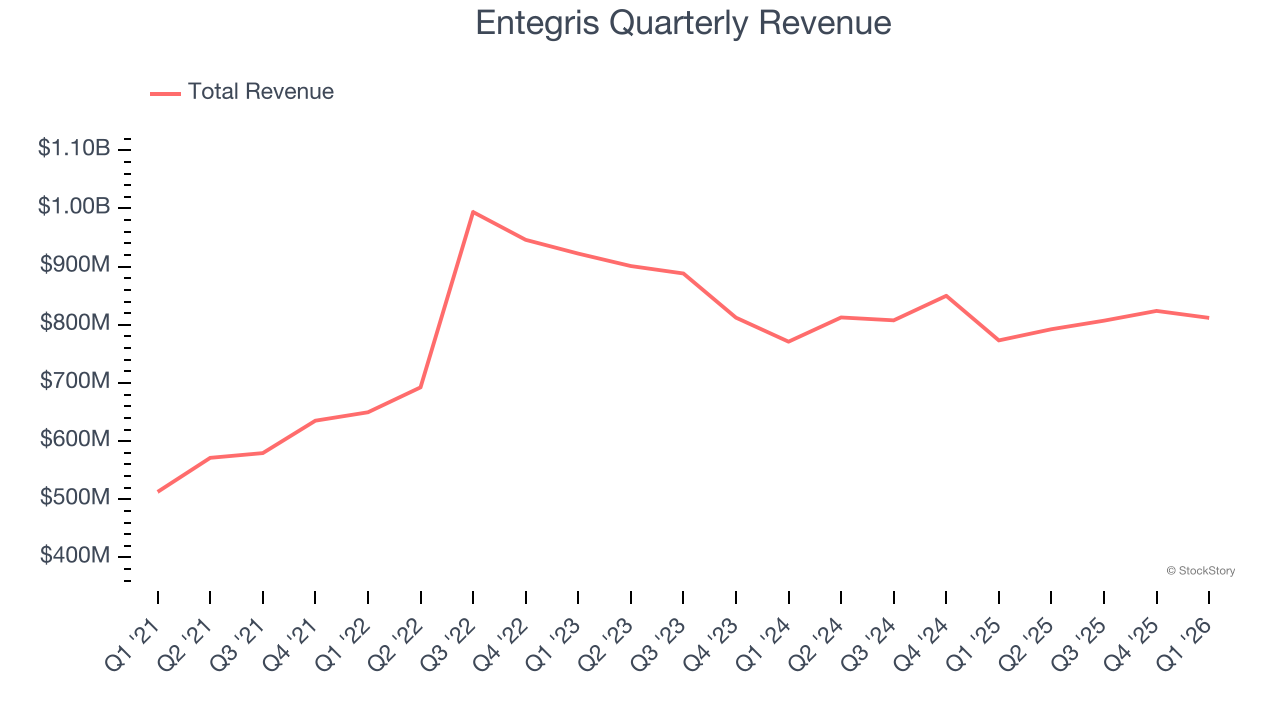

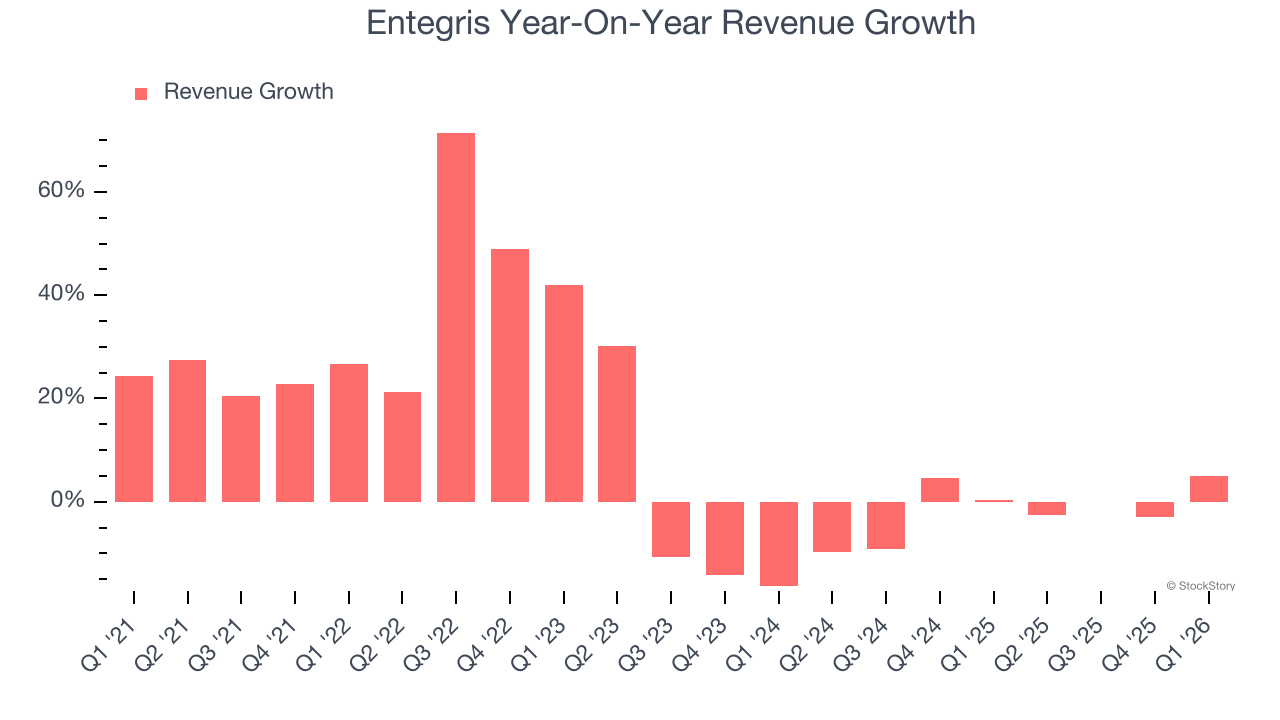

Semiconductor materials supplier Entegris (NASDAQ: ENTG) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 5% year on year to $811.9 million. The company expects next quarter’s revenue to be around $830 million, close to analysts’ estimates. Its non-GAAP profit of $0.86 per share was 15.4% above analysts’ consensus estimates.

Is now the time to buy Entegris? Find out by accessing our full research report, it’s free.

Entegris (ENTG) Q1 CY2026 Highlights:

- Revenue: $811.9 million vs analyst estimates of $807.8 million (5% year-on-year growth, 0.5% beat)

- Adjusted EPS: $0.86 vs analyst estimates of $0.75 (15.4% beat)

- Adjusted EBITDA: $226.1 million vs analyst estimates of $219.6 million (27.8% margin, 2.9% beat)

- Revenue Guidance for Q2 CY2026 is $830 million at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for Q2 CY2026 is $0.80 at the midpoint, above analyst estimates of $0.77

- Operating Margin: 17.4%, up from 15.8% in the same quarter last year

- Free Cash Flow Margin: 17.4%, up from 4.2% in the same quarter last year

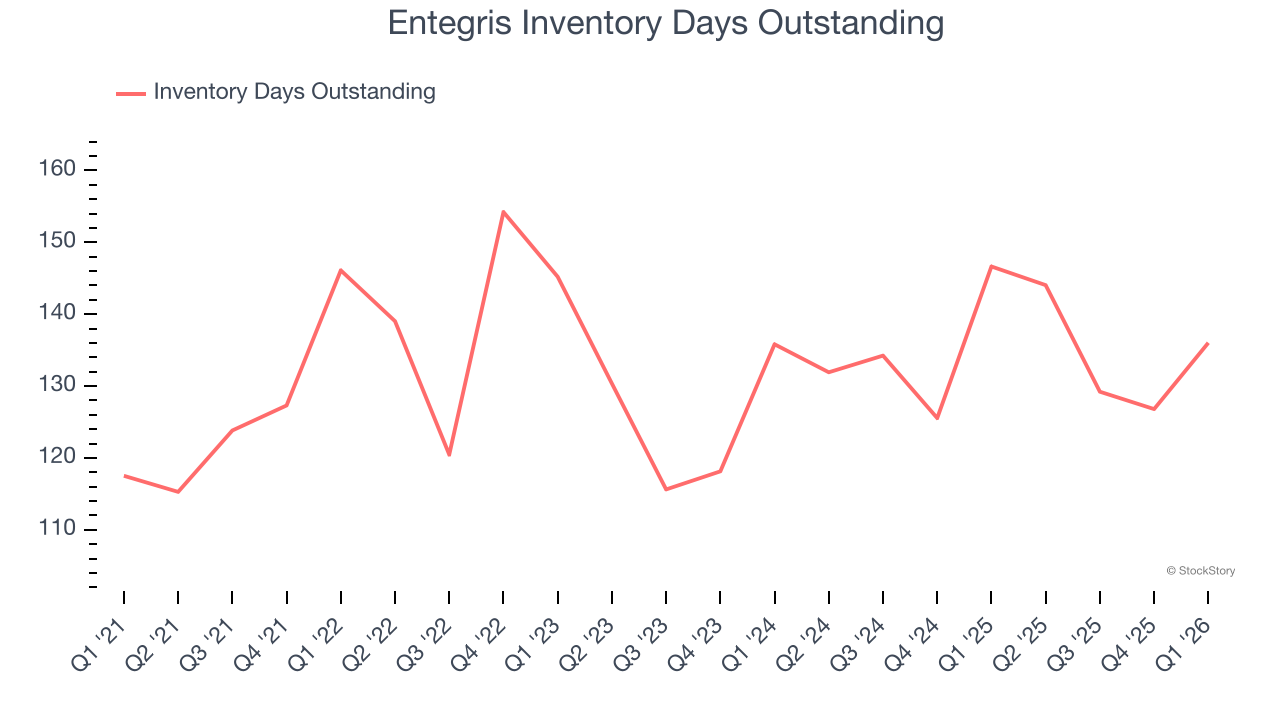

- Inventory Days Outstanding: 136, up from 127 in the previous quarter

- Market Capitalization: $22.71 billion

Dave Reeder, Entegris’ President and Chief Executive Officer, said: “Entegris delivered solid first quarter results, continuing our trend of disciplined execution and focused customer engagement. Revenue grew 5% year-over-year, primarily driven by increasing unit-driven volumes related to the industry’s most advanced manufacturing processes. Adjusted gross margin, adjusted EBITDA margin and non-GAAP EPS all exceeded our guidance range. Strong cash generation allowed us to reduce leverage while continuing to invest in our customers’ technology roadmaps.”

Company Overview

With fabs representing the company’s largest customer type, Entegris (NASDAQ: ENTG) supplies products that purify, protect, and generally ensure the integrity of raw materials needed for advanced semiconductor manufacturing.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, Entegris’s 10.5% annualized revenue growth over the last five years was solid. Its growth beat the average semiconductor company and shows its offerings resonate with customers. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Entegris’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 2.1% over the last two years.

This quarter, Entegris reported year-on-year revenue growth of 5%, and its $811.9 million of revenue exceeded Wall Street’s estimates by 0.5%. Adding to the positive news, Entegris’s growth inflected positively this quarter, news that will likely give some shareholders hope. Company management is currently guiding for a 4.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.9% over the next 12 months. While this projection implies its newer products and services will fuel better top-line performance, it is still below average for the sector.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Entegris’s DIO came in at 136, which is 4 days above its five-year average, suggesting that the company’s inventory has grown to higher levels than we’ve seen in the past.

Key Takeaways from Entegris’s Q1 Results

It was good to see Entegris beat analysts’ EPS expectations this quarter. We were also glad its adjusted operating income outperformed Wall Street’s estimates. On the other hand, its inventory levels materially increased. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 3.5% to $154.67 immediately after reporting.

Indeed, Entegris had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).