Looking back on healthcare technology stocks’ Q2 earnings, we examine this quarter’s best and worst performers, including Tandem Diabetes (NASDAQ: TNDM) and its peers.

Healthcare Technology

The 8 healthcare technology stocks we track reported a mixed Q2. As a group, revenues beat analysts’ consensus estimates by 2.4% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 7.1% on average since the latest earnings results.

Tandem Diabetes (NASDAQ: TNDM)

With technology that automatically adjusts insulin delivery based on continuous glucose monitoring data, Tandem Diabetes Care (NASDAQ: TNDM) develops and manufactures automated insulin delivery systems that help people with diabetes manage their blood glucose levels.

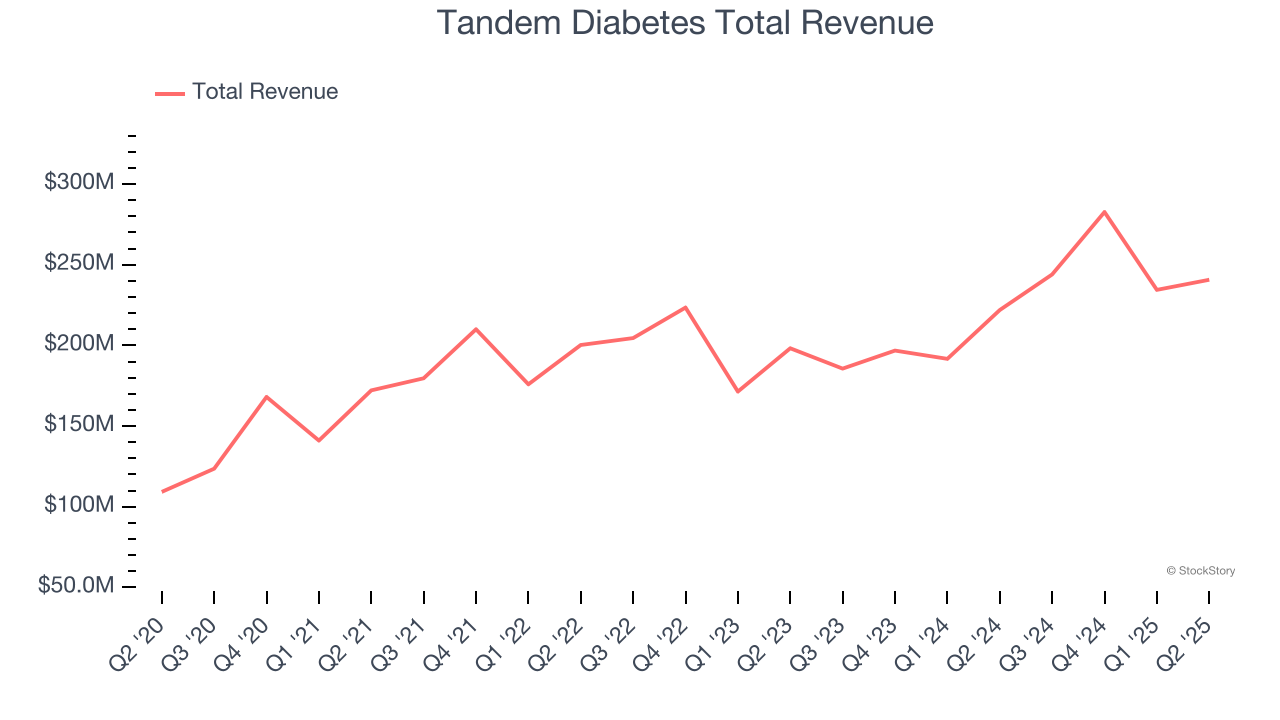

Tandem Diabetes reported revenues of $240.7 million, up 8.5% year on year. This print exceeded analysts’ expectations by 1.5%. Despite the top-line beat, it was still a slower quarter for the company with a significant miss of analysts’ EPS estimates and full-year revenue guidance meeting analysts’ expectations.

Interestingly, the stock is up 2.2% since reporting and currently trades at $14.77.

Read our full report on Tandem Diabetes here, it’s free for active Edge members.

Best Q2: Omnicell (NASDAQ: OMCL)

Driven by the vision of an "Autonomous Pharmacy" with zero medication errors, Omnicell (NASDAQ: OMCL) provides medication management automation and adherence tools that help healthcare systems and pharmacies reduce errors and improve efficiency.

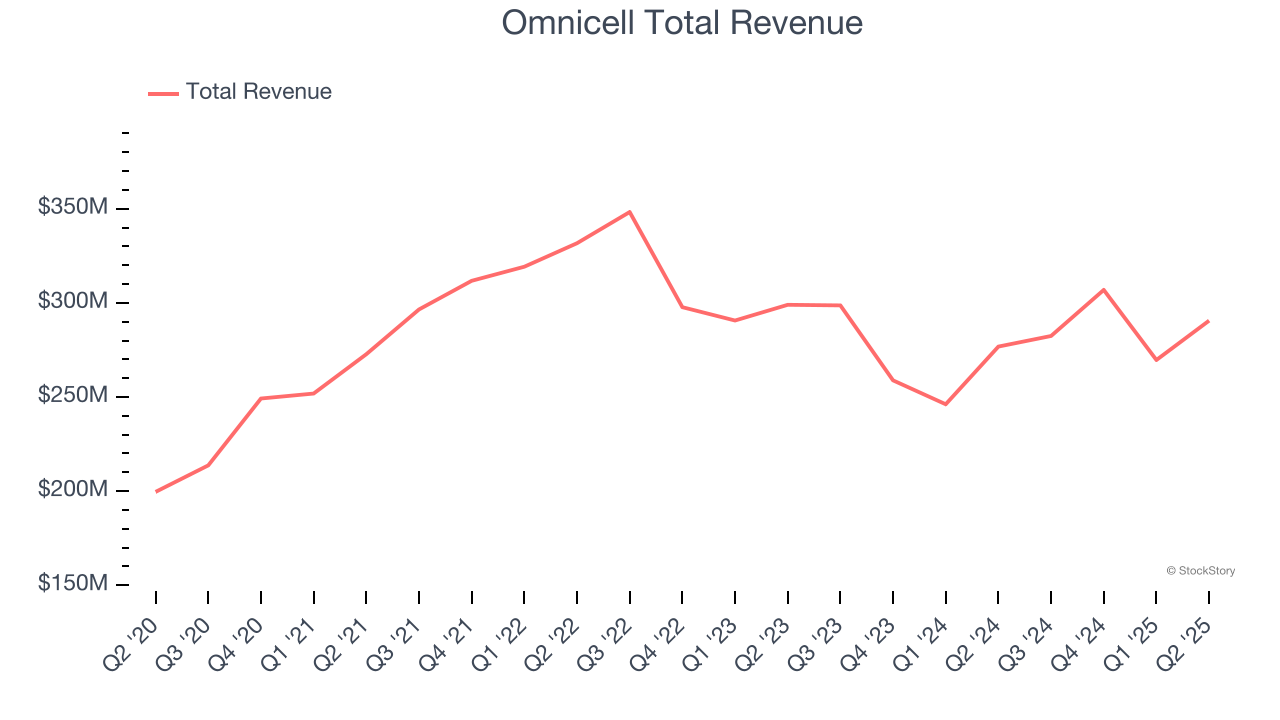

Omnicell reported revenues of $290.6 million, up 5% year on year, outperforming analysts’ expectations by 4.9%. The business had a very strong quarter with a beat of analysts’ EPS estimates and an impressive beat of analysts’ full-year EPS guidance estimates.

The market seems content with the results as the stock is up 4.6% since reporting. It currently trades at $31.10.

Is now the time to buy Omnicell? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q2: GoodRx (NASDAQ: GDRX)

Started in 2011 to tackle the problem of high prescription drug costs in America, GoodRx (NASDAQ: GDRX) operates a digital platform that helps consumers find lower prices on prescription medications through price comparison tools and discount codes.

GoodRx reported revenues of $203.1 million, up 1.2% year on year, falling short of analysts’ expectations by 1.3%. It was a disappointing quarter as it posted EPS in line with analysts’ estimates and a significant miss of analysts’ customer base estimates.

As expected, the stock is down 9.8% since the results and currently trades at $3.92.

Read our full analysis of GoodRx’s results here.

Privia Health (NASDAQ: PRVA)

Operating in 13 states and the District of Columbia with over 4,300 providers serving more than 4.8 million patients, Privia Health (NASDAQ: PRVA) is a technology-driven company that helps physicians optimize their practices, improve patient experiences, and transition to value-based care models.

Privia Health reported revenues of $521.2 million, up 23.4% year on year. This print surpassed analysts’ expectations by 10.9%. It was a strong quarter as it also recorded a solid beat of analysts’ revenue estimates and a beat of analysts’ EPS estimates.

Privia Health delivered the biggest analyst estimates beat but had the weakest full-year guidance update among its peers. The stock is up 33.3% since reporting and currently trades at $26.39.

Read our full, actionable report on Privia Health here, it’s free for active Edge members.

Premier (NASDAQ: PINC)

Operating one of the largest healthcare group purchasing organizations in the United States with over 4,350 hospital members, Premier (NASDAQ: PINC) is a technology-driven healthcare improvement company that helps hospitals, health systems, and other providers reduce costs and improve clinical outcomes.

Premier reported revenues of $262.9 million, down 12.5% year on year. This number beat analysts’ expectations by 5%. Overall, it was a strong quarter as it also produced a beat of analysts’ EPS estimates and an impressive beat of analysts’ revenue estimates.

The stock is up 15% since reporting and currently trades at $28.12.

Read our full, actionable report on Premier here, it’s free for active Edge members.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.