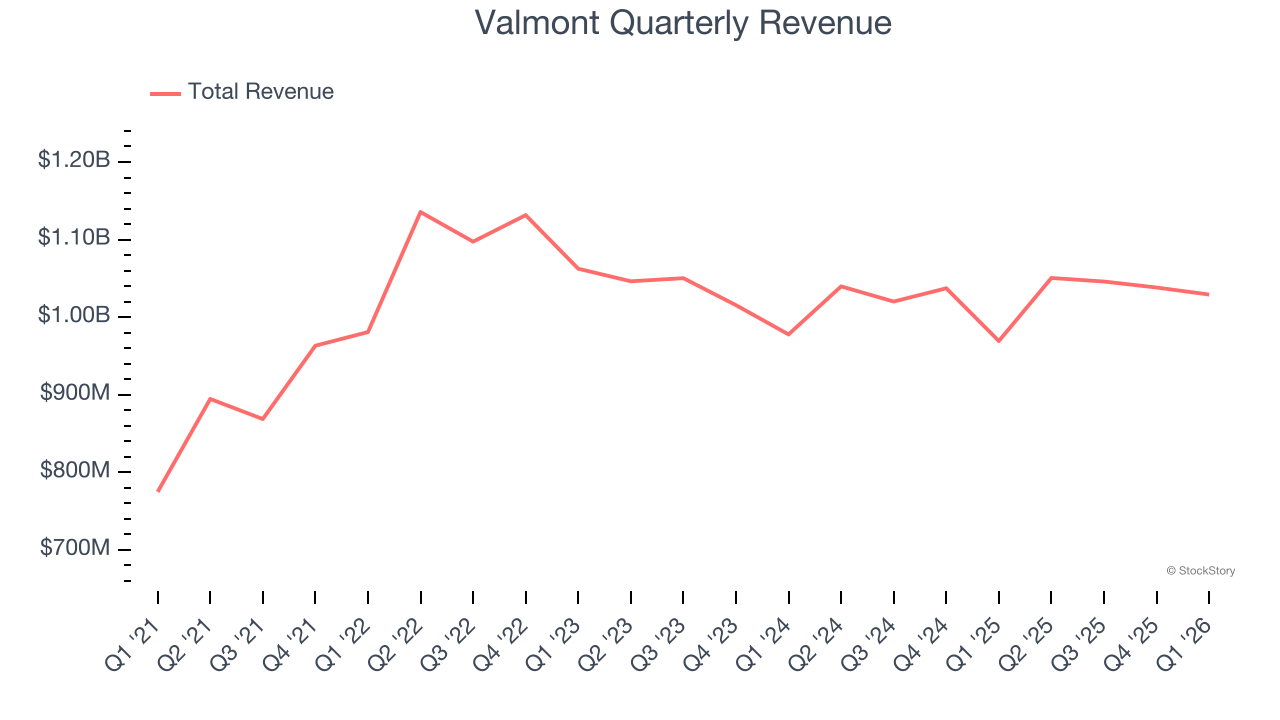

Infrastructure and agriculture equipment manufacturer Valmont Industries (NYSE: VMI) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 6.2% year on year to $1.03 billion. The company expects the full year’s revenue to be around $4.3 billion, close to analysts’ estimates. Its GAAP profit of $5.51 per share was 18.1% above analysts’ consensus estimates.

Is now the time to buy Valmont? Find out by accessing our full research report, it’s free.

Valmont (VMI) Q1 CY2026 Highlights:

- Revenue: $1.03 billion vs analyst estimates of $998.8 million (6.2% year-on-year growth, 3% beat)

- EPS (GAAP): $5.51 vs analyst estimates of $4.67 (18.1% beat)

- Adjusted EBITDA: $178.2 million vs analyst estimates of $163.3 million (17.3% margin, 9.1% beat)

- The company reconfirmed its revenue guidance for the full year of $4.3 billion at the midpoint

- EPS (GAAP) guidance for the full year is $22.50 at the midpoint, beating analyst estimates by 2.8%

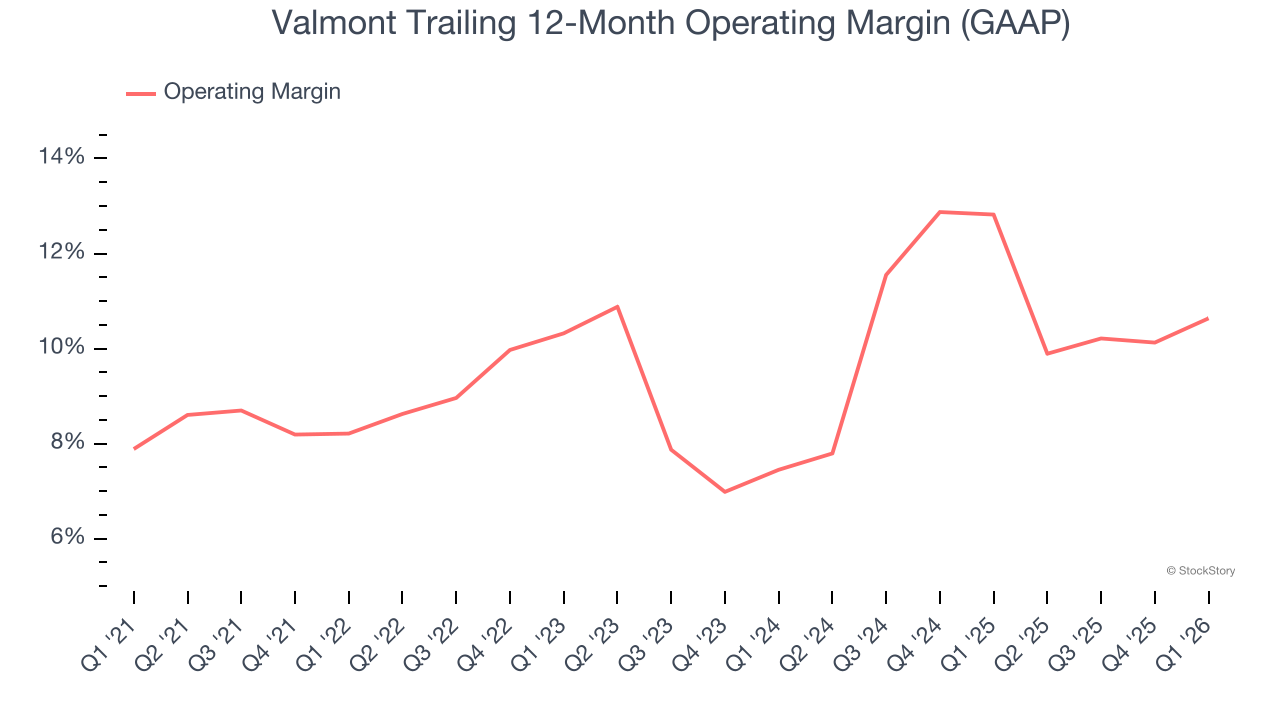

- Operating Margin: 15.1%, up from 13.2% in the same quarter last year

- Free Cash Flow Margin: 6.7%, up from 3.6% in the same quarter last year

- Backlog: $1.65 billion at quarter end, up 11.1% year on year

- Market Capitalization: $8.01 billion

President and Chief Executive Officer Avner M. Applbaum commented, “We delivered a strong start to 2026, including record first-quarter earnings per share, reflecting solid sales growth and margin expansion driven primarily by pricing strength and higher volumes in North America Utility. This performance reflects the team’s focus on value-based pricing, a disciplined commercial approach, and continued progress on our capacity and throughput initiatives. We are advancing our strategy and key value drivers to support sustainable growth and long-term shareholder value.

Company Overview

Credited with an invention in the 1950s that improved crop yields, Valmont (NYSE: VMI) provides engineered products and infrastructure services for the agricultural industry.

Revenue Growth

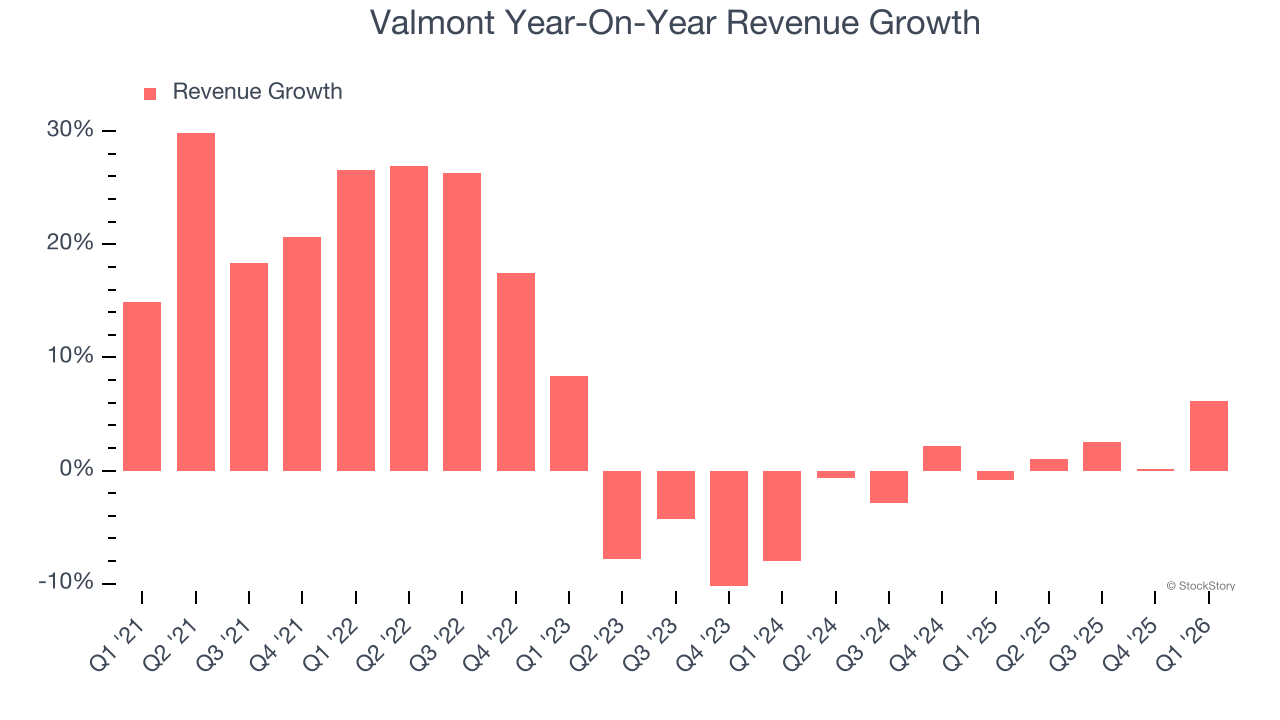

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Regrettably, Valmont’s sales grew at a mediocre 6.8% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the industrials sector, but there are still things to like about Valmont.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Valmont’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Valmont reported year-on-year revenue growth of 6.2%, and its $1.03 billion of revenue exceeded Wall Street’s estimates by 3%.

Looking ahead, sell-side analysts expect revenue to grow 4.3% over the next 12 months. Although this projection indicates its newer products and services will spur better top-line performance, it is still below the sector average. At least the company is tracking well in other measures of financial health.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Valmont has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 9.9%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, Valmont’s operating margin rose by 2.4 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Valmont generated an operating margin profit margin of 15.1%, up 1.9 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

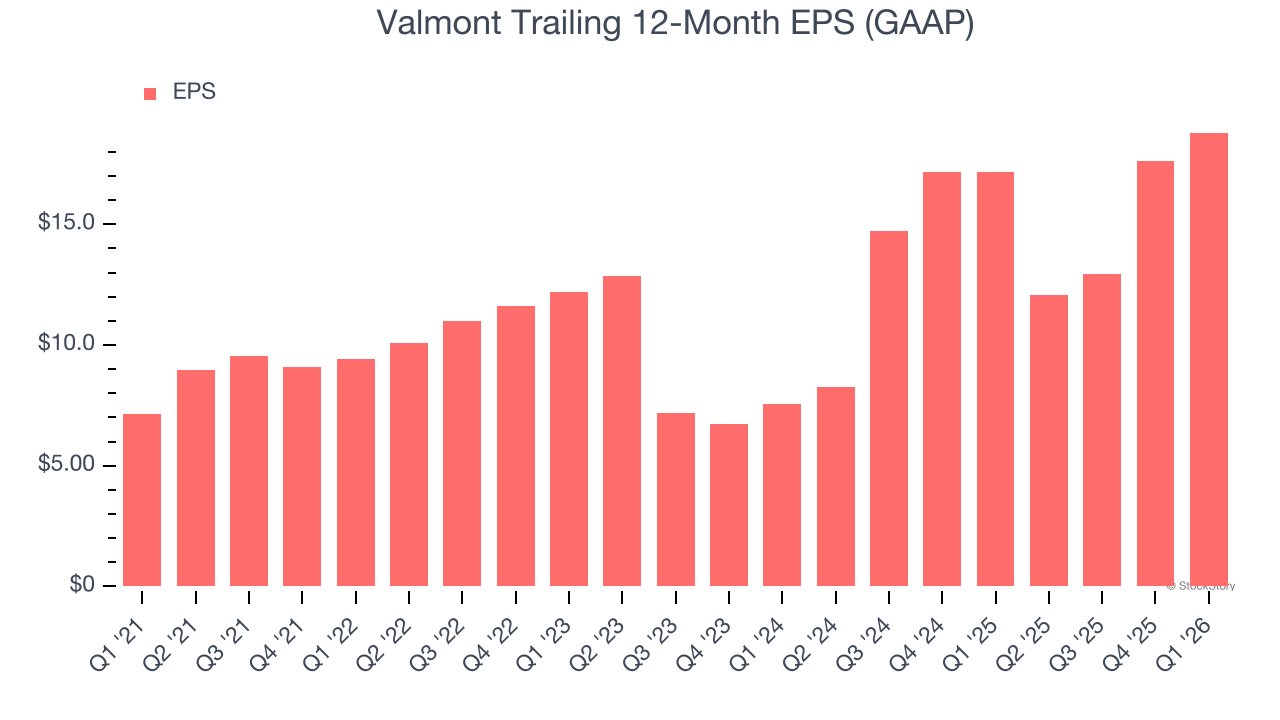

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Valmont’s EPS grew at 21.4% compounded annual growth rate over the last five years, higher than its 6.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

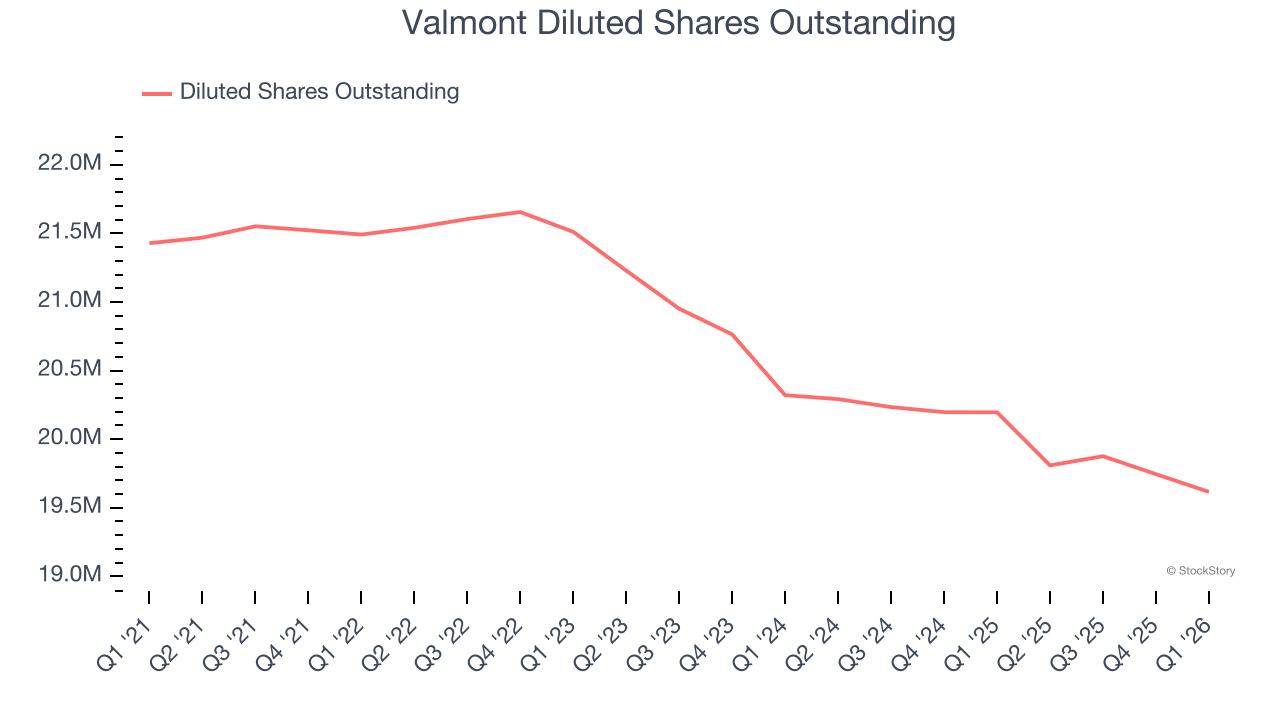

Diving into Valmont’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Valmont’s operating margin expanded by 2.4 percentage points over the last five years. On top of that, its share count shrank by 8.5%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Valmont, its two-year annual EPS growth of 57.6% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, Valmont reported EPS of $5.51, up from $4.32 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Valmont’s Q1 Results

We were impressed by how significantly Valmont blew past analysts’ EBITDA expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 5.4% to $431.94 immediately after reporting.

Indeed, Valmont had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).