Carmax (NASDAQ: KMX) and the rest of the used car industry have suffered, and the hard times are not over. The good news is that conditions may not worsen, and this company is well-positioned and still positioned for the rebound. The key takeaway from the FQ4 report is that margin was much better than expected. That news is fueling an expectation for consensus-beating results in 2023 and has the market up more than 5%. The price surge confirms the bottom put in late last year and has this market set up for a reversal. The question is if it can break out of the trading range and move up to a new high or will continue to consolidate until later in the year.

“...we made significant progress to further improve the most customer-centric omni-channel experience in the industry, including enabling online self-progression for all of our retail customers and completing the nationwide rollout of our finance prequalification product.” said CEO Bill Nash in the press release.” We also enhanced our wholesale shopping experience by launching a modernized, mobile-friendly vehicle detail page. We are confident that we are well positioned to continue leading the used car industry and to accelerate growth when the market improves.”

Carmax Has Mixed Quarter, Opens New Stores

Carmax had a mixed quarter but in a way that reinvigorated bullish activity. Revenue of $5.72 billion is down 25.64% compared to last year and missed the Marketbeat.com consensus by 620 basis points, but the margin was much better than expected. The weakness in revenue is driven by a 14.1% decline in comp-store units fueled by a 12.6% decline in retail units, a 19.3% decline in wholesale units and lower prices in both categories. The retail price held up better and fell only 9.3% YOY but the wholesale price fell by 27% and may not recover soon.

The good news is that margin increased for the retail segment, with profit per car increasing by 3.75% to offset the decline in price and volume to some degree. The wholesale segment profit per car was relatively flat, which was also better than expected. The company also improved its SG&A spending, resulting in GAAP EPS of $0.44. This is down from last year’s $0.98, but that was the peak of the used car market. The EPS is $0.24 better than expected, and fiscal strength will continue into the new reporting year.

The company is still growing. Carmax opened 5 new stores in key markets during Q4 and has plans to open 5 more stores this year. As of EOY F2023, there are 240 Carmax locations in addition to the digital channels, so 5 stores are worth about 2% of revenue.

The Analysts May Provide A Catalyst, Or Cap Gains

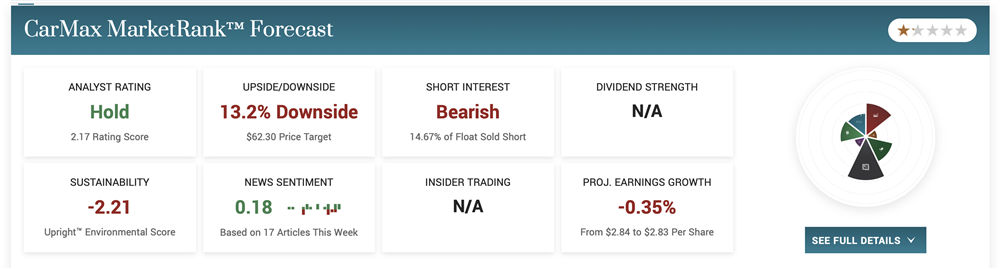

Marketbeat’s analyst tracking tools haven’t picked up any new reports since the Q4 release, but we know they are on the way. Until then, the analysts rate the stock a Hold with a price target of 13% below the current price action. The most recent targets are below the consensus, so upward movement may be capped. The catalyst would be a shift in sentiment that resulted in upgrades or price target increases. Still, even then, it would take significant increases to get the consensus above the trading range.

The chart is promising. The candle being formed on the weekly chart is large and green, showing support at critical levels. The caveat is that it is still well within the trading range, so resistance may be heavy as the price increases. If the market can get above the $80 level, a reversal will be in play, but even then, the next resistance target is just above, near $90.