Shopify has had an impressive run over the past six months. While the S&P 500 has been flat, the stock has returned 28.8% and now trades at $104.01. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now still a good time to buy SHOP? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Are We Positive On SHOP?

Originally created as an internal tool for a snowboarding company, Shopify (NYSE: SHOP) provides a software platform for building and operating e-commerce businesses.

1. TPV Surges as Payment Activity Increases

TPV, or total processing volume, is the aggregate dollar value of transactions flowing through Shopify’s platform. This is the number from which the company will ultimately collect fees, and the higher it is, the more chances Shopify has to upsell additional services (like banking).

Shopify’s TPV punched in at $61 billion in Q4, and over the last four quarters, its year-on-year growth averaged 32%. This performance was fantastic and shows the company is capturing significant demand on its platform. It also indicates that customers are highly active and engaged, driving higher transaction volumes and allowing Shopify to collect more fees.

2. Customer Acquisition Costs Are Recovered in Record Time

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Shopify is extremely efficient at acquiring new customers, and its CAC payback period checked in at 6.4 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Shopify more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

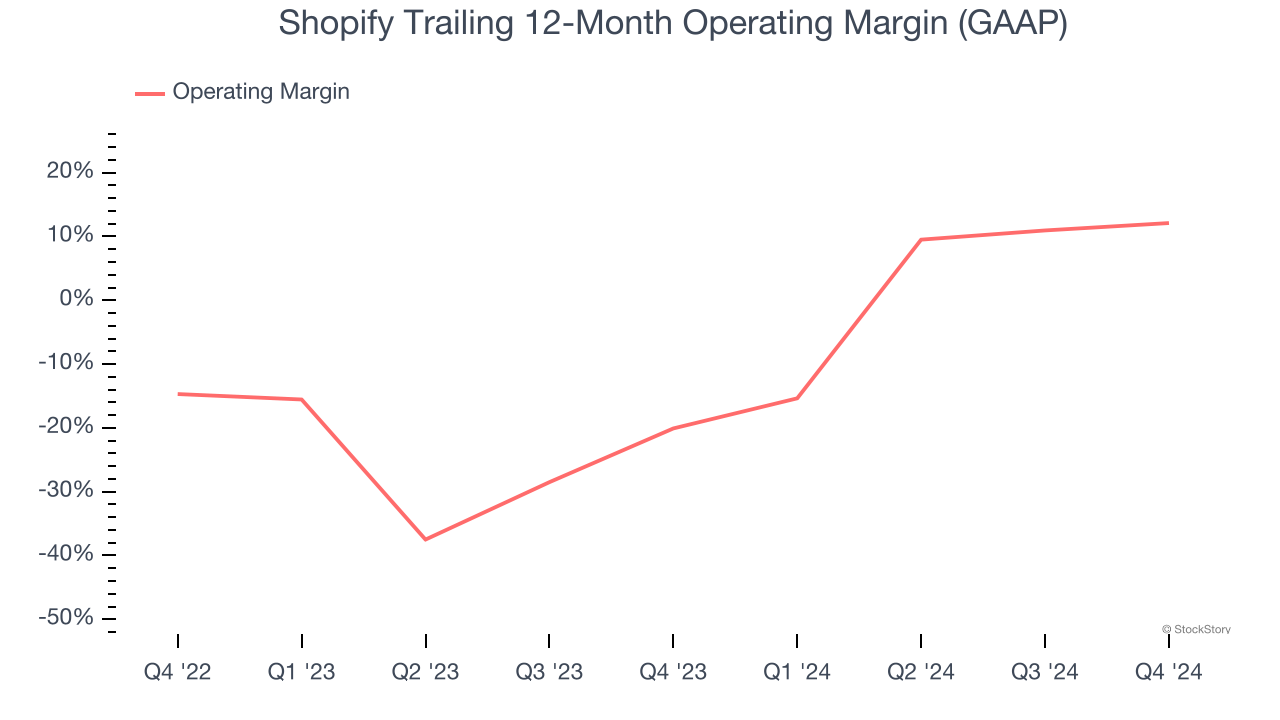

3. Operating Margin Rising, Profits Up

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Looking at the trend in its profitability, Shopify’s operating margin rose by 32.2 percentage points over the last year, as its sales growth gave it immense operating leverage. Its operating margin for the trailing 12 months was 12.1%.

Final Judgment

These are just a few reasons why we think Shopify is a high-quality business, and with its shares beating the market recently, the stock trades at 12.4× forward price-to-sales (or $104.01 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Shopify

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.