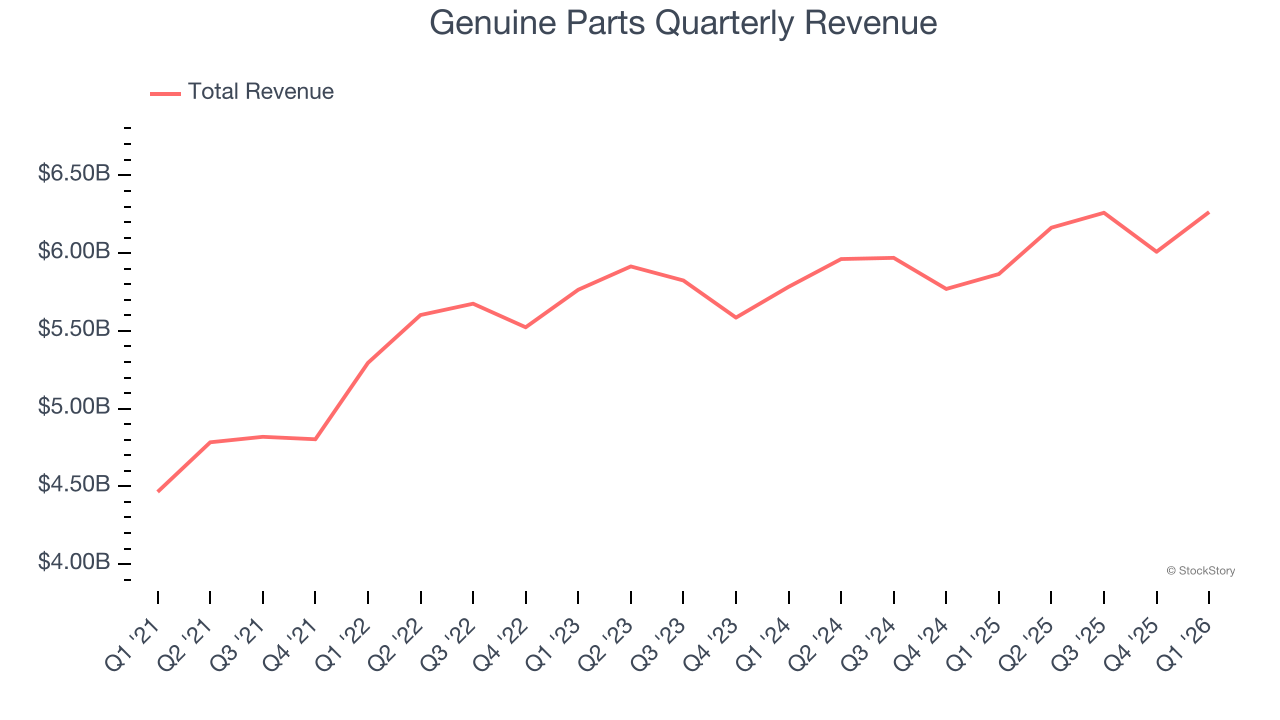

Auto and industrial parts retailer Genuine Parts (NYSE: GPC) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 6.8% year on year to $6.26 billion. Its non-GAAP profit of $1.77 per share was 1.3% above analysts’ consensus estimates.

Is now the time to buy Genuine Parts? Find out by accessing our full research report, it’s free.

Genuine Parts (GPC) Q1 CY2026 Highlights:

- Revenue: $6.26 billion vs analyst estimates of $6.18 billion (6.8% year-on-year growth, 1.4% beat)

- Adjusted EPS: $1.77 vs analyst estimates of $1.75 (1.3% beat)

- Adjusted EBITDA: $429.5 million vs analyst estimates of $493.3 million (6.9% margin, 12.9% miss)

- Management reiterated its full-year Adjusted EPS guidance of $7.75 at the midpoint

- Operating Margin: 4.6%, in line with the same quarter last year

- Free Cash Flow was -$33.64 million compared to -$160.7 million in the same quarter last year

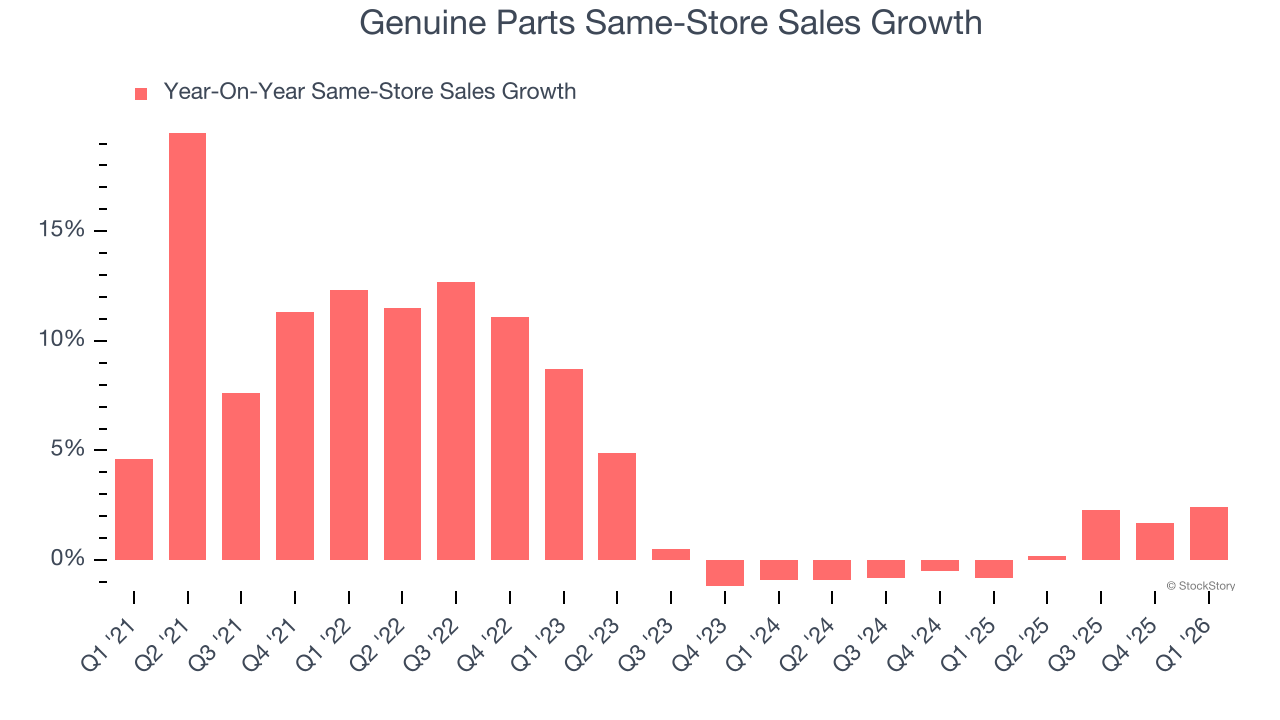

- Same-Store Sales rose 2.4% year on year (-0.8% in the same quarter last year)

- Market Capitalization: $15.66 billion

"The GPC team delivered first quarter results ahead of expectations, driven by solid sales growth and operating discipline across our business segments," said Will Stengel, Chair-Elect and Chief Executive Officer.

Company Overview

Largely targeting the professional customer, Genuine Parts (NYSE: GPC) sells auto and industrial parts such as batteries, belts, bearings, and machine fluids.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $24.7 billion in revenue over the past 12 months, Genuine Parts is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there are only a finite number of places to build new stores, making it harder to find incremental growth. To accelerate sales, Genuine Parts likely needs to optimize its pricing or lean into international expansion.

As you can see below, Genuine Parts’s 3.1% annualized revenue growth over the last three years was sluggish. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

This quarter, Genuine Parts reported year-on-year revenue growth of 6.8%, and its $6.26 billion of revenue exceeded Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 3.7% over the next 12 months, similar to its three-year rate. This projection is above the sector average and suggests its newer products will help maintain its historical top-line performance.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Same-Store Sales

Same-store sales show the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

Genuine Parts’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat.

In the latest quarter, Genuine Parts’s same-store sales rose 2.4% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

Key Takeaways from Genuine Parts’s Q1 Results

It was good to see Genuine Parts narrowly top analysts’ revenue expectations this quarter. On the other hand, its EBITDA missed. Overall, this was a weaker quarter. The stock traded down 1.4% to $111.00 immediately after reporting.

Genuine Parts’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).