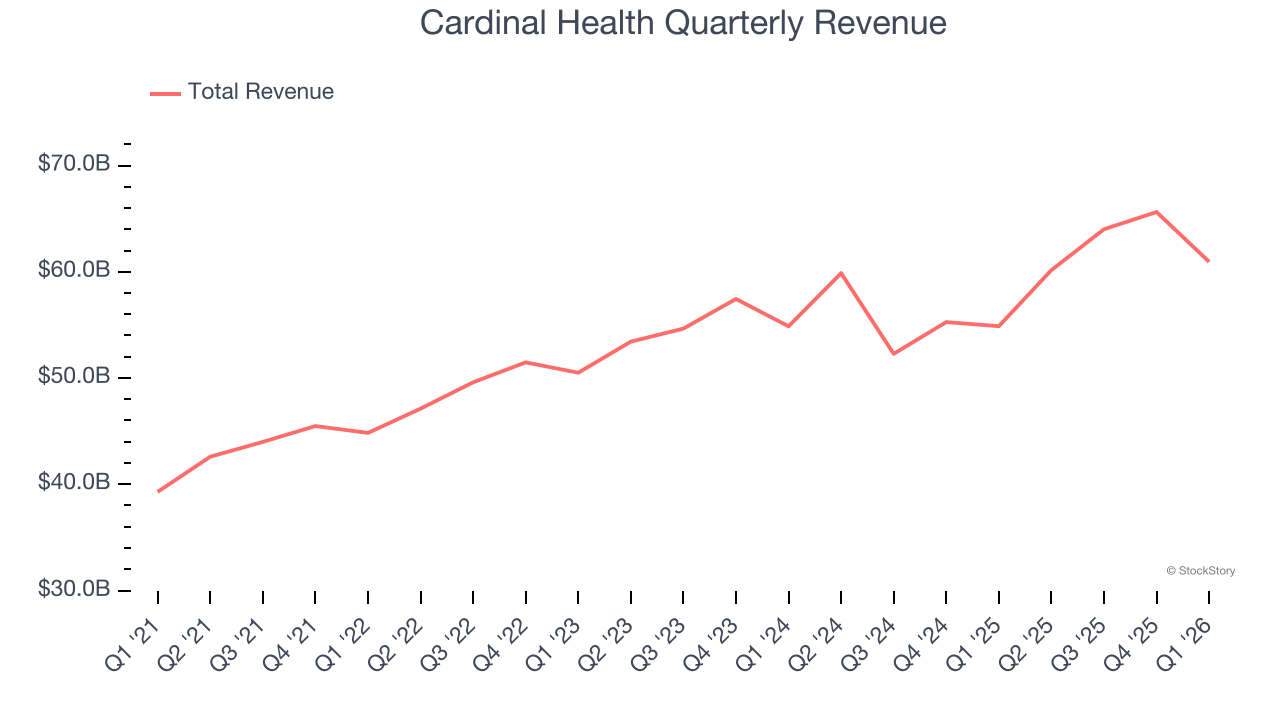

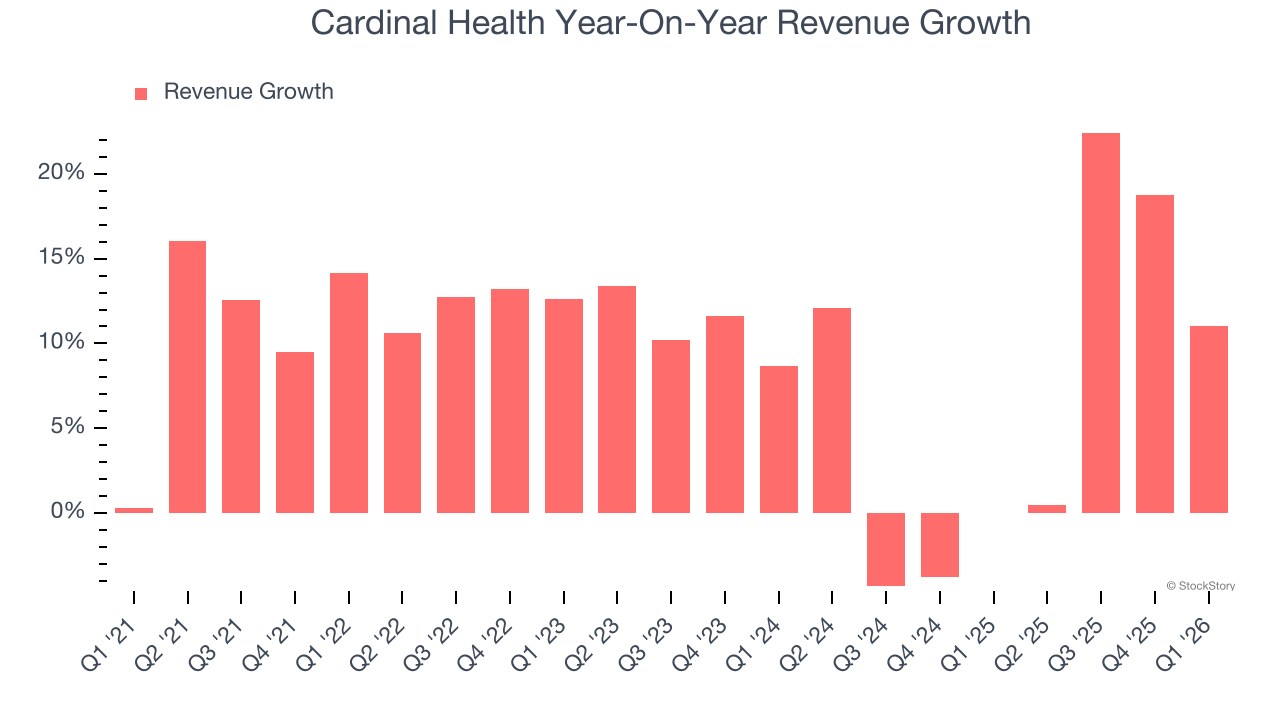

Healthcare distributor and services company Cardinal Health (NYSE: CAH) fell short of the market’s revenue expectations in Q1 CY2026, but sales rose 11% year on year to $60.94 billion. Its non-GAAP profit of $3.17 per share was 13.7% above analysts’ consensus estimates.

Is now the time to buy Cardinal Health? Find out by accessing our full research report, it’s free.

Cardinal Health (CAH) Q1 CY2026 Highlights:

- Revenue: $60.94 billion vs analyst estimates of $62.28 billion (11% year-on-year growth, 2.1% miss)

- Adjusted EPS: $3.17 vs analyst estimates of $2.79 (13.7% beat)

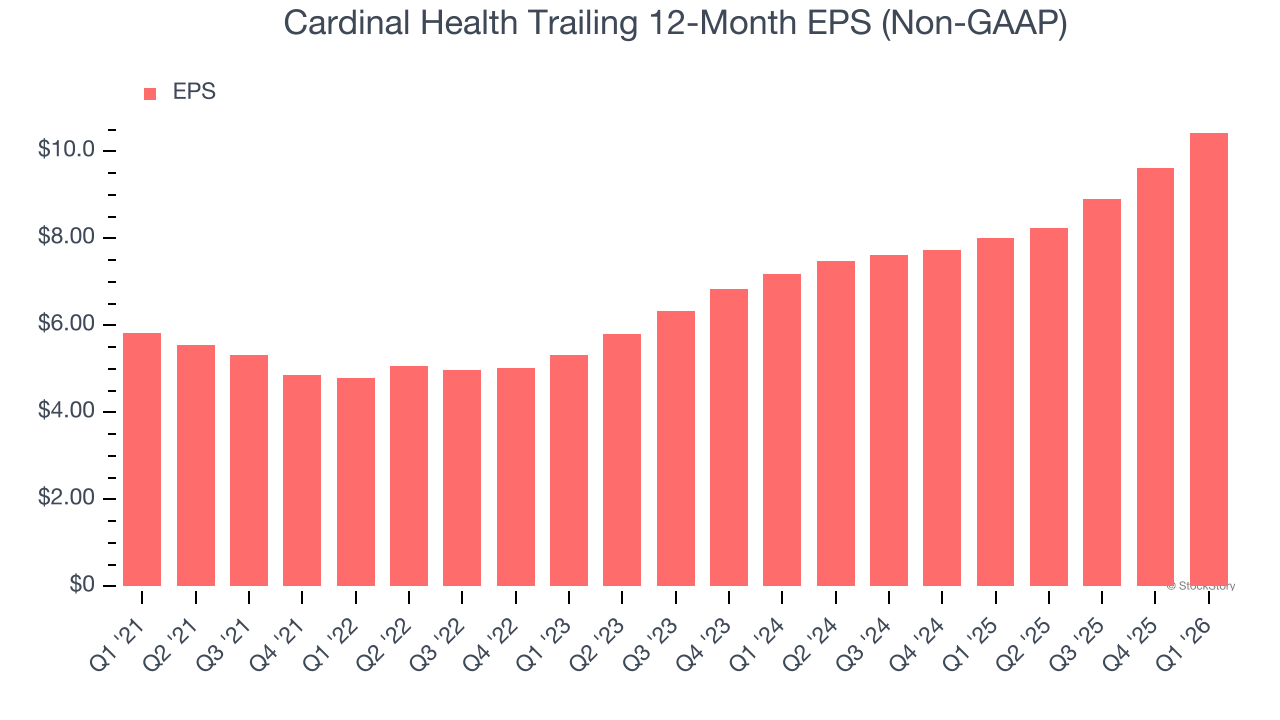

- Management raised its full-year Adjusted EPS guidance to $10.75 at the midpoint, a 4.9% increase

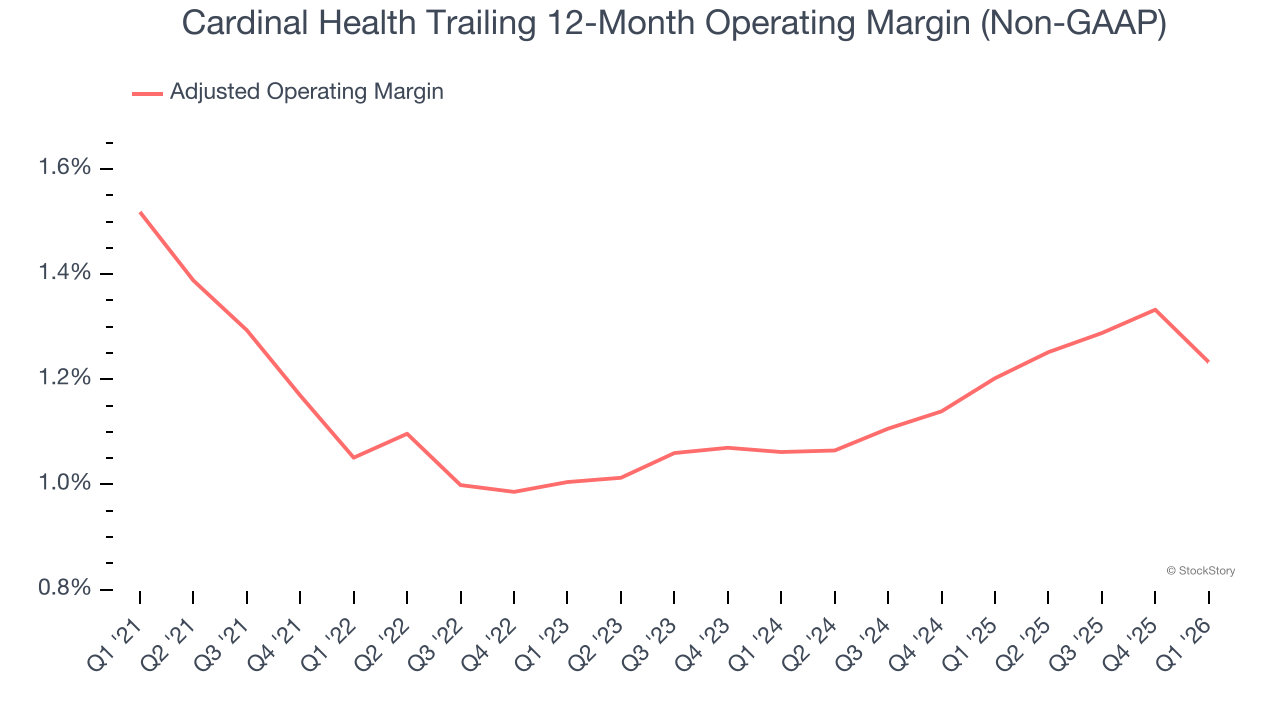

- Operating Margin: 0.8%, in line with the same quarter last year

- Free Cash Flow Margin: 2.8%, down from 5.1% in the same quarter last year

- Market Capitalization: $47.73 billion

"An excellent third quarter extends our FY26 momentum, due to the durability and resilience of our business," said Jason Hollar, CEO of Cardinal Health.

Company Overview

Operating as a critical link in the healthcare supply chain since 1979, Cardinal Health (NYSE: CAH) distributes pharmaceuticals and manufactures medical products for hospitals, pharmacies, and healthcare providers across the global healthcare supply chain.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Cardinal Health grew its sales at a decent 9.9% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Cardinal Health’s recent performance shows its demand has slowed as its annualized revenue growth of 6.7% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Cardinal Health’s revenue grew by 11% year on year to $60.94 billion but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 10.6% over the next 12 months, an improvement versus the last two years. This projection is particularly noteworthy for a company of its scale and suggests its newer products and services will spur better top-line performance.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Cardinal Health’s adjusted operating margin has generally stayed the same over the last 12 months, averaging 1.1% over the last five years. This profitability was lousy for a healthcare business and caused by its suboptimal cost structure.

Looking at the trend in its profitability, Cardinal Health’s adjusted operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q1, Cardinal Health generated an adjusted operating margin profit margin of 1%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Cardinal Health’s EPS grew at 12.4% compounded annual growth rate over the last five years, higher than its 9.9% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its adjusted operating margin didn’t improve.

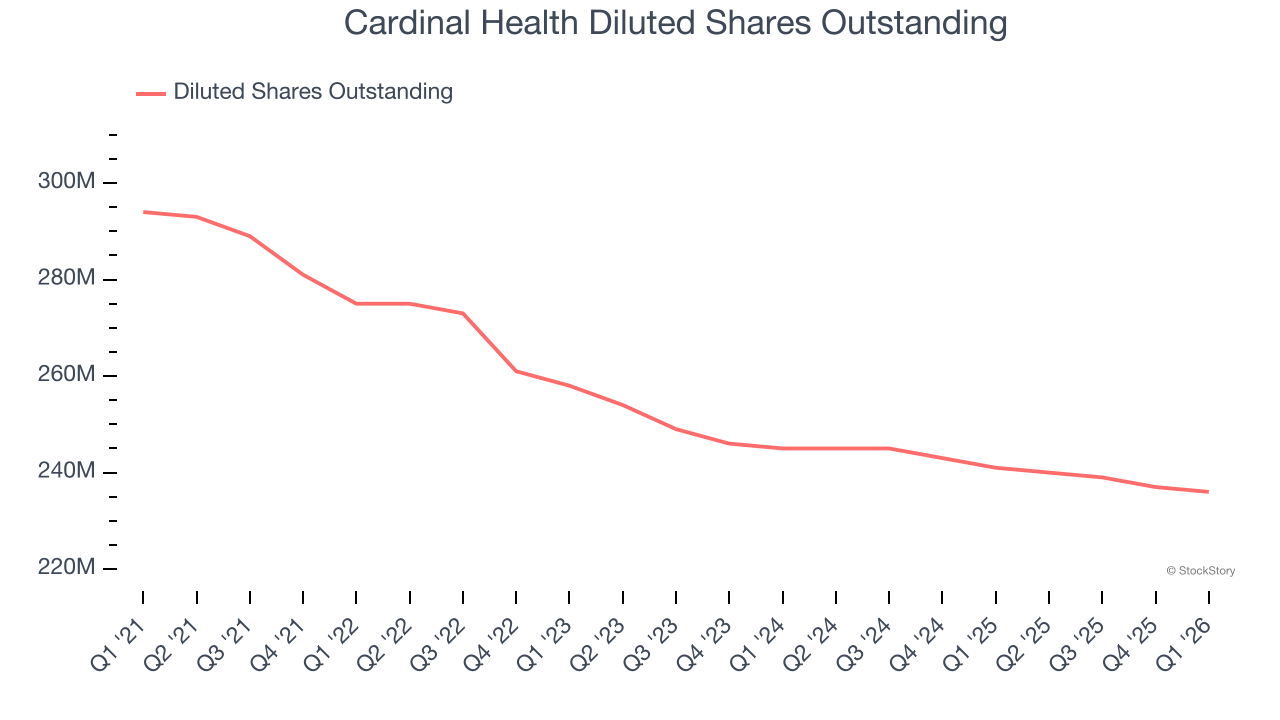

We can take a deeper look into Cardinal Health’s earnings to better understand the drivers of its performance. A five-year view shows that Cardinal Health has repurchased its stock, shrinking its share count by 19.7%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q1, Cardinal Health reported adjusted EPS of $3.17, up from $2.35 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Cardinal Health’s full-year EPS of $10.43 to grow 7.9%.

Key Takeaways from Cardinal Health’s Q1 Results

We enjoyed seeing Cardinal Health beat analysts’ full-year EPS guidance expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue missed. Overall, this print was mixed. The stock remained flat at $203.50 immediately after reporting.

Is Cardinal Health an attractive investment opportunity at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).