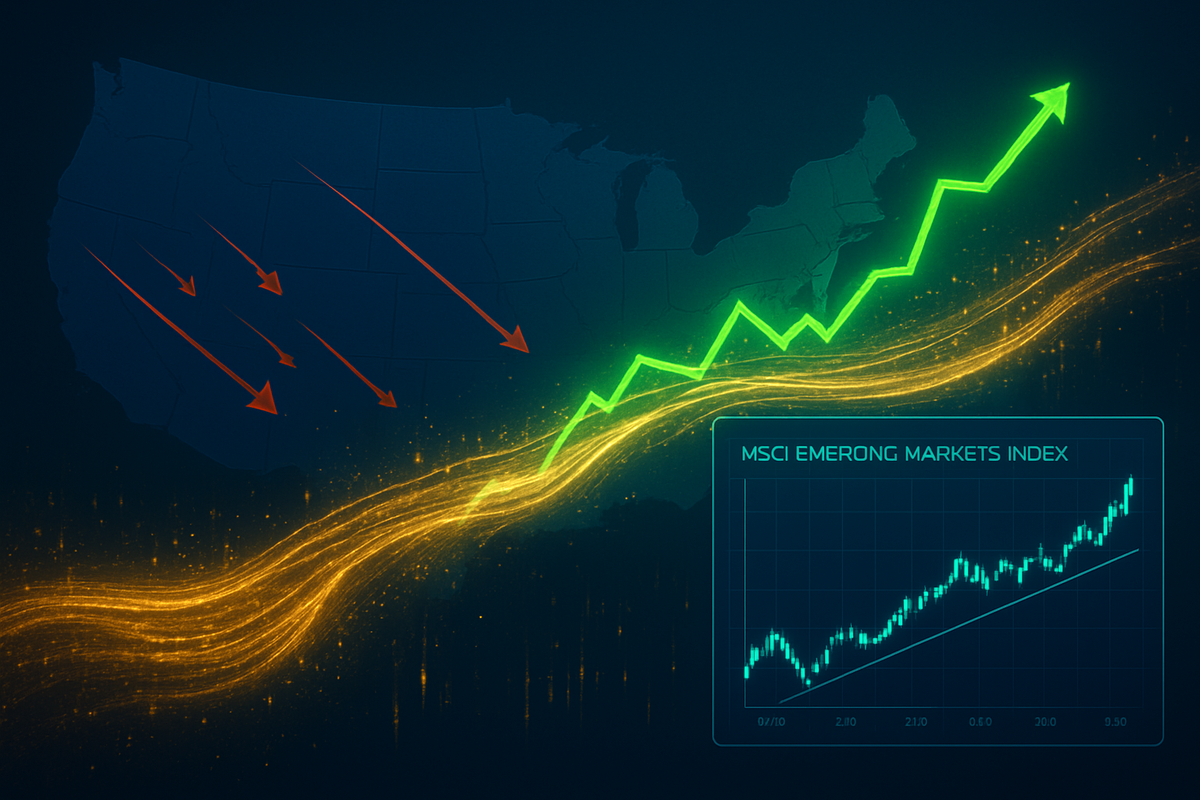

The financial landscape of 2026 is witnessing a profound shift in global capital as the "Emerging Markets Breakout" transitions from a technical signal to a full-blown market regime. For the first time in over fifteen years, the MSCI Emerging Markets Index has decisively cleared long-standing resistance levels, marking what analysts are calling the end of "U.S. Exceptionalism." As of March 4, 2026, the rotation of funds from domestic U.S. equities into developing markets has reached a fever pitch, driven by a combination of peak North American valuations and a "perfect storm" of domestic policy uncertainty that has left global investors searching for stability outside of the United States.

This massive migration of wealth is not merely a short-term trade but a structural recalibration. Data from the first two months of 2026 shows a staggering $15.4 billion flowing into diversified emerging-market equity funds in January alone—the largest monthly inflow on record. Meanwhile, the U.S. share of global capital inflows has plummeted to just 26%, a sharp contrast to its 92% dominance only a few years ago. This "Great Rotation" is being fueled by a weakening U.S. Dollar and a growing consensus that the growth engines of the next decade are firmly rooted in the high-tech corridors of East Asia and the burgeoning consumer markets of the Global South.

The Technical Trigger and the 'Liberation Day' Catalyst

The technical foundations for this breakout were laid in late 2025, but the momentum accelerated sharply in early 2026. The iShares Core MSCI Emerging Markets ETF (NYSE: IEMG) cleared the critical $70 resistance level in mid-January, a barrier that had capped the asset class since 2021. This absolute breakout was accompanied by a historic reversal in the MSCI EM vs. S&P 500 ratio chart, which breached a 15-year downtrend. By the end of February 2026, the KOSPI Index in South Korea surpassed the 5,000 mark for the first time in history, signaling that the rally was backed by significant breadth across multiple regions.

The immediate catalyst for this exodus from U.S. markets can be traced back to the "Liberation Day" proclamations of April 2, 2025. The enactment of broad, reciprocal tariffs—which raised the effective U.S. tariff rate to 17%—introduced a level of policy chaos not seen since the 1930s. Although the U.S. Supreme Court struck down these tariffs in the case of Learning Resources, Inc. v. Trump on February 20, 2026, the immediate invocation of Section 122 of the Trade Act of 1974 to impose a 15% global surcharge further spooked the markets. This "deliberate policy chaos," combined with a U.S. federal deficit exceeding 8% of GDP, has led institutional investors to treat emerging markets as a necessary hedge against domestic fiscal instability.

While the U.S. struggled with these headwinds, emerging economies were reporting stellar fundamentals. Consensus forecasts for 2026 show EM earnings growth accelerating to 29%, more than double the 14% growth expected for the S&P 500. This disparity has made the valuation gap—with U.S. equities trading at a Shiller P/E of 38x compared to EM's 16x—simply too large for the market to ignore. The result has been a coordinated "Sell America, Buy the World" sentiment that dominated the February 2026 trading sessions.

Winners of the East vs. Losers of the 'Software-mageddon'

The primary beneficiaries of this capital shift are the titans of the AI-semiconductor and financial sectors in Asia. Taiwan Semiconductor Manufacturing Co. (NYSE: TSM) has emerged as the vanguard of the breakout, with projected 2026 EPS growth of 36% driven by insatiable demand for 2nm AI chips. Similarly, South Korean giants Samsung Electronics (KRX: 005930) and SK Hynix (KRX: 000660) have reported record operating profits as the tech cycle shifts in favor of Asian hardware over U.S. software. In India, the financial sector is seeing unprecedented credit growth; HDFC Bank (NYSE: HDB) and ICICI Bank (NYSE: IBN) both reported significant year-over-year gains in net interest income as of their most recent February 2026 filings.

Conversely, the U.S. corporate landscape is grappling with the fallout of what traders are calling "Software-mageddon." High-flying software firms like ServiceNow (NYSE: NOW) and Oracle (NYSE: ORCL) have seen their market caps slashed by nearly 40-50% from their 2025 highs, as AI disruption and high valuations collide with a shrinking pool of domestic liquidity. Traditional American industry has not been spared either; Ford Motor Co. (NYSE: F) and Nike (NYSE: NKE) have been severely impacted by the 15% global surcharge, with Ford reporting over $2 billion in annual tariff-related costs that have eaten into margins and forced production delays.

The "Magnificent Seven" have also shown cracks. Microsoft (NASDAQ: MSFT) and Apple Inc. (NASDAQ: AAPL) were among the worst performers in early 2026, with Apple particularly exposed to the ongoing trade frictions and supply chain disruptions resulting from the administration's aggressive tariff stance. Even the private credit sector has felt the sting, as Blue Owl Capital (NYSE: OWL) saw its valuation drop by 25% in February due to its exposure to the struggling U.S. software and tech sectors.

A Super-Cycle Redux: Comparing 2026 to the 2003-2007 Boom

Analysts are increasingly drawing parallels between the current market environment and the legendary Emerging Markets Super-Cycle of 2003–2007. Just as that period was defined by a weakening U.S. Dollar following the dot-com bubble and the Iraq War, 2026 is characterized by a "Dollar Retreat" triggered by fiscal overreach and inflationary trade policies. In both eras, the primary driver was a search for "Alpha" in markets that had been ignored for a decade. The 15-year period of U.S. dominance that began in 2010 appears to have finally hit a wall of overvaluation and political exhaustion.

However, the 2026 breakout differs in its engine of growth. While the 2003–2007 bull run was a commodity-driven cycle fueled by China’s physical infrastructure boom, 2026 is an AI-infrastructure cycle. Taiwan and South Korea have replaced oil and ore exporters as the primary drivers of the MSCI Emerging Markets Index. Furthermore, the modern EM landscape is far more resilient than it was two decades ago, with many nations boasting robust local currency bond markets and significantly higher foreign exchange reserves, making them less susceptible to the "taper tantrums" of the past.

The broader significance of this event lies in the erosion of the U.S. Dollar’s status as the sole safe haven. The move into EM assets is not just a search for growth, but a strategic diversification away from a singular geopolitical risk. As the Federal Reserve begins to ease rates in early 2026 to combat a slowing domestic economy, the carry trade into higher-yielding EM currencies has accelerated, creating a self-reinforcing loop of capital appreciation and currency gains for international investors.

Navigating the Path Ahead: Strategic Pivots and Scenarios

Looking ahead, the longevity of this breakout will depend on the continued divergence between U.S. and EM policy paths. In the short term, the market expects the 15% global surcharge to remain a point of contention, likely keeping U.S. multinational margins under pressure. For investors, the strategic pivot involves shifting from "growth at any price" in U.S. tech to "growth at a reasonable price" in EM tech and financials. We are likely to see more institutional portfolios move toward a 10-15% allocation in emerging markets, up from the skeleton-weightings of 5% seen during the early 2020s.

Potential scenarios for the remainder of 2026 include a "Melt-Up" in Asian equities if China successfully navigates its AI-driven economic pivot, or a period of consolidation if the U.S. administration pivots back toward more traditional trade policies. However, the technical damage to the U.S. indices and the structural breakout in the MSCI EM Index suggest that any pullbacks in the developing world will likely be viewed as buying opportunities. The "Great Rotation" has cleared its first major hurdles, and the momentum appears to be sustainable through the year.

Market opportunities are particularly ripe in countries like India, where GST reforms and manufacturing incentives are bearing fruit, and in the "AI-Hardware Belt" of East Asia. The challenge for investors will be navigating the idiosyncratic risks of each nation, as the "Emerging Markets" tag now covers a diverse range of economies with varying degrees of sensitivity to global trade.

Summary and Investor Outlook

The emerging markets breakout of 2026 marks a definitive end to the era of U.S. market dominance. Triggered by a technical breach of a 15-year resistance level and fueled by a massive $15.4 billion monthly inflow of capital, the shift represents a search for growth and stability in the face of domestic U.S. policy uncertainty. While U.S. giants like Microsoft and Ford struggle with tariffs and valuation resets, EM leaders like TSMC and Samsung are capitalizing on a new global AI-infrastructure cycle.

Moving forward, the market is entering a phase where global liquidity seeks yield and value outside of traditional Western hubs. The 2026 breakout is not just a repeat of the 2003 bull run, but a sophisticated evolution driven by high-tech manufacturing and robust domestic consumption. For the remainder of the year, investors should watch the U.S. Dollar Index (DXY) for further signs of weakness and monitor the sustainability of the KOSPI and NIFTY breakouts.

The primary takeaway for March 2026 is clear: the risk of not being in emerging markets now outweighs the risk of the markets themselves. As the "Great Rotation" continues to unfold, those positioned in the diversified, high-growth economies of the East are likely to lead the global leaderboard for the foreseeable future.

This content is intended for informational purposes only and is not financial advice