Revolve’s 28.4% return over the past six months has outpaced the S&P 500 by 24.9%, and its stock price has climbed to $25.73 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Revolve, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think Revolve Will Underperform?

Despite the momentum, we're cautious about Revolve. Here are three reasons there are better opportunities than RVLV and a stock we'd rather own.

1. Change in Active Customers Points to Soft Demand

As an online retailer, Revolve generates revenue growth by expanding its number of users and the average order size in dollars.

Over the last two years, Revolve’s active customers , a key performance metric for the company, increased by 5.4% annually to 2.84 million in the latest quarter. This growth rate lags behind the hottest consumer internet applications. If Revolve wants to accelerate growth, it likely needs to engage users more effectively with its existing offerings or innovate with new products.

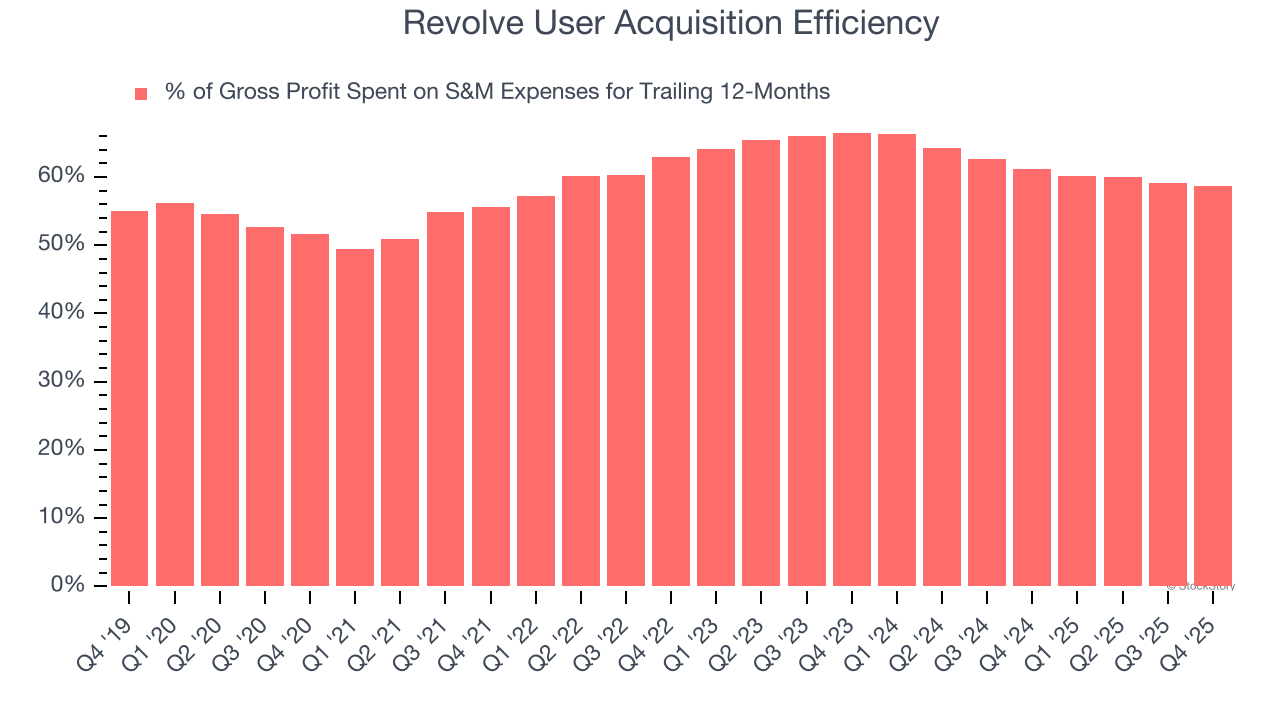

2. Poor Marketing Efficiency Drains Profits

Unlike enterprise software that’s typically sold by dedicated sales teams, consumer internet businesses like Revolve grow from a combination of product virality, paid advertisement, and incentives.

It’s expensive for Revolve to acquire new users as the company has spent 58.7% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates that Revolve’s product offering can be easily replicated and that it must continue investing to maintain an acceptable growth trajectory.

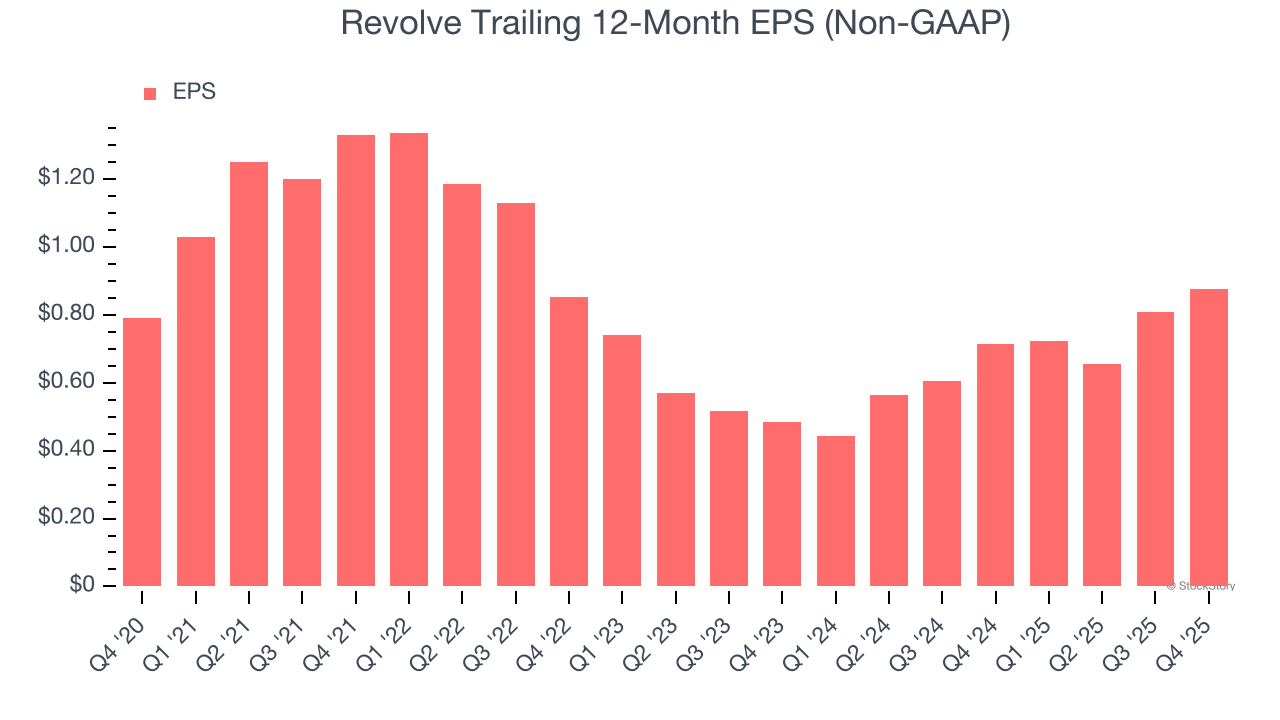

3. EPS Growth Has Stalled

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Revolve’s flat EPS over the last three years was below its 3.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Revolve doesn’t pass our quality test. With its shares outperforming the market lately, the stock trades at 15.8× forward EV/EBITDA (or $25.73 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. We’d suggest looking at our favorite semiconductor picks and shovels play.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.