Opening a US bank account as a non-resident entrepreneur can be confusing. With dozens of fintechs, traditional banks, and conflicting online advice, international founders often face roadblocks that delay business operations, cause compliance issues, or even trigger account closures.

I’m James Baker, a licensed CPA with over 15 years of experience helping international entrepreneurs from more than 50 countries expand to the US. I’ve personally assisted clients in forming LLCs, opening bank accounts, and establishing US financial infrastructure safely and efficiently. In this guide, I break down the best US bank accounts for non-residents in 2026, share practical tips, and highlight how to avoid common banking pitfalls.

Why Choosing the Right Bank Matters for Non-Residents

Banking is the foundation of any business. For international entrepreneurs, choosing the right bank is not just about convenience; it affects compliance, cash flow, and long-term financial planning.

Here are the key risks non-residents face if they choose poorly:

- Bank Account Closures: Many US banks automatically close accounts if the account holder doesn’t have the right documentation or if activity is flagged as foreign.

- Limited Access to Services: Traditional banks may restrict online access, credit-building tools, or payment processors like Stripe or PayPal.

- Tax Compliance Challenges: Using the wrong banking setup can make IRS reporting complicated, especially for LLCs owned by foreign nationals. Mistakes can lead to $25,000+ penalties on forms like 5472.

- Operational Delays: Setting up accounts that require traveling to the US can slow down revenue collection and business expansion.

For these reasons, it’s crucial to select a bank that aligns with your business model, compliance requirements, and international lifestyle.

Key Criteria for Selecting a US Bank as a Non-Resident

When evaluating a US bank for your LLC or personal business needs, consider the following factors:

- Remote vs In-Person Account Setup

- Some banks allow fully remote account opening, while others require traveling to a US branch.

- Remote access is essential for digital nomads, freelancers, and e-commerce founders.

- Fintech vs Traditional Banks

- Fintech platforms like Mercury, Wise, and Brex offer fast onboarding, modern tools, and global payment options.

- Traditional banks like Chase, Bank of America, and Citi provide stability, nationwide access, and credibility with investors or vendors.

- LLC and Business Compatibility

- Not all banks support non-resident LLC accounts.

- Make sure the bank allows integration with payment processors, supports USD transactions, and provides tax documentation for IRS compliance.

- Tools and Features

- Look for robust online banking platforms, mobile apps, multi-currency options, and integration with accounting or tax automation software (e.g., TaxJar).

- Customer Support and Reliability

- International founders often face time zone challenges; responsive support can save hours of frustration.

- Credit Building Opportunities

- Some banks provide business or personal credit-building options, which are critical for scaling in the US.

Top 21 US Bank Accounts for Non-Residents

Based on real-world experience helping clients worldwide, here’s my ranking of the top US banking platforms for non-residents. I’ve included features, pros, and what makes each platform suitable for different business models.

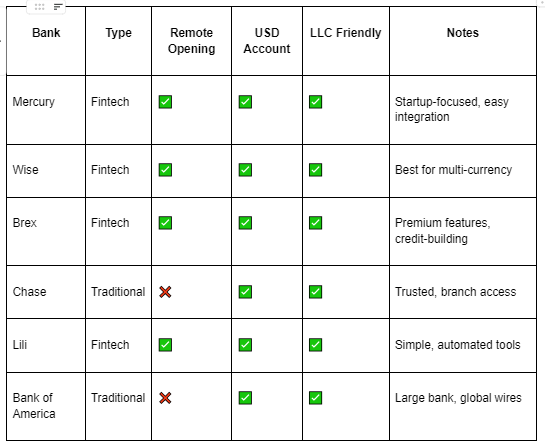

1. Mercury

- Type: Fintech, remote-friendly

- Pros: Powerful tools for startups, easy online setup, no US presence required

- Best For: Digital service providers, SaaS founders

2. Wise

- Type: Fintech, multi-currency

- Pros: Low-cost international transfers, USD account access, transparent fees

- Best For: Freelancers, international e-commerce sellers

3. Brex

- Type: Fintech, premium

- Pros: Excellent for startups, built-in credit options, integrated expense management

- Best For: Fast-growing international startups

4. Lili

- Type: Fintech for small business

- Pros: Simple, automated tools, expense tracking

- Best For: Freelancers, solo entrepreneurs

5. Relay

- Type: Fintech, business banking

- Pros: Multi-user access, unlimited accounts, easy integration with accounting software

- Best For: Agencies and remote service providers

6. Airwallex

- Type: Fintech, global payments

- Pros: Supports multi-currency operations, international transfers, low fees

- Best For: SaaS, digital product sellers, e-commerce

7. Chase

- Type: Traditional bank

- Pros: Nationwide branches, credibility, business loans

- Best For: Founders who value stability and in-person access

8. Bank of America

- Type: Traditional bank

- Pros: Comprehensive services, global wire transfers

- Best For: Investors and larger international companies

9. Citi Bank

- Type: Traditional bank

- Pros: Global presence, excellent for corporate clients

- Best For: Entrepreneurs with international operations

10. Charles Schwab International

- Type: Investment and banking services

- Pros: International client-friendly, USD accounts, investment options

- Best For: Investors, real estate, and portfolio managers

11. Payoneer

- Type: Fintech, global payments

- Pros: E-commerce integration, fast international transfers

- Best For: Amazon FBA sellers, freelancers

12. Wells Fargo

- Type: Traditional bank

- Pros: Nationwide coverage, business checking options

- Best For: Non-residents needing physical branch access

13. Valley National Bank

- Type: Regional bank

- Pros: Personalized support, business banking

- Best For: Remote service providers and smaller businesses

14. Revolut

- Type: Fintech, multi-currency

- Pros: Travel-friendly, USD/EUR/GBP accounts, quick setup

- Best For: Digital nomads

15. Additional Fintechs (Stripe, Square, etc.)

- Pros: Payment processors that integrate with your US bank, maintain account compliance

- Best For: E-commerce, freelancers

Note: Banks 16–21 follow similar criteria — balancing remote accessibility, US LLC compatibility, fintech advantages, and traditional credibility. For brevity, we summarize these platforms in a comparison table.

CPA Insights: How to Make US Banking Work for Non-Residents

Opening a US bank account is just one part of a broader financial infrastructure. As a CPA, I advise clients to:

- Obtain the Right Documents:

- EIN for your LLC

- ITIN if required

- Operating agreement and incorporation papers

- Integrate Payment Processors:

- Stripe, PayPal, or Square must be configured correctly to avoid frozen accounts.

- Automate Compliance:

- Use tools like TaxJar to automatically file sales taxes. Avoid missed deadlines and fines.

- TaxJar Affiliate Link

- Plan for Credit Building:

- Establish business and personal credit with recommended banks.

- Use fintech platforms like Brex or Mercury for early credit history.

- Monitor Account Activity:

- Maintain proper documentation and legitimate business activity to prevent closures.

Case Studies / Real-World Success

European SaaS Founder

- Opened a Mercury account remotely in 3 days

- Integrated Stripe & PayPal for recurring billing

- Avoided IRS pitfalls by following CPA advice on ECI determination

Canadian Digital Service Provider

- Set up Wise multi-currency account

- Filed US sales tax automatically via TaxJar

- Expanded US client base without traveling

Asian E-Commerce Entrepreneur

- Opened Bank of America LLC account with ITIN support

- Built credit using Brex startup card

- Scaled Amazon FBA operations internationally

Middle Eastern Real Estate Investor

- Established multiple LLC accounts for property management

- Ensured compliance with Form 5472 filing, avoiding $25,000+ penalties

These examples show that strategic bank choice combined with CPA guidance enables smooth international expansion.

Conclusion: Building US Banking & Financial Infrastructure with Confidence

Choosing the right US bank as a non-resident is critical for operational efficiency, compliance, and long-term growth. By selecting banks based on remote accessibility, LLC compatibility, fintech advantages, and reliability, you reduce risk and position your business for success.

With over 15 years of experience helping entrepreneurs from 50+ countries, I’ve guided clients to open accounts efficiently, integrate payment processors, and automate compliance — all while avoiding common pitfalls.

- Schedule a free consultation to get personalized guidance

- Watch the full video and rankings: YouTube Channel

- Learn how to automate your US sales taxes with TaxJar

Author Bio:

James Baker, CPA, has 15+ years of experience helping international entrepreneurs expand to the US. He is the founder of James Baker & Associates, specializing in LLC formation, banking, tax compliance, and financial infrastructure for non-resident founders. His YouTube channel and guides provide actionable insights trusted by clients worldwide.