Fast-food chain Wingstop (NASDAQ: WING) fell short of the market’s revenue expectations in Q1 CY2026, but sales rose 7.4% year on year to $183.7 million. Its non-GAAP profit of $1.18 per share was 15.1% above analysts’ consensus estimates.

Is now the time to buy Wingstop? Find out by accessing our full research report, it’s free.

Wingstop (WING) Q1 CY2026 Highlights:

- Revenue: $183.7 million vs analyst estimates of $188.3 million (7.4% year-on-year growth, 2.4% miss)

- Adjusted EPS: $1.18 vs analyst estimates of $1.03 (15.1% beat)

- Adjusted EBITDA: $65.4 million vs analyst estimates of $63.39 million (35.6% margin, 3.2% beat)

- Operating Margin: 27.4%, up from 22.4% in the same quarter last year

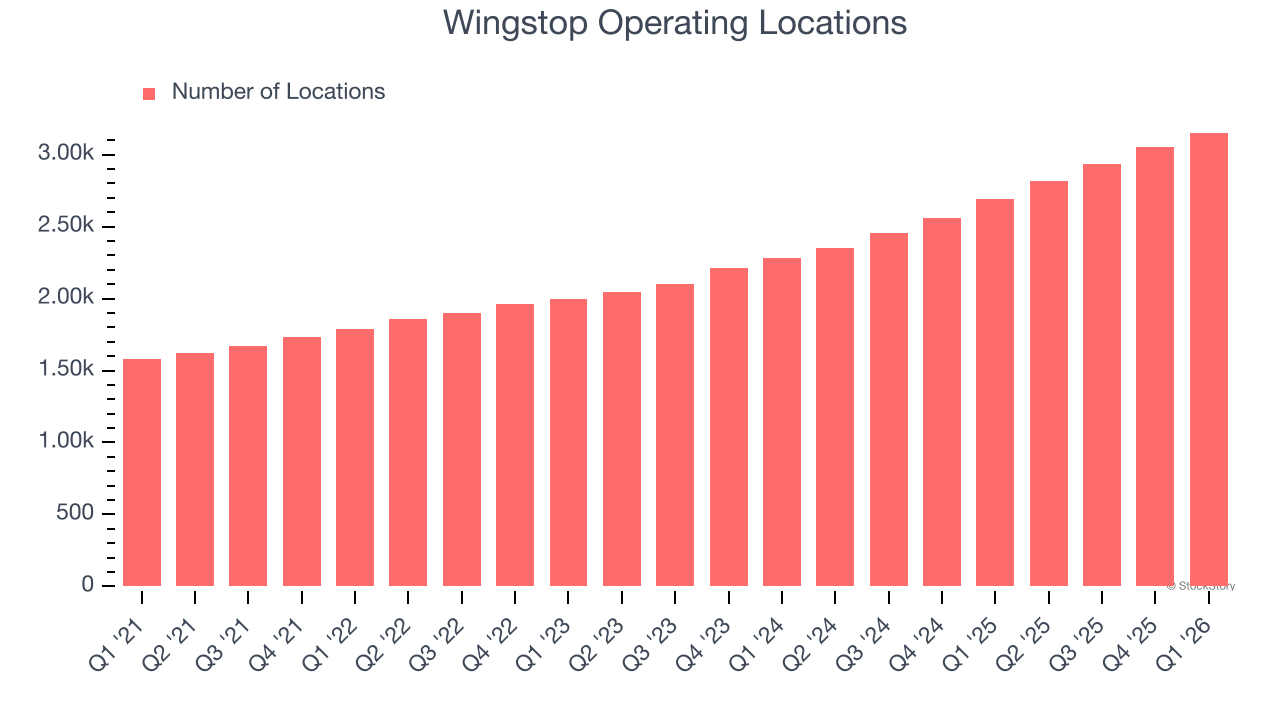

- Locations: 3,153 at quarter end, up from 2,689 in the same quarter last year

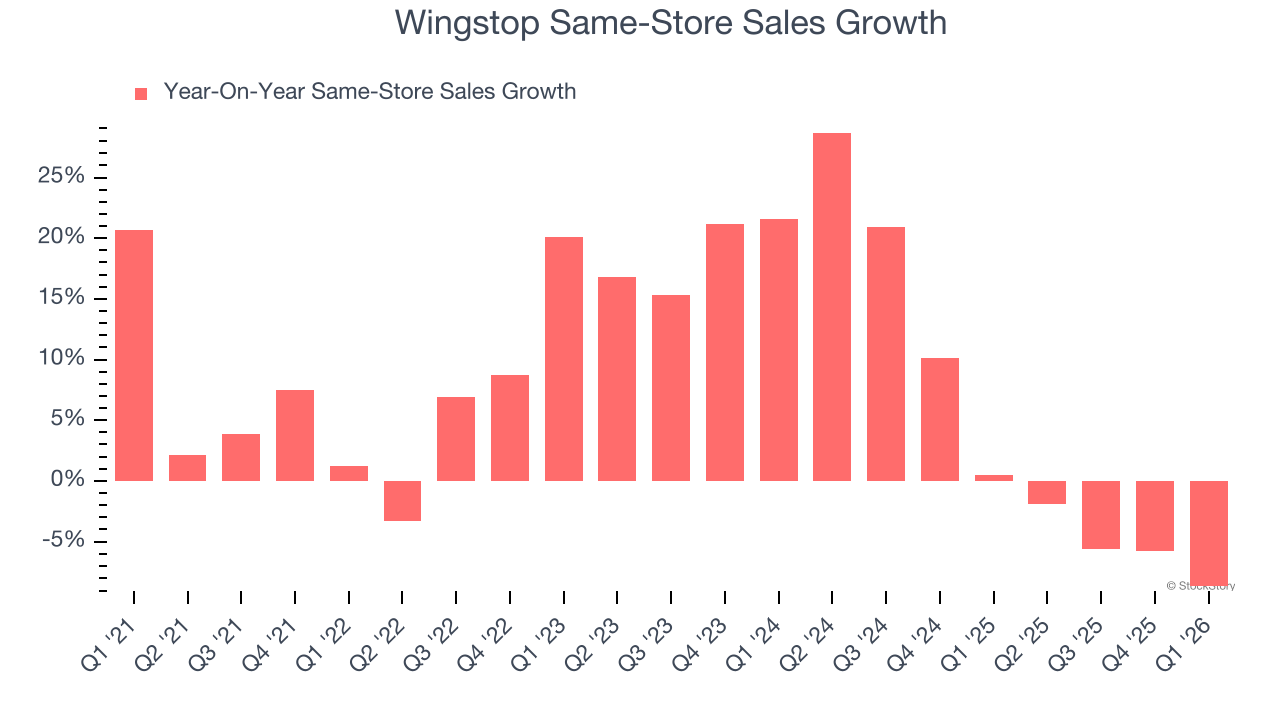

- Same-Store Sales fell 8.7% year on year (0.5% in the same quarter last year)

- Market Capitalization: $4.73 billion

"Despite the decline in same store sales, we delivered system-wide sales growth and double-digit Adjusted EBITDA growth in the quarter supported by 17% unit growth. Our results demonstrate the resiliency of our asset-light, highly franchised model," said Michael Skipworth, President and Chief Executive Officer.

Company Overview

The passion project of two chicken wing aficionados in Texas, Wingstop (NASDAQ: WING) is a popular fast-food chain known for its flavorful and crispy chicken wings offered in a variety of sauces and seasonings.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $709.5 million in revenue over the past 12 months, Wingstop is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the bright side, it can grow faster because it has more white space to build new restaurants.

As you can see below, Wingstop’s 23.3% annualized revenue growth over the last seven years was incredible as it opened new restaurants and increased sales at existing, established dining locations.

This quarter, Wingstop’s revenue grew by 7.4% year on year to $183.7 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 16.6% over the next 12 months, a deceleration versus the last seven years. Still, this projection is noteworthy and indicates the market is baking in success for its menu offerings.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Restaurant Performance

Number of Restaurants

The number of dining locations a restaurant chain operates is a critical driver of how quickly company-level sales can grow.

Wingstop sported 3,153 locations in the latest quarter. Over the last two years, it has opened new restaurants at a rapid clip by averaging 17.7% annual growth, among the fastest in the restaurant sector. This gives it a chance to scale into a mid-sized business over time. Additionally, one dynamic making expansion more seamless is the company’s franchise model, where franchisees are primarily responsible for opening new restaurants while Wingstop provides support.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where its concepts have few or no locations.

Same-Store Sales

A company's restaurant base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at restaurants open for at least a year.

Wingstop has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 4.8%. This performance along with its meaningful buildout of new restaurants suggest it’s playing some aggressive offense.

In the latest quarter, Wingstop’s same-store sales fell by 8.7% year on year. This decline was a reversal from its historical levels. A one quarter hiccup shouldn’t deter you from investing in a business, and we’ll be monitoring the company to see how things progress.

Key Takeaways from Wingstop’s Q1 Results

We were glad Wingstop's EPS outperformed Wall Street’s estimates. On the other hand, its same-store sales missed and its revenue fell short of Wall Street’s estimates, showing that demand was softer than expected. Overall, this was a weaker quarter. The stock traded down 5.5% to $163.46 immediately following the results.

Wingstop’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).