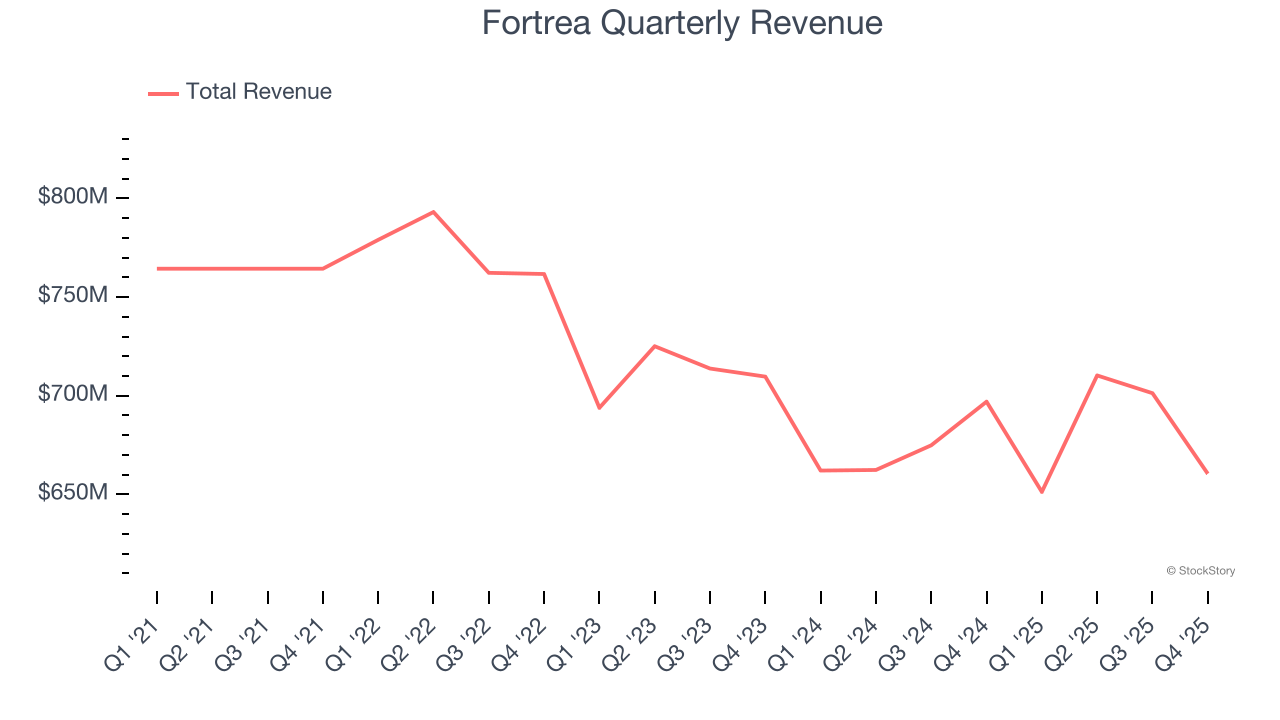

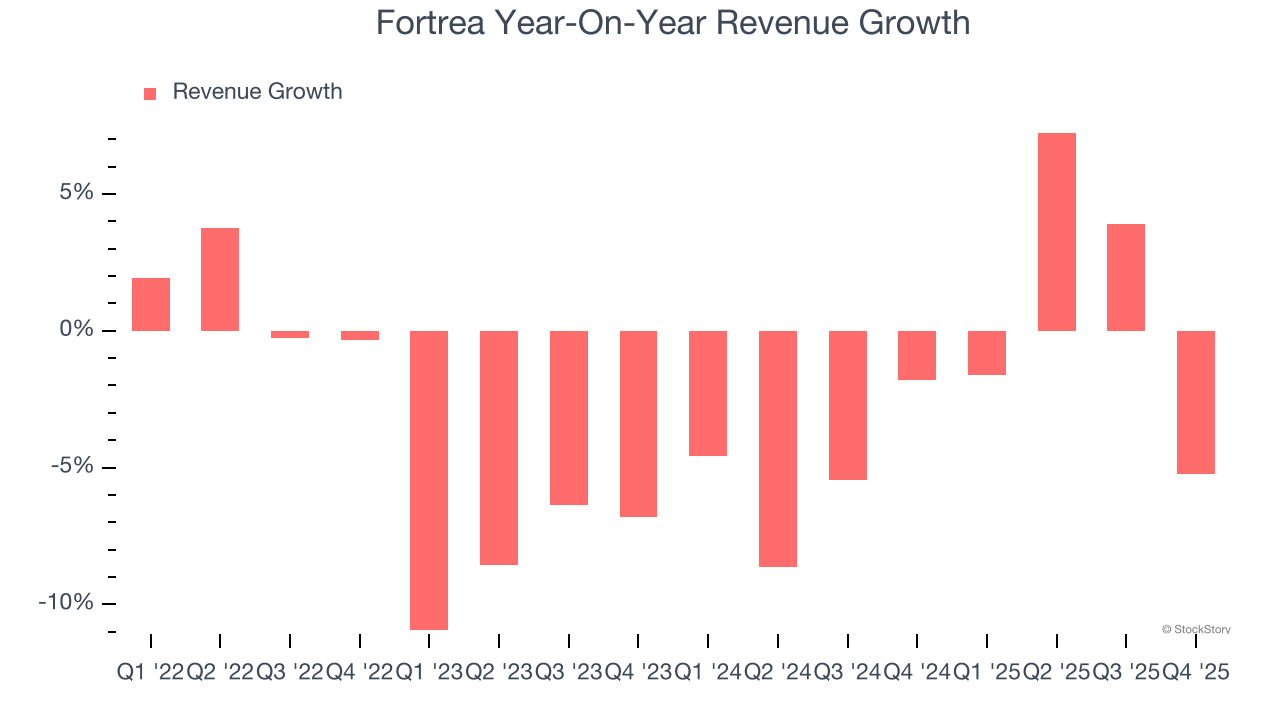

Clinical research company Fortrea Holdings (NASDAQ: FTRE) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 5.2% year on year to $660.5 million. The company’s full-year revenue guidance of $2.6 billion at the midpoint came in 4.9% below analysts’ estimates. Its non-GAAP profit of $0.09 per share was 43.8% below analysts’ consensus estimates.

Is now the time to buy Fortrea? Find out by accessing our full research report, it’s free.

Fortrea (FTRE) Q4 CY2025 Highlights:

- Revenue: $660.5 million vs analyst estimates of $666.8 million (5.2% year-on-year decline, 0.9% miss)

- Adjusted EPS: $0.09 vs analyst expectations of $0.16 (43.8% miss)

- Adjusted EBITDA: $54 million vs analyst estimates of $50.09 million (8.2% margin, 7.8% beat)

- EBITDA guidance for the upcoming financial year 2026 is $205 million at the midpoint, in line with analyst expectations

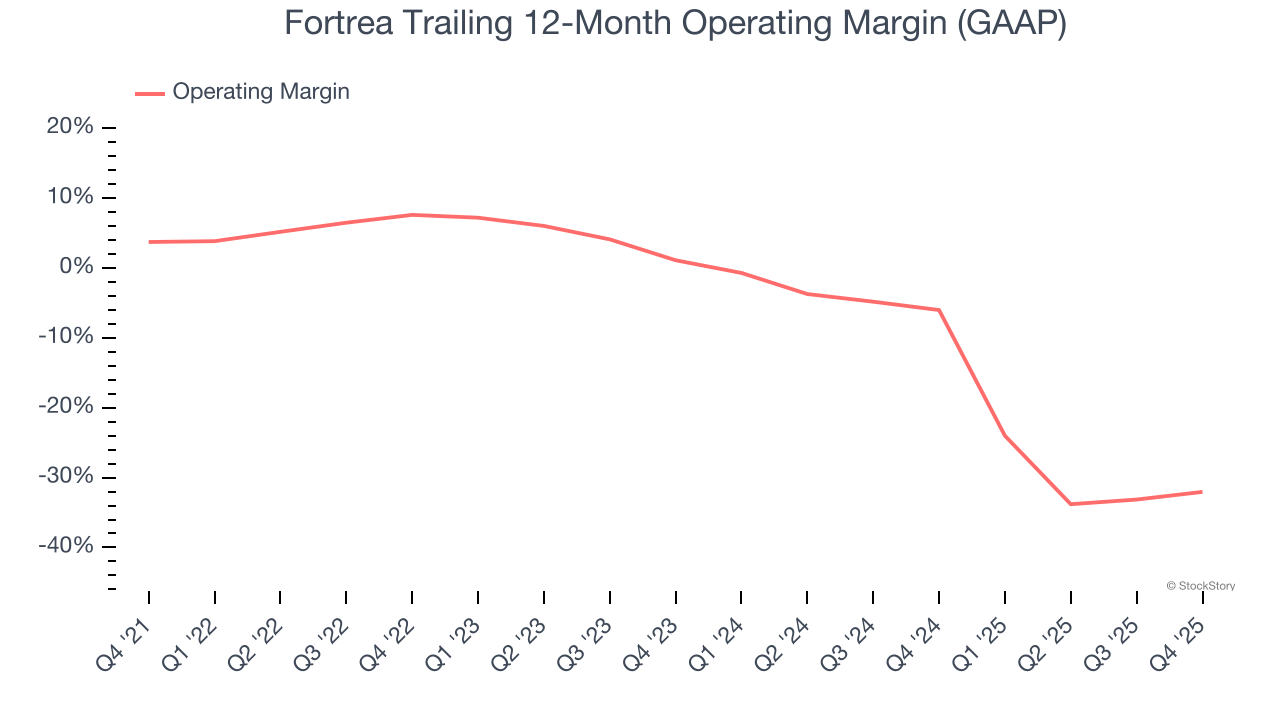

- Operating Margin: -2.1%, up from -8% in the same quarter last year

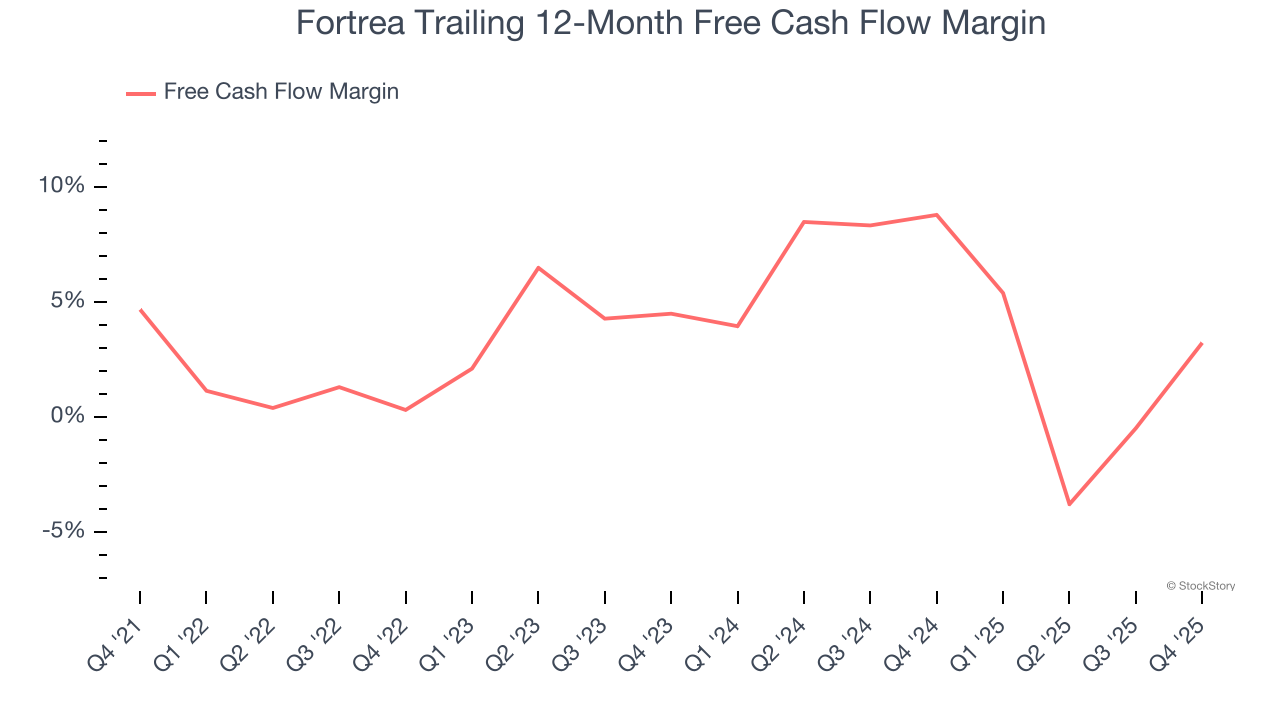

- Free Cash Flow Margin: 18.4%, up from 2.9% in the same quarter last year

- Market Capitalization: $955.4 million

“We finished 2025 with solid results for the fourth quarter, as the Fortrea team’s shared commitment to commercial, operational and financial excellence becomes embedded in our way of working,” said Anshul Thakral, CEO of Fortrea.

Company Overview

Spun off from Labcorp in 2023 to focus exclusively on clinical research services, Fortrea (NASDAQ: FTRE) is a contract research organization that helps pharmaceutical, biotech, and medical device companies develop and bring their products to market through clinical trials and support services.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last four years, Fortrea’s demand was weak and its revenue declined by 2.9% per year. This was below our standards and suggests it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a stretched historical view may miss recent innovations or disruptive industry trends. Fortrea’s annualized revenue declines of 2.1% over the last two years align with its four-year trend, suggesting its demand has consistently shrunk.

This quarter, Fortrea missed Wall Street’s estimates and reported a rather uninspiring 5.2% year-on-year revenue decline, generating $660.5 million of revenue.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Fortrea’s high expenses have contributed to an average operating margin of negative 4.5% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, Fortrea’s operating margin decreased by 35.8 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 33.2 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Fortrea generated a negative 2.1% operating margin. The company's consistent lack of profits raise a flag.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Fortrea has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.2%, subpar for a healthcare business.

Taking a step back, we can see that Fortrea’s margin dropped by 1.4 percentage points during that time. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s in the middle of an investment cycle.

Fortrea’s free cash flow clocked in at $121.6 million in Q4, equivalent to a 18.4% margin. This result was good as its margin was 15.5 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

Key Takeaways from Fortrea’s Q4 Results

We struggled to find many positives in these results. Its full-year revenue guidance missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 1.4% to $10.20 immediately following the results.

The latest quarter from Fortrea’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).