Fastenal’s 26.7% return over the past six months has outpaced the S&P 500 by 21.4%, and its stock price has climbed to $46.77 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Fastenal, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Fastenal Not Exciting?

We’re glad investors have benefited from the price increase, but we don't have much confidence in Fastenal. Here are three reasons why you should be careful with FAST and a stock we'd rather own.

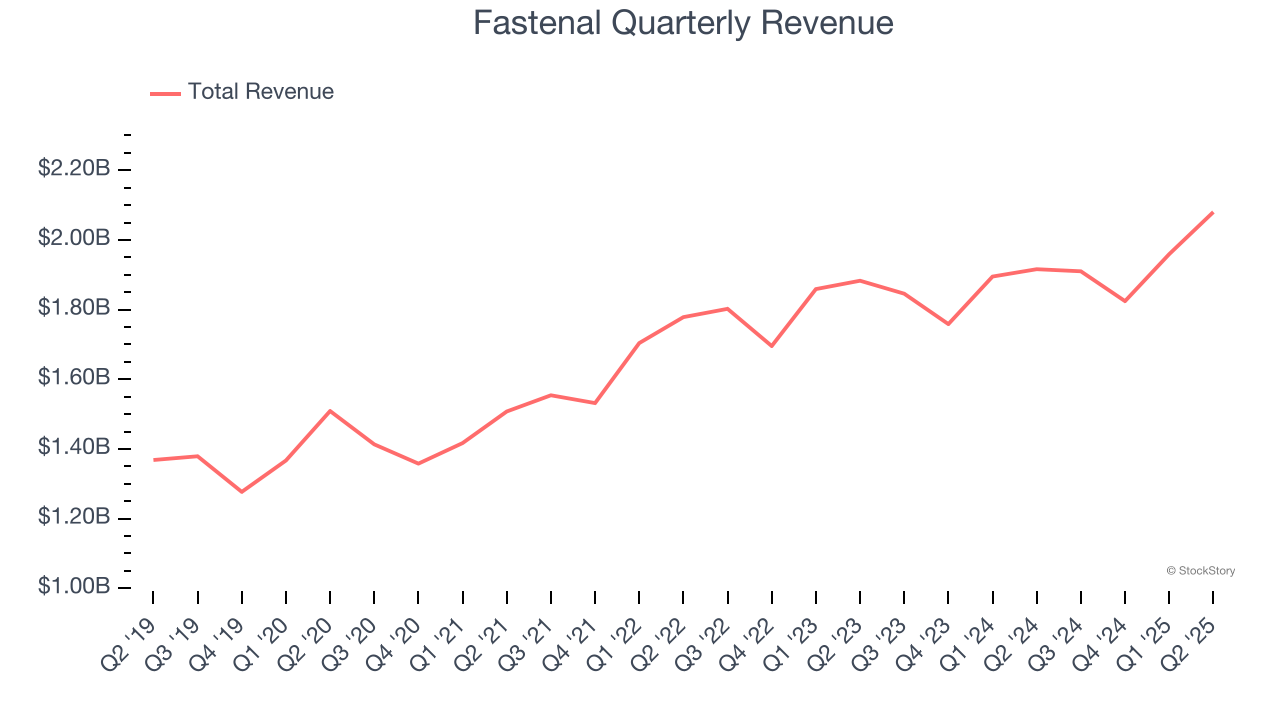

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Fastenal’s 7% annualized revenue growth over the last five years was mediocre. This was below our standard for the industrials sector.

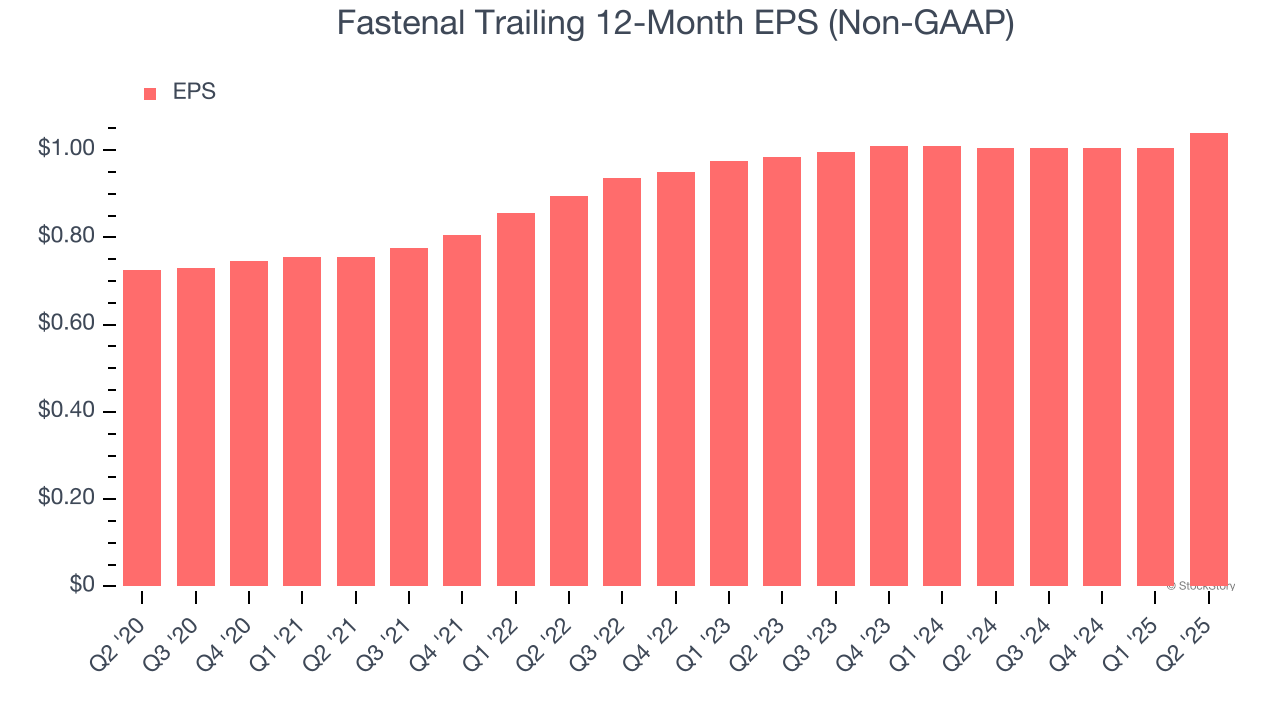

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Fastenal’s unimpressive 7.5% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

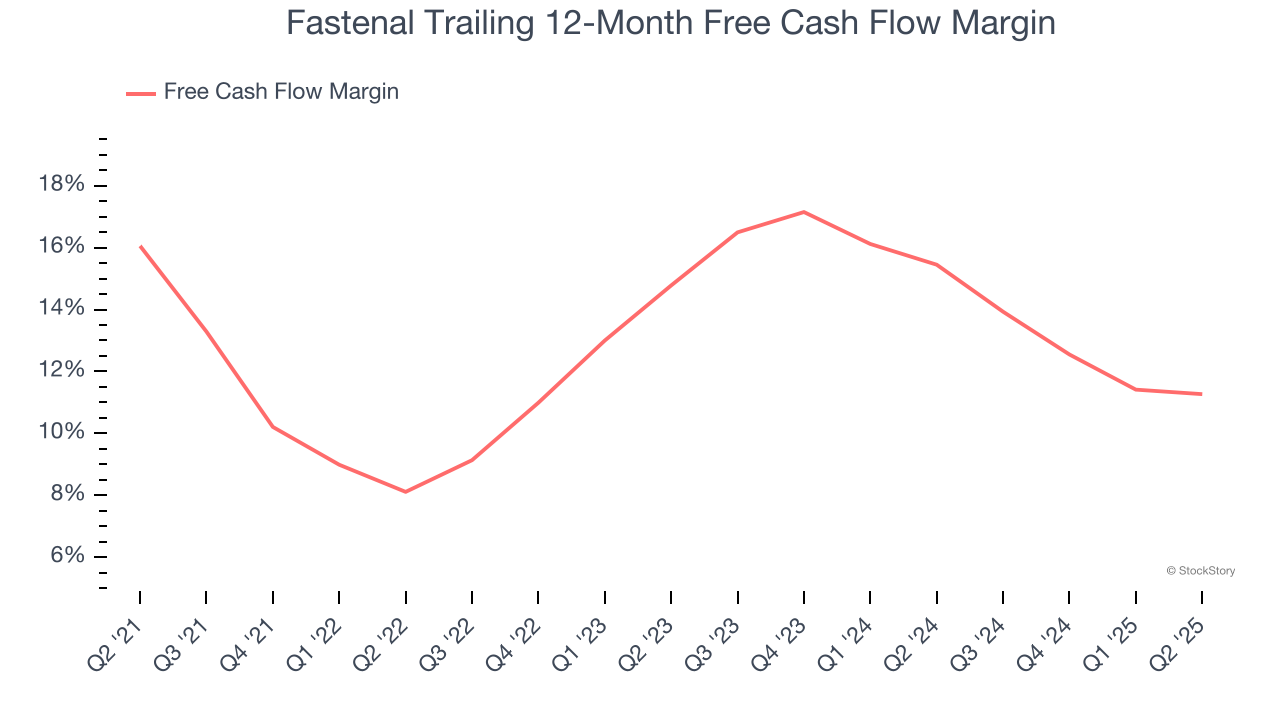

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Fastenal’s margin dropped by 4.8 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Fastenal’s free cash flow margin for the trailing 12 months was 11.3%.

Final Judgment

Fastenal isn’t a terrible business, but it isn’t one of our picks. With its shares topping the market in recent months, the stock trades at 43.5× forward P/E (or $46.77 per share). At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment. Let us point you toward a top digital advertising platform riding the creator economy.

Stocks We Like More Than Fastenal

When Trump unveiled his aggressive tariff plan in April 2024, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.