they turn into bigger problems.

That also improves decision-making across the business. Department leaders can see how much budget is left. Finance can review trends during the month, not only at close. Procurement and treasury teams get a clearer signal when a vendor relationship needs attention.

This kind of visibility is even stronger when card data sits next to SaaS tracking and shadow IT discovery. Then you are not only seeing transactions, you are seeing the full picture of who bought the tool and whether the company still needs it.

Separate company spending from personal or shared expenses

Dedicated virtual cards reduce the gray area that causes bad records. When one card belongs to one owner or one use case, finance can assign spend correctly from the start.

That helps with SaaS, cloud usage, paid media, and procurement purchases. Each spend line can connect to the right team and budget owner. If someone leaves the company, finance can deactivate only that card without touching unrelated vendors.

For founders and COOs who still wear the finance hat, this is a major upgrade. It turns scattered spending into something cleaner and easier to review.

What CFOs should look for in a virtual card platform

The card alone is not enough. CFOs need a platform that sits inside a wider spend system, with controls, approvals, visibility, and secure finance infrastructure behind it.

That is why the best options focus on centralized oversight, not only card issuance. If you are comparing virtual cards for corporate spend control, look at the full operating model around them.

Controls that match real finance policies

Finance policies should live in the workflow, not in a PDF nobody reads. A strong platform lets you apply rules that match the way your company approves spend.

Look for these features:

Per-card limits for one-time, recurring, or project-based spend

Merchant or vendor restrictions

Expiration dates and single-use card options

Approval flows for issuing cards or raising limits

Permissions by team, role, or cost center

For global teams, multi-currency support matters too. Some platforms combine cards with corporate accounts in major currencies and local payment rails such as SEPA or Faster Payments, which removes more manual work from treasury operations.

Visibility across SaaS, cloud, and team spend

Card data in a silo is not enough for a CFO. You need one view across subscriptions, cloud costs, vendor renewals, and team-level spending.

That is why broader spend platforms are gaining ground. Some combine virtual cards with SaaS audits, shadow IT discovery, procurement requests, and vendor negotiation support. Others add cloud discount programs or credits. When those tools connect, finance can do more than approve payments. It can shape total spend.

This is where the old plastic model falls short. A stack of statements cannot tell you which subscriptions overlap, which renewals are coming, or where you have room to cut cost.

Security and compliance features that reduce headaches

Strong controls are only useful if the underlying setup is safe. Ask how the cards are issued, how KYB and account verification work, and whether integrations are read-only.

Clean audit trails matter just as much. Finance should be able to see who created a card, who approved it, when limits changed, and how the card was used. That record makes internal reviews, audits, and policy checks easier.

It also helps to choose a provider built on established payments infrastructure. Secure issuance, clear transaction oversight, and customer-controlled access reduce the stress that comes with distributed spending.

Conclusion

Scaling companies outgrow physical corporate cards faster than many finance teams expect. Plastic is slow to issue, hard to manage across departments, and weak on real-time visibility.

Virtual cards give CFOs tighter spend control, faster payment setup, lower fraud exposure, and less admin at close. The real shift is bigger than replacing a card format. It is about building a finance operation that is easier to control every day.