Swimming pool distributor Pool (NASDAQ: POOL) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 6.2% year on year to $1.14 billion. Its GAAP profit of $1.45 per share was 6.7% above analysts’ consensus estimates.

Is now the time to buy Pool? Find out by accessing our full research report, it’s free.

Pool (POOL) Q1 CY2026 Highlights:

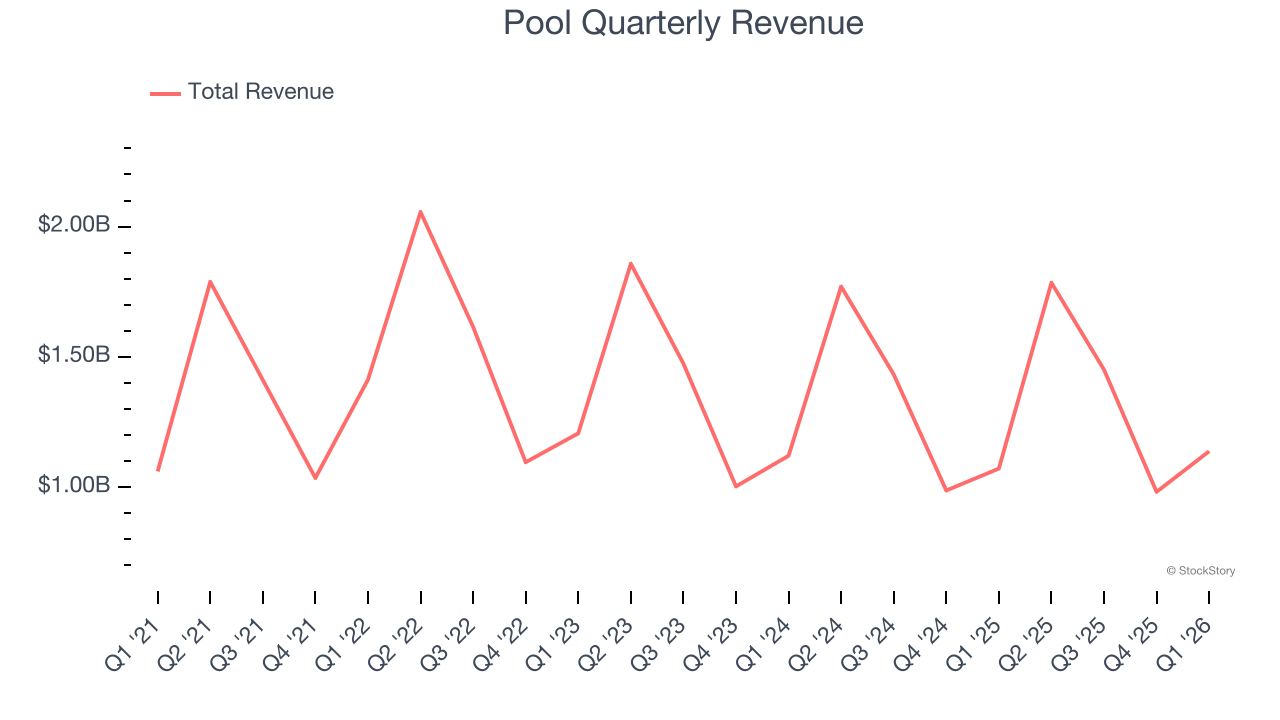

- Revenue: $1.14 billion vs analyst estimates of $1.10 billion (6.2% year-on-year growth, 3.8% beat)

- EPS (GAAP): $1.45 vs analyst estimates of $1.36 (6.7% beat)

- Adjusted EBITDA: $101.5 million vs analyst estimates of $97.51 million (8.9% margin, 4.1% beat)

- EPS (GAAP) guidance for the full year is $11.02 at the midpoint, roughly in line with what analysts were expecting

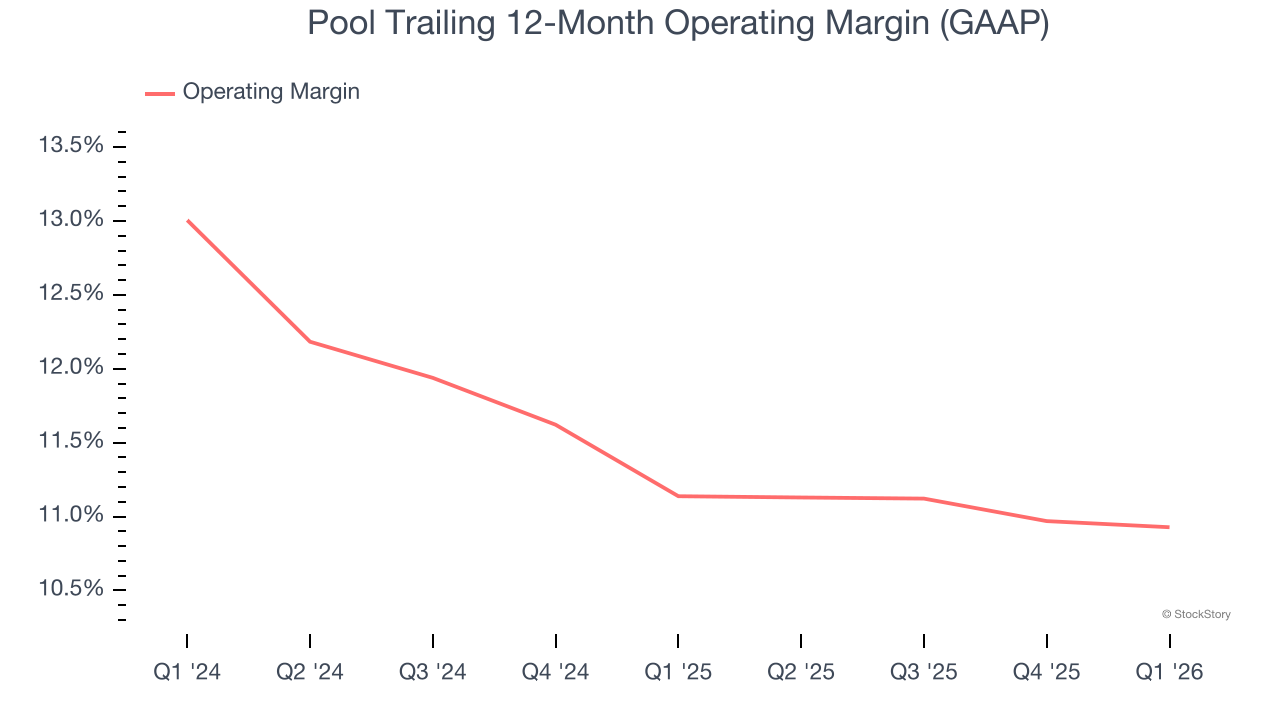

- Operating Margin: 7.3%, in line with the same quarter last year

- Free Cash Flow Margin: 1.5%, similar to the same quarter last year

- Market Capitalization: $8.60 billion

“We are off to a solid start in 2026, with net sales up 6% and operating income growing 7% year-over-year. Maintenance demand remained resilient, and we saw continued, though still gradual, recovery in discretionary categories. Gross margin reflected the typical first quarter seasonal mix, with strong equipment and customer early buy sales partially offset by our pricing and supply chain initiatives. Our greenfield investments are contributing to growth, and we are beginning to see operating expense leverage as those locations mature. We remain confident in our strategy and our ability to drive profitable growth,” said Peter D. Arvan, president and CEO.

Company Overview

Founded in 1993 and headquartered in Louisiana, Pool (NASDAQ: POOL) is one of the largest wholesale distributors of swimming pool supplies, equipment, and related leisure products.

Revenue Growth

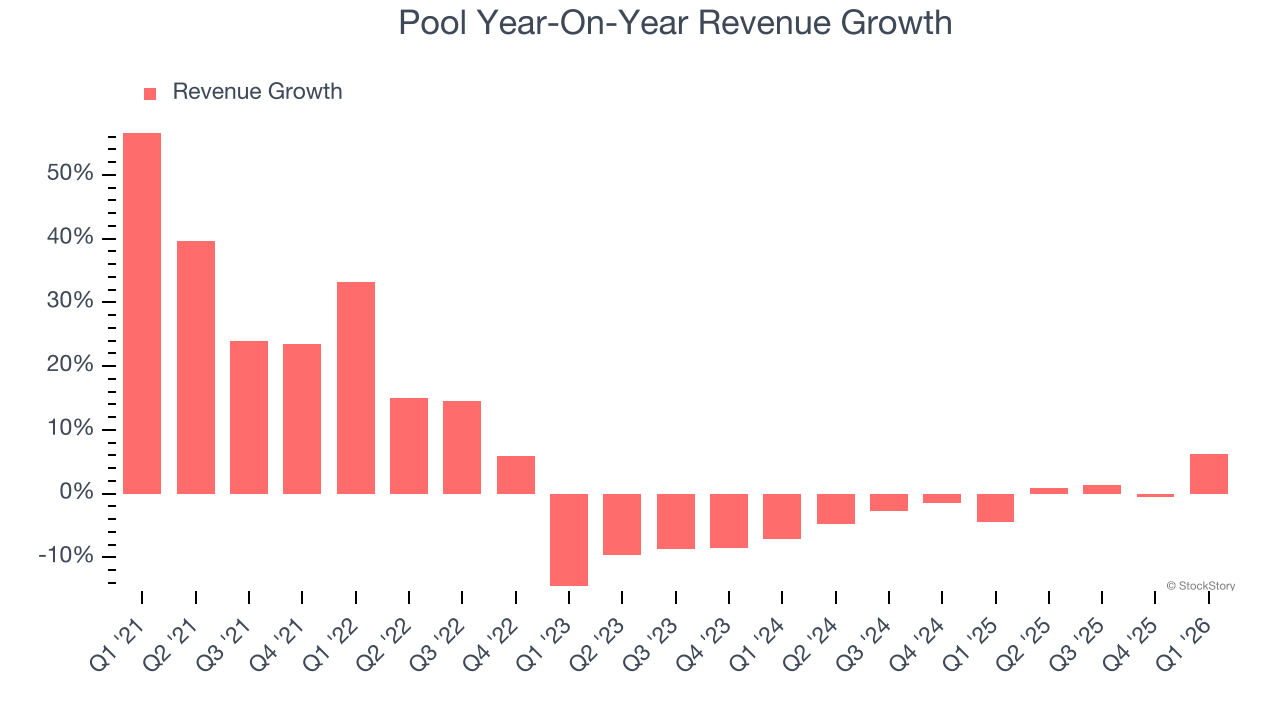

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Pool grew its sales at a weak 4.4% compounded annual growth rate. This fell short of our benchmark for the consumer discretionary sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Pool’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Pool reported year-on-year revenue growth of 6.2%, and its $1.14 billion of revenue exceeded Wall Street’s estimates by 3.8%.

Looking ahead, sell-side analysts expect revenue to grow 1.7% over the next 12 months. While this projection implies its newer products and services will fuel better top-line performance, it is still below the sector average.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Pool’s operating margin has generally stayed the same over the last 12 months, and we generally like to see margin increases due to economies of scale and cost efficiency over time.

This quarter, Pool generated an operating margin profit margin of 7.3%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

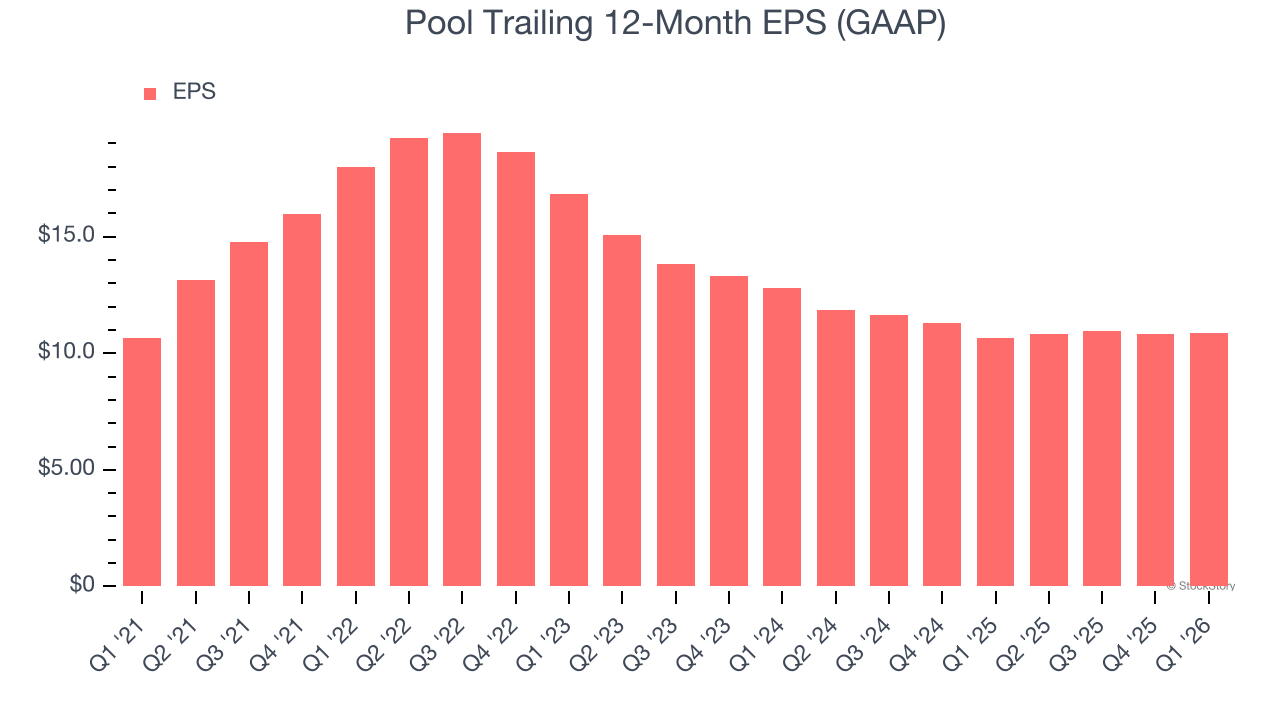

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Pool’s flat EPS over the last five years was below its 4.4% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

In Q1, Pool reported EPS of $1.45, up from $1.42 in the same quarter last year. This print beat analysts’ estimates by 6.7%. Over the next 12 months, Wall Street expects Pool’s full-year EPS of $10.87 to grow 3%.

Key Takeaways from Pool’s Q1 Results

It was encouraging to see Pool beat analysts’ adjusted operating income expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, this print had some key positives. The market seemed to be hoping for more, and the stock traded down 2.2% to $229.01 immediately after reporting.

Big picture, is Pool a buy here and now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).