- Pre-Tax NPV5% of USD825 million, Pre-Tax IRR of 34% and AISC of USD893/oz

- Steady State Average Annual Gold Production of approximately 188Koz

- Base Case Development Contemplates 14-Year Mine Life

Toronto, Ontario--(Newsfile Corp. - June 24, 2021) - Pasofino Gold Limited (TSXV: VEIN) (OTCQB: EFRGF) (FSE: N07) ("Pasofino" or the "Company") is pleased to announce that it has completed a PEA on the Dugbe Gold Project, which includes both the Dugbe F and Tuzon deposits. The Company is earning a 49% economic interest in the project (prior to the issuance of the Government of Liberia's 10% carried interest).

HIGHLIGHTS

- Significant Production Potential - Establishing a Foundation for a New Gold District

- 5Mtpa operation, producing approximately 2.5 Moz of gold over a 14-year Life-of-Mine (LoM).

- Steady state average annual gold production of approximately 188 Koz, with peak production of approximately 226 Koz in year 8 of operation.

- Strong Financial Metrics

- Pre-tax NPV5% of USD825M (USD627M post-tax), 34% IRR (31% post-tax) at a conservative base gold price of USD1,600/oz.

- Pre-tax NPV5% of USD1,153M (USD874M post-tax), at USD1,800/oz.

- Fast capital payback of approximately 2.9 years from start of production.

- LoM Cash flow of USD627M.[1]

- LoM AISC1 of USD893/oz and USD821/oz cash cost.1

- Simple Project with Economies of Scale

- LoM strip ratio of 4.5:1 highlighted by a low 2.8:1 ratio in the first 4 years.

- Low power costs of USD0.18/kWh, with opportunities for long term savings with alternative renewable energy sources.

- Significant community support built over more than a 10-year history of the Project.

- Development Capital

- Pre-production capital requirement of approximately USD391M. Exploration and Study Upside

- Much of the 2,599km2 land package is prospective. The Company has new drill targets in the pipeline following intensive surface exploration work undertaken over the last 6 months.

- Ongoing positive drilling results at Dugbe F and Tuzon will be included in updated Mineral Resource Estimates planned for July and August 2021.

- Current test work underway in at ALS Perth, Australia looking to improve metallurgical recoveries

KEY ASPECTS WHICH ENHANCE THE QUALITY OF THE PROJECT INCLUDE:

- 74km by road from the port of Greenville to the Dugbe Project.

- Dugbe F and Tuzon deposits are 4km apart, serviced by a central processing plant.

- USD0.18/kWh estimated mine life power costs.

Ian Stalker, CEO, commented; "We are extremely pleased with the set of outcomes from this PEA exercise. It underscores the potential of the Project to deliver significant value to all stakeholders going forward. Our consulting engineers and management team have set the basis for a quality feasibility study which is in progress, and which will incorporate the positive recent infill and step out exploration results recently announced. We look forward to completion of the Feasibility Study which should provide a solid foundation for the start of the build phase expected to occur in 2023

There are many key attributes of this Project demonstrated by the results of the PEA. However, from a practical construction and mining perspective, the following are worth highlighting:

- The proximity of the Project to the deep-water port of Greenville (74km away);

- The high productivity opportunity that both deposits on the Project offer provides added value to the development of Project.

- The constructive relationship enjoyed with the Government of Liberia"

The PEA was prepared in accordance with Canadian Securities Administrators' National Instrument 43-101 Standards of Disclosure for Mineral Projects ("NI 43-101"). The reader is advised that the PEA summarized in this news release is intended to provide only a high-level review of the project potential and design options. The PEA mine plan and economic model include numerous assumptions and the use of inferred mineral resources. The PEA is preliminary in nature, includes inferred mineral resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves, and there is no certainty that the PEA will be realized. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

TRADE-OFFS

DRA Global (South Africa) was appointed as lead consultant to prepare the PEA in accordance with NI 43-101, and was assisted by SRK Consulting Ltd (UK) and Epoch Resources (Pty) Ltd.

A number of trade-offs were completed by DRA Global and Pasofino during the PEA work, including the evaluation of processing capacities from 4Mtpa to 7Mpta and a trade-off on a full range of power options. The 5Mtpa option was identified as the most suitable capacity for the current project, based on the life of the project, estimated capital and shareholder return.

Figure 1: The Dugbe Project location of the Dugbe F and Tuzon and deposits

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/6283/88534_691b0dcc64fa7878_001full.jpg

For an owner mining scenario, the base case requires USD391M in initial capital. Operating costs are expected to be approximately USD826/oz during the initial years, and an average of USD893 /oz over the life of mine. During the first 4 years, operating costs are kept low by mining the shallow mineralized material in both pits (Dugbe F and Tuzon) at a targeted strip ratio of less than 2.8, increasing thereafter to an average of 6.8 over the balance of life of mine.

In terms of contained ounces, the PEA relies on 65% Indicated Resources and 35% Inferred Resources, from the Dugbe F and Tuzon deposits which are 4km apart. Updated Mineral Resource Estimate (MRE) on the Dugbe F and Tuzon deposit are anticipated to be released in July and August 2021. With the PEA now complete, the foundation is now set for the completion of the feasibility study in order to then fully demonstrate the financial viability of the Project, which is ongoing.

Other key considerations for the PEA included:

- Mining and processing scenarios that were considered ranging from 4 Mtpa to 7 Mtpa.

- Recent West African benchmarks were used to determine the capital and operating costs.

- Work to date has included the potential for power generation from hydro power and thermal co-generation with photovoltaics (PVs). This may effectively reduce the project operating cost and carbon footprint.

- Various TSF options have been initially evaluated in accordance with the stringent new Global Industry Standard on Tailings Management classification.

PROJECT DESCRIPTION AND LOCATION

The Project is located in south-eastern Liberia, approximately 60km east of Greenville and 240km south-east of the capital Monrovia. The combined Project covers an area of 2,559km2 and is defined within a single Mineral Development Agreement (MDA), issued to Hummingbird in January 2019, valid for 25 years. The centre of the Project has an approximate latitude of 5.093º and longitude of -8.502º. The Dugbe F and Tuzon deposits are approximately 4km apart.

The Sackor Prospect is located 2.5km SW of Dugbe F. The Project area comprises a number of license areas that were amalgamated, the most recent of these being the Central License area.

Figure 2. Project Location in Liberia

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/6283/88534_691b0dcc64fa7878_002full.jpg

The Project area is an undeveloped area of Liberia, with one main access road, recently upgraded by the mine, and several villages. Most people in the area engage in artisanal mining, hunting or small-scale farming. No utilities such as power and water are available. The area is primarily degraded rainforest over low rolling hills, interspersed with numerous rivers. A sizable river, the Geebo, divides the two deposits. The climate is typically tropical, with high humidity, daytime temperatures and rainfall. The nearest town of consequence is Greenville, the Sinoe County capital, which has a basic port and a palm oil processing centre, but no grid-scale utilities.

MINERAL RESOURCE ESTIMATE

SRK originally produced an MRE for Tuzon in March 2014. Without any material further exploration work, SRK updated the Tuzon MRE with an effective date initially reported as 30 July 2020, later revised to 19 August 2020 to align both deposit estimates, using SRK's 2014 model but applying updated economic parameters.

CSA produced an updated MRE for the Dugbe F deposit with an effective date of 15 July 2020. SRK reviewed the CSA MRE for Dugbe F for the purposes of the Company's Technical Report and the PEA; the effective date of the Technical Report was revised to 19 August 2020 to align both estimates.

Table 1 provides the MRE for the Dugbe Gold Project which has been prepared in accordance with the terminology, definitions and guidelines given in the Canadian Institute of Mining, Metallurgy and Petroleum (CIM) Definition Standards for Mineral Resources and Mineral Reserves (May 2014) and has been reported in accordance with National Instrument (NI) 43-101 Standards of Disclosure for Mineral Projects. The Qualified Person for both estimates is Martin Pittuck (CEng, FGS, MIMMM). Martin Pittuck is an independent Qualified Person as defined by the Canadian National Instrument NI 43-101. No mining other than very minor artisanal workings has taken place at the deposits and therefore no depletion of the estimates was required. For both deposits, the Mineral Resource is restricted to a conceptual pit shell, as is required to establish reasonable prospects for eventual economic extraction (RPEEE). Both estimates are reported at a 0.5 g/t Au cut-off. Other parameters used for the conceptual pit-shell are provided in section.

Table 1. Mineral Resource for the Dugbe Gold Project

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/6283/88534_691b0dcc64fa7878_003full.jpg

Notes:

- The effective date of the Mineral Resource is 19 August 2020.

- The Mineral Resource assumes open pit mining at a cut-off grade of 0.5g/t Au and within a USD1700/oz gold conceptual pit shell.

- A geological loss of 5% has been applied to the mineralised volumes at Dugbe F due to barren late-stage intrusive pegmatites.

- Figures have been rounded to the appropriate level of precision for the reporting of Mineral Resources.

- The Mineral Resources are stated as in situ dry tonnes. All figures are in metric tonnes.

- The Mineral Resource has been classified under the guidelines of the Canadian Institute of Mining, Metallurgy and Petroleum (CIM) Standards on Mineral Resources and Reserves, Definitions and Guidelines prepared by the CIM Standing Committee on Reserve Definitions and adopted by CIM Council (2014), and procedures for classifying the reported Mineral Resources were undertaken within the context of the Canadian Securities Administrators' National Instrument 43-101 (NI 43-101).

- Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability.

MINING METHODS

Both the Dugbe F and Tuzon deposits are shallow and so amenable to open pit mining operations. The planned open pits will be mined utilising conventional truck and shovel method to supply mill feed to the run of mine (RoM) tip (near Tuzon) and waste to the respective pit's waste stockpile facilities.

The primary aim of the PEA work was to test and evaluate various mining and processing options in order to scope the more detailed study work to follow. Most of the testing and evaluation was carried out through mine optimisation models that included technical and financial data from all aspects of the planned operation. As Pasofino is completing drilling work with the intention of converting Inferred Resources into Indicated Resources, the PEA work included Inferred material, in order to obtain a more accurate processing capacity for the probable mine life.

Three rounds of optimisation were completed as the results and inputs were refined. The technical results will be used to guide the further Feasibility Study work. The results of one of the selected scenarios were also used to support the financial model in this report to determine the financial potential of that scenario.

Geological and production schedule data was used to determine a suitable mining approach and fleet, which in turn informed the optimisation work. A fleet option was selected and further detailed for the selected scenario.

MINERAL PROCESSING AND METALLURGICAL TESTING

A number of historical test work programs have been undertaken on samples originating from the Dugbe F and Tuzon deposits over the period 2009 to 2014. DRA reviewed the historical test work, with a primary focus on the Mintek work, to derive a conceptual level flowsheet, recovery and operating cost estimate for the updated PEA.

The Dugbe Gold Mine Project 5.0 Mtpa gold processing plant design has been based on a typical semi-autogenous grinding (SAG) and ball milling circuit followed by a carbon-in-leach (CIL) gold recovery circuit. This process flowsheet is well known in industry and has historically been proven as a successful processing route for oxide and fresh gold ores. Figure 3 below summarises the conceptual flowsheet for the PEA.

Figure 3. Conceptual flowsheet

To view an enhanced version of this graphic, please visit:

https://orders.newsfilecorp.com/files/6283/88534_691b0dcc64fa7878_004full.jpg

Based on previously reported similarities between the Dugbe F and Tuzon ore deposits in terms of mineralisation style, host lithology type and geometry, DRA interprets the metallurgical response for Dugbe F would be similar to Tuzon. The gold recoveries for Dugbe F and Tuzon oxide and fresh ore will be validated in the 2021 test work program undertaken at ALS laboratories.

From the historical test work, gold recoveries are expected to range from 87.1% to 89.5%, averaging 88.4% over LoM. The recovery assessment is based on a feed blend containing 71% Tuzon fresh material and 26% Dugbe F fresh material with the remaining 3% comprised of oxides.

PROJECT INFRASTRUCTURE

Access

The primary access is a 74km road from the port of Greenville to the mine site utilising the existing public road infrastructure. The main requirement is to upgrade the existing access roads and tracks to accommodate the anticipated traffic volumes during mining operations, as well as providing public access to the local villages. The road is split into two defined sections: the 30km road from Greenville Port to Plazon Junction and the 44km track from Plazon Junction to the mine site. Access along the 30km from Greenville to Plazon Junction consists of gravel roads that are mostly in fair condition. The balance of the primary access road, between Plazon Junction and the mine site, consists of existing gravel roads and tracks. This section will require extensive upgrades to meet the required standards.

Water

It is anticipated that the Project will be water positive, and as such care will be taken to ensure that all water discharged to the environment meets the necessary quality requirements as per local legislation and international best practice.

The main water systems will be the tailings storage facility (TSF) and the process plant. Tailings slurry will be delivered to the TSF and the solids will settle out. The TSF will collect rain and runoff water. Water will be returned to the process plant for reuse, and excess water will be discharged in a controlled manner to the environment.

Other water-related considerations are runoff from the waste storage facility (WSF) and process plant areas. Waste ore will be tested for any geochemical contamination before a decision is made regarding appropriate designs for the WSF. All runoff from the process plant will be directed to pollution control dams.

Power

An electric load list was developed, based on a preliminary mechanical equipment list (carbon-in-leach recovery flow sheet). The load demand of the process plant and associated infrastructure is anticipated to be 25MW (28MVA), whilst annual energy consumption is expected to be approximately 205GWh.

As there is no electrical utility infrastructure in the vicinity of the mine site, energy demands must be met through local generation. Power provision will be the largest single operating cost for the operation. Consequently, various power supply options were evaluated to find the most cost-effective solution. Power generation can also be a material source of greenhouse gases and environmental impact, so low carbon emission options were also considered.

A high-level trade-off study was completed to determine the most cost-effective power generation technologies available to the Project; where the levelized cost of energy was compared between thermal generation (diesel and HFO), hydroelectric power generation and solar photovoltaic (PV) power generation. The base case power generation costs considered in this report are based on HFO fueled thermal generation plant, as this technology is readily available to the Project. "Hybrid" power generation solutions, involving a portion of PV generation and battery storage, should result in a reduction in energy cost and will be assessed during the execution of the FS. Other 'green' generation technologies show a reduction in the levelized cost of energy but require an investment by third parties, which is being actively pursued by Pasofino.

Based on HFO fueled power generation, operating costs are expected at $0.18 per kWh, with USD52.1M capital investment required (the capital portion is assumed to be spread over a 12-year period, based on the application of a build-own-operate-transfer (BOOT) type contract agreement). The operating cost is primarily comprised of fuel cost, which is subject to fluctuation with the crude oil price (dated January 2021).

Several fuel suppliers have been approached, and several proposals have been received regarding the delivery of 2,935 kl HFO fuel to site per month. The volume of fuel required supports the landing of new fuel storage and handling infrastructure at Greenville Port, with delivery to site taking place via road tanker. The costs for the required supply chain infrastructure have been included in the budgetary cost per litre provided.

CAPITAL COST ESTIMATE

The project capital has been derived from four previous projects of a similar nature executed in West Africa and is summarised in the table below. Capital is within the accuracy of a Class 4 Association of the Advancement of Cost Engineering (AACE) estimate of (+50%/-30%).

Table 2. Project capital cost overview - base case

| Cost Category | Units | Total | Yr -1 | Yr 0 | Yr 1 | % of Total |

| Mining | USD M | 15 | - | - | 15 | 4 |

| Plant & Infrastructure (incl. Owner's Costs) | USD M | 298 | 15 | 104 | 179 | 76 |

| TSF | USD M | 40 | 2 | 14 | 24 | 10 |

| Other[2] | USD M | 37 | - | 15 | 22 | 10 |

| Total | USD M | 391 | 17 | 133 | 241 | 100 |

(Columns may not add up due to rounding)

OPERATING COST ESTIMATE

The operating costs over life of Project include mine operations, process plant, TSF and general and administrative (G&A) costs. Total LoM average operational costs are estimated to be approximately USD134 million per annum equivalent to a unit rate of USD28/t RoM. An overview of operational costs is presented in Table 3 below.

Table 3. Operating expenditure

| Description | LoM Ave, USD M pa | Unit Cost, USD/t RoM | % of Total |

| Mine | 49 | 10 | 37 |

| Process Plant | 71 | 15 | 53 |

| TSF | <1 | <1 | 1 |

| G&A | 12 | 3 | 9 |

| Total Operating Cost | 134 | 28 | 100 |

(columns may not add up due to rounding)

ECONOMIC OUTCOMES

The potential viability of the Project has been determined through developing an economic model founded on the results derived from the PEA. The financial model has been prepared on a 100% equity project basis and does not consider alternative financing scenarios. A discount rate of 5% has been applied in the analysis. A static metal price of USD1,600/oz has been applied. All-in sustaining costs have been reported as per the World Gold Council (WGC) guideline dated November 2018 and are exclusive of project capital, depreciation and amortisation costs. Capital payback is referenced to the timeline from initial production up to the point of realising a net zero cumulative cashflow. The key economic outcomes are presented in Table 4 on a pre-tax and post-tax basis.

The impact of initial capital costs has a limited elasticity in impacting overall project value due to the capital phasing profile and relatively low expenditure in comparison to revenue and operating costs over the prescribed LoM.

Table 4. Economic outcomes summary

| Description | Units | Value |

| Production Statistics | ||

| Production LoM | years | 14 |

| Total Ore Tonnes | Mt | 66.1 |

| Total Au Ounces Recovered | Moz | 2.5 |

| Steady State Average (Yrs 2 to 13) | ||

| Throughput | Mtpa | 5 |

| Au Grade | g/t | 1.34 |

| Au Recovery | % | 88.40 |

| Au Ounces Recovered | Oz/a | 180,259 |

| Initial Capital Estimate | USD M | 391 |

| Sustaining Capital Estimate | USD M | 170 |

| Operating Cost Estimate | ||

| Steady State Average (Yrs 2 to 13) | USD M/a | 134 |

| Steady State Average Unit Cost (Yrs 2 to 13) | USD/t | 28 |

| Financial Outcomes (PRE-TAX) | ||

| NPV | USD M | 825 |

| IRR | % | 34 |

| Payback Period (Undiscounted) | years | 2.8 |

| AISC | USD/oz | 893 |

| USD/t | 34 | |

| Financial Outcomes (POST-TAX) | ||

| NPV | USD M | 627 |

| IRR | % | 31 |

| Payback Period (Undiscounted) | years | 2.9 |

NPV SENSITIVITY TO GOLD PRICE

The impact of flexing gold price and discount rate on NPV (pre-and post-tax) has been assessed and presented in Table 5 below.

Table 5. Metal price and discount rate data tables

| Metal Price, USD/ozt | ||||||||

| Discount Rate | 1,200 | 1,300 | 1,400 | 1,500 | 1,570 | 1,600 | 1,700 | 1,800 |

| 5 | 168 | 333 | 497 | 661 | 776 | 825 | 989 | 1,153 |

| 10 | 33 | 151 | 270 | 388 | 470 | 506 | 624 | 742 |

| 15 | -46 | 43 | 132 | 220 | 283 | 309 | 398 | 487 |

| 20 | -94 | -25 | 45 | 114 | 162 | 183 | 252 | 321 |

| 25 | -123 | -68 | -12 | 43 | 82 | 98 | 154 | 209 |

| 30 | -142 | -96 | -51 | -5 | 26 | 40 | 86 | 131 |

| NPV (Pre-Tax), USDm | ||||||||

| Metal Price, USD/ozt | ||||||||

| Discount Rate | 1,200 | 1,300 | 1,400 | 1,500 | 1,570 | 1,600 | 1,700 | 1,800 |

| 5 | 126 | 254 | 379 | 504 | 590 | 627 | 751 | 874 |

| 10 | 10 | 105 | 198 | 289 | 352 | 378 | 468 | 556 |

| 15 | -59 | 15 | 86 | 156 | 203 | 224 | 291 | 358 |

| 20 | -101 | -42 | 15 | 70 | 107 | 123 | 176 | 228 |

| 25 | -128 | -79 | -32 | 12 | 43 | 56 | 98 | 140 |

| 30 | -145 | -104 | -65 | -27 | -2 | 8 | 44 | 78 |

| NPV (Post-Tax), USDm | ||||||||

OPPORTUNITIES:

A number of potential opportunities exist to improve the economics of the Dugbe project:

- reduce capital through contract mining,

- increase mine life or throughput when recent drilling at Dugbe, Tuzon and Sackor is included in the MRE,

- increase in recoveries based on further metallurgical testing,

- additional deposits may be discovered along strike from Tuzon following positive trench results (reported in 18 May 2021), and

- reduction in power costs with the potential for hydroelectric and solar power.

CURRENT WORK

Current work that is in progress includes:

- further geological, geotechnical and hydrogeological drilling,

- metallurgical test work from existing and new drill core, and

- environmental and social field work.

QUALIFIED PERSONS STATEMENT

Scientific or technical information in this disclosure (other than information that relates to mining, processing and related infrastructure results) was reviewed by Mr Martin Pittuck a full-time employee of SRK UK. Mr Pittuck is a member in good standing with the Institute of Materials, Minerals and Mining, a Fellow of the Geological Society of London and is a Chartered Engineer; he has sufficient experience which is relevant to the commodity, style of mineralization under consideration and activity which he is undertaking to qualify as a Qualified Person under National Instrument 43-101.

Scientific or technical information in this disclosure that relates to mining, processing and related infrastructure results was reviewed by Mr Robin Welsh, a full-time employee of DRA Global. Mr Welsh is a Professional Engineer in good standing with the Engineering Council of South Africa and has sufficient experience which is relevant to the project under consideration which he is undertaking to qualify as a Qualified Person under National Instrument 43-101.

This preliminary economic assessment is preliminary in nature, includes inferred resources that are considered too speculative to have the economic considerations applied to them that would enable them to be categorized as mineral reserves and there is no certainty the preliminary economic assessment will be realized.

ABOUT THE DUGBE GOLD PROJECT

The 2,559 km2 Dugbe Project is located in southern Liberia and situated within the south westmost part of the Birimian Supergroup, which is host to the majority of West African gold deposits. To date, several gold deposits have been identified on the Project; currently, Mineral Resources have been declared for Dugbe F and Tuzon. The deposits are located within 4km of the Dugbe Shear Zone which is thought to have played a role in large scale gold mineralization in the area. A large amount of exploration in the area was conducted by Hummingbird including 74,497m of diamond coring. 70,700m of this was at the Dugbe F and Tuzon deposits, discovered by Hummingbird in 2009 and 2011 respectively. Both deposits outcrop at surface and may be amenable to open-cut mining. Since executing the joint venture agreement in 2020, Pasofino has drilled an additional 14,584m at Dugbe F and Tuzon.

In addition, there are a number of prospects within the Project, including 'Sackor' where gold mineralization has been intersected in drill-holes and where additional drilling is planned. No other prospects have been drill-tested to date. At some prospects extensive trenching identified anomalous levels of gold that require drill-testing. An aggressive exploration program to test the prospects by the Company is ongoing. In 2019, Hummingbird signed a 25-year Mineral Development Agreement (MDA) with the Government of Liberia providing the necessary long-term framework and stabilization of taxes and duties. Under the terms of the MDA, the royalty rate on gold production is 3%, the income tax rate payable is 25% (with credit given for historic exploration expenditures), the fuel duty is reduced by 50%, and the Government of Liberia is granted a free carried interest of 10% in the Project.

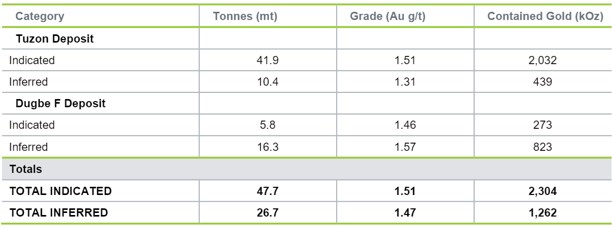

Table 6: Mineral Resource Estimate for the Dugbe Gold Project using a 0.5 g/t Au cut-off grade

| Category | Tonnes (million) | Au Grade (g/t) | Contained Gold (000 ounces) |

| Tuzon Deposit | |||

| Indicated | 41.9 | 1.51 | 2,032 |

| Inferred | 10.4 | 1.31 | 439 |

| Dugbe F Deposit | |||

| Indicated | 5.8 | 1.46 | 273 |

| Inferred | 16.3 | 1.57 | 823 |

| Totals | |||

| TOTAL INDICATED | 47.7 | 1.51 | 2,304 |

| TOTAL INFERRED | 26.7 | 1.47 | 1,262 |

Notes:

- Rounding errors may be evident when combining totals in the table but are immaterial.

- The effective date of the Mineral Resource Estimate is August 19, 2020 as reported in "Dugbe Gold Project, Liberia NI 43-101 Technical Report, Effective Date 19 August 2020," a report prepared by SRK Consulting (UK) Limited.

- The Qualified Person is Mr. Martin Pittuck (CEng, MIMMM).

- The Mineral Resource has been classified under the guidelines of the Canadian Institute of Mining, Metallurgy and Petroleum (CIM) Standards on Mineral Resources and Reserves, Definitions and Guidelines prepared by the CIM Standing Committee on Reserve Definitions and adopted by CIM Council (2014), and procedures for classifying the reported Mineral Resources were undertaken within the context of the Canadian Securities Administrators National Instrument 43-101 (NI 43-101).

- The estimates are stated using a 0.5 g/t Au cut-off grade.

- Mineral Resources are not Mineral Reserves and have no demonstrated economic viability. The estimate of Mineral Resources may be materially affected by environmental, permitting, legal, marketing, or other relevant issues.

- Mineral Resource estimates are stated within conceptual pit shells that have been used to define Reasonable Prospects for Eventual Economic Extraction (RPEEE). The pit shells used the following main parameters: (i) Au price of USD1,700/ounce; (ii) plant recovery of 88%; and (iii) mean specific gravity of 2.78 t/m3 for fresh rock and 1.56 t/m3 for oxide material for Tuzon, and for Dugbe F a mean specific gravity of 2.73t/m3.

ABOUT PASOFINO GOLD LTD.

Pasofino Gold Ltd. is a Canadian-based mineral exploration company listed on the TSX-V (VEIN). Pasofino, through its wholly-owned subsidiary, is earning a 49% economic interest (prior to the issuance of the Government of Liberia's 10% carried interest) in the Dugbe Gold Project.

For further information, please visit www.pasofinogold.com or contact:

Ian Stalker, President & CEO

T: 604 367 8110

E: istalker@pasofinogold.com

NATIONAL INSTRUMENT 43-101 TECHNICAL REPORT

A technical report for the Dugbe Gold Project will be prepared in accordance with National Instrument 43-101 and will be filed on SEDAR at www.sedar.com and on the Company's website at www.pasofinogold.com within 45 days of this news release. Readers are encouraged to read the technical report in its entirety, including all qualifications, assumptions and exclusions that relate to the details summarized in this news release. The technical report is intended to be read as a whole, and sections should not be read or relied upon out of context.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

CAUTIONARY STATEMENTS REGARDING FORWARD-LOOKING STATEMENTS

This news release contains "forward-looking statements" that are based on expectations, estimates, projections and interpretations as at the date of this news release. Forward-looking statements are frequently characterized by words such as "plan", "expect", "project", "seek", "intend", "believe", "anticipate", "estimate", "suggest", "indicate" and other similar words or statements that certain events or conditions "may" or "will" occur, and include, without limitation, statements regarding the ability to raise the funds to finance its ongoing business activities including the acquisition of mineral projects and the exploration and development of its projects. Such forward looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such risks and other factors may include, but are not limited to, the results of exploration activities; the ability of the Company to complete further exploration activities; timing and availability of external financing on acceptable terms and those risk factors outlined in the Company's Management Discussion and Analysis as filed on SEDAR. The Company does not undertake to update any forward-looking information except in accordance with applicable securities laws.

NON-GAAP MEASURES

This news release includes certain terms or performance measures commonly used in the mining industry that are not defined under International Financial Reporting Standards ("IFRS"), including cash costs and AISC per payable ounce of gold sold. Non-GAAP measures do not have any standardized meaning prescribed under IFRS and, therefore, they may not be comparable to similar measures employed by other companies. We believe that, in addition to conventional measures prepared in accordance with IFRS, certain investors use this information to evaluate our performance. The data presented is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

[1] Cash costs per payable ounce and AISC per payable ounce are non-GAAP financial measures. Please see "Cautionary Note Regarding Non-GAAP Measures". AISC per payable ounce includes all mining costs, processing costs, mine level G&A, royalties, sustaining capital and closure costs. Cash costs per payable ounce includes all mining costs, processing costs, mine level G&A, and royalties.

[2] Includes bulk infrastructure and re-settlement costs.

![]()

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/88534