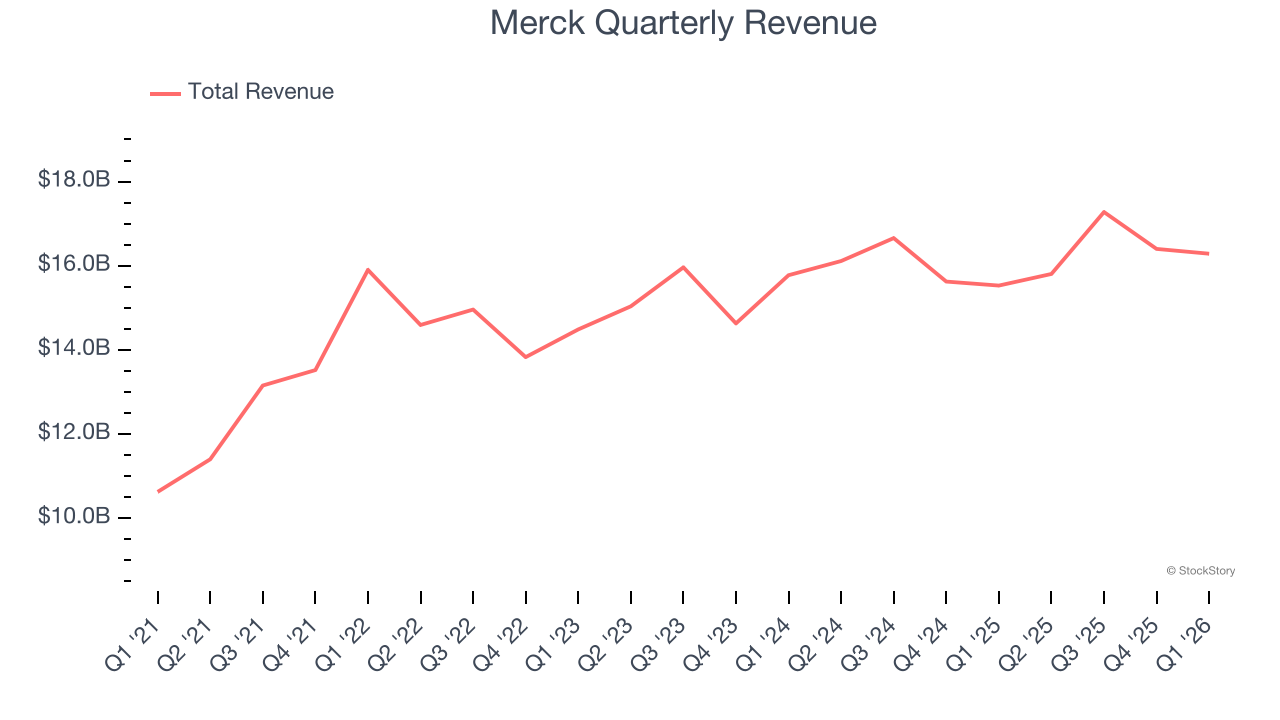

Global pharmaceutical company Merck (NYSE: MRK) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 4.9% year on year to $16.29 billion. The company expects the full year’s revenue to be around $66.4 billion, close to analysts’ estimates. Its non-GAAP loss of $1.28 per share was 13.2% above analysts’ consensus estimates.

Is now the time to buy Merck? Find out by accessing our full research report, it’s free.

Merck (MRK) Q1 CY2026 Highlights:

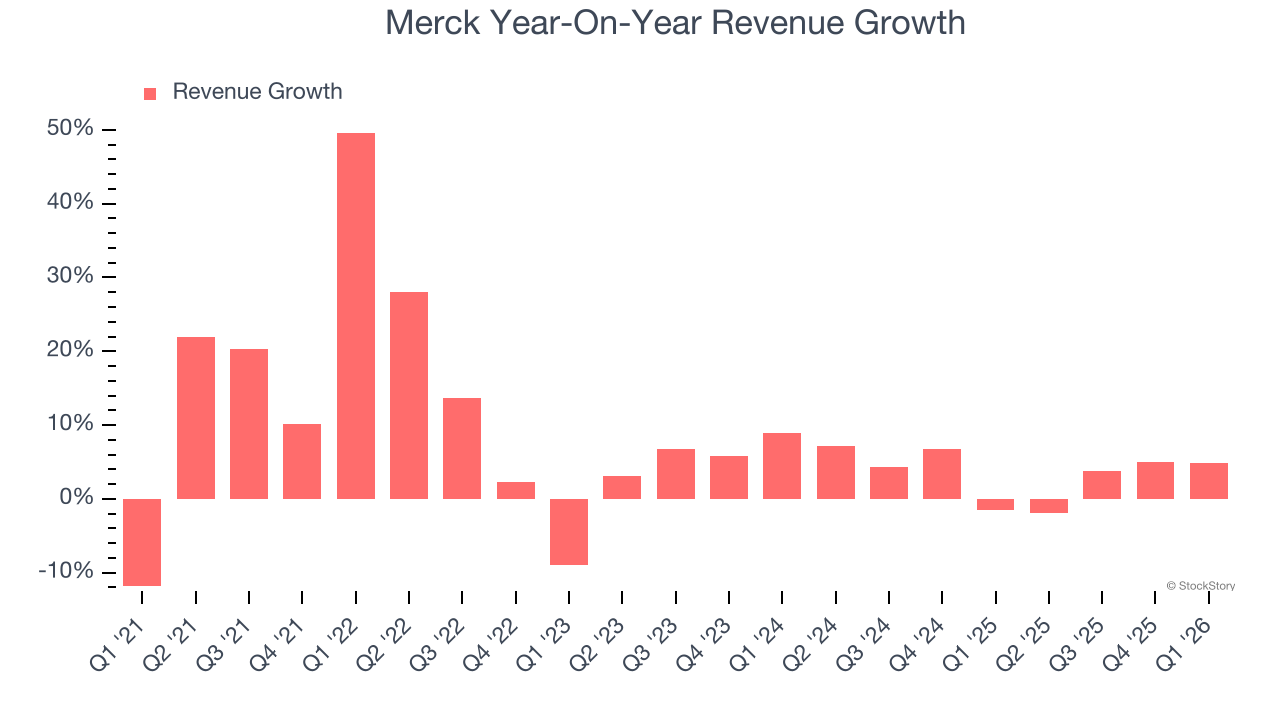

- Revenue: $16.29 billion vs analyst estimates of $15.82 billion (4.9% year-on-year growth, 3% beat)

- Adjusted EPS: -$1.28 vs analyst estimates of -$1.47 (13.2% beat)

- The company slightly lifted its revenue guidance for the full year to $66.4 billion at the midpoint from $66.25 billion

- Management slightly raised its full-year Adjusted EPS guidance to $5.10 at the midpoint

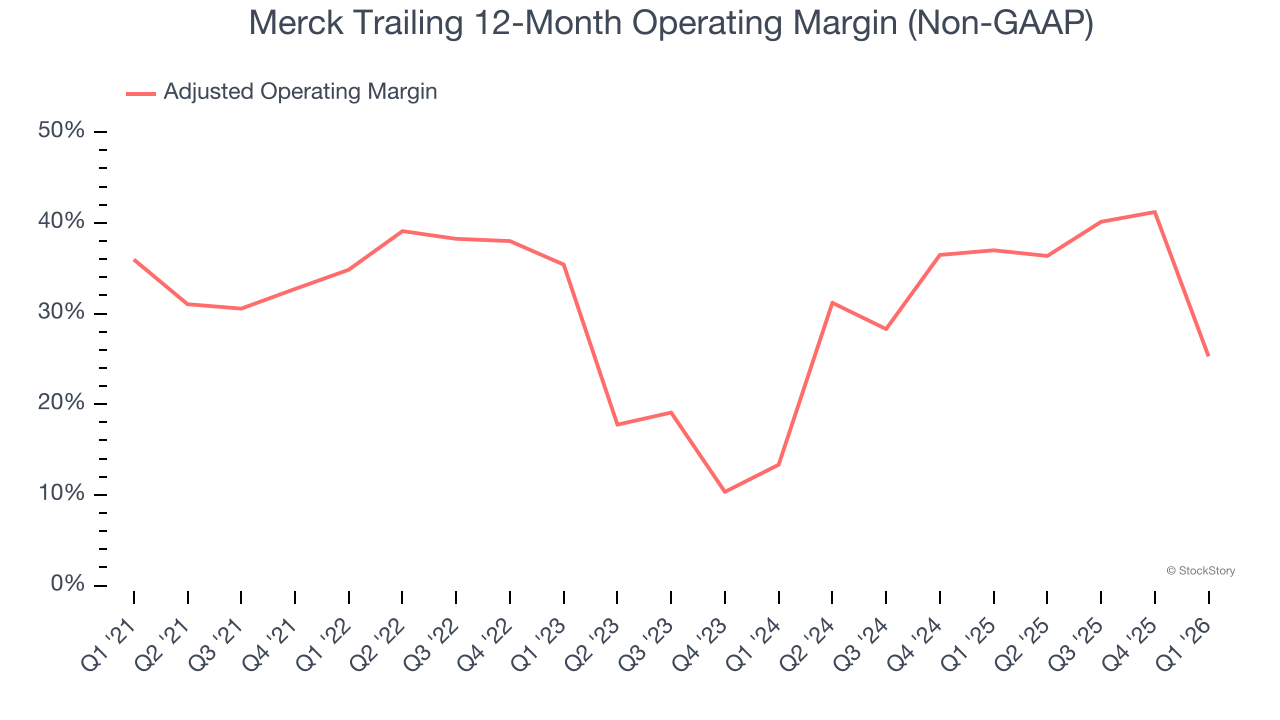

- Operating Margin: -21.7%, down from 37.8% in the same quarter last year

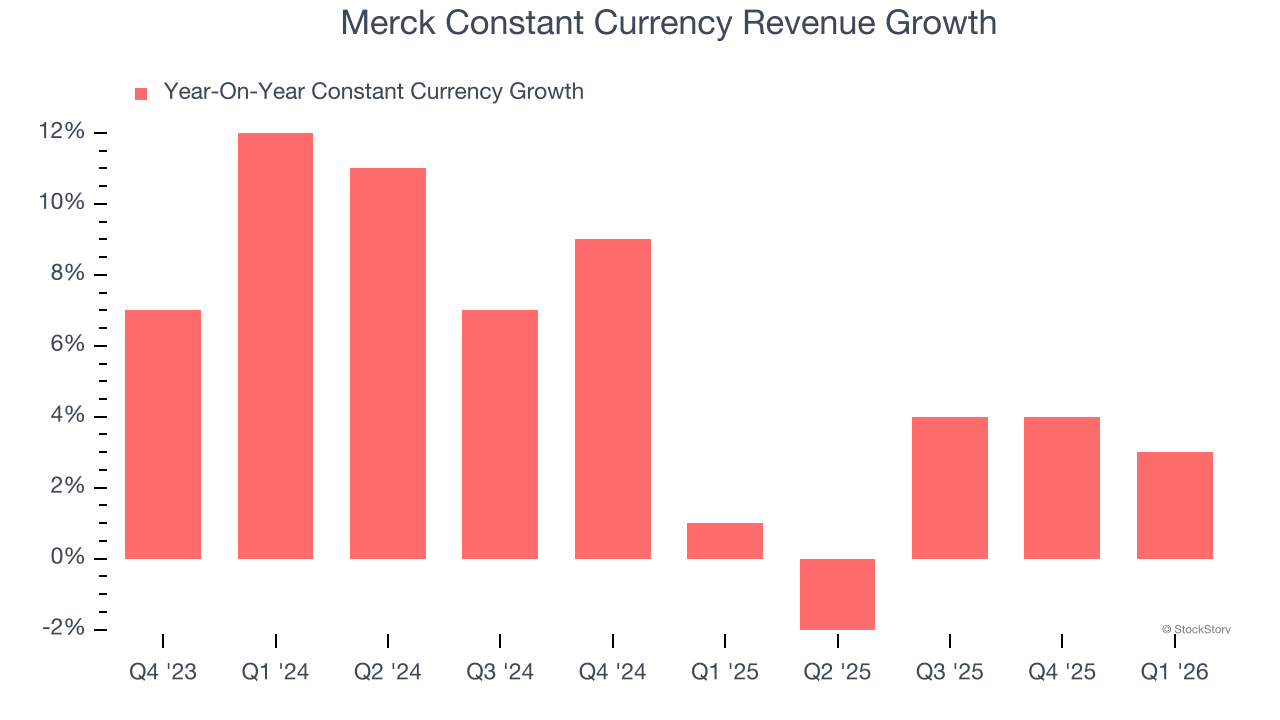

- Constant Currency Revenue rose 3% year on year (1% in the same quarter last year)

- Market Capitalization: $274 billion

“We are moving with speed to transform our portfolio to one with a diversified set of growth drivers across a broad set of therapeutic areas,” said Robert M. Davis, chairman and chief executive officer.

Company Overview

With roots dating back to 1891 and a portfolio that includes the blockbuster cancer immunotherapy Keytruda, Merck (NYSE: MRK) develops and sells prescription medicines, vaccines, and animal health products across oncology, infectious diseases, cardiovascular, and other therapeutic areas.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Merck’s sales grew at a decent 8.8% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Merck’s recent performance shows its demand has slowed as its annualized revenue growth of 3.5% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

Merck also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 4.6% year-on-year growth. Because this number aligns with its reported revenue growth, we can see that foreign exchange has not had a meaningful impact on topline.

This quarter, Merck reported modest year-on-year revenue growth of 4.9% but beat Wall Street’s estimates by 3%.

Looking ahead, sell-side analysts expect revenue to grow 1.8% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

Merck has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average adjusted operating margin of 29%.

Analyzing the trend in its profitability, Merck’s adjusted operating margin decreased by 9.6 percentage points over the last five years, but it rose by 11.9 percentage points on a two-year basis. We like Merck and hope it can right the ship.

This quarter, Merck generated an adjusted operating margin profit margin of negative 21.7%, down 64.3 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

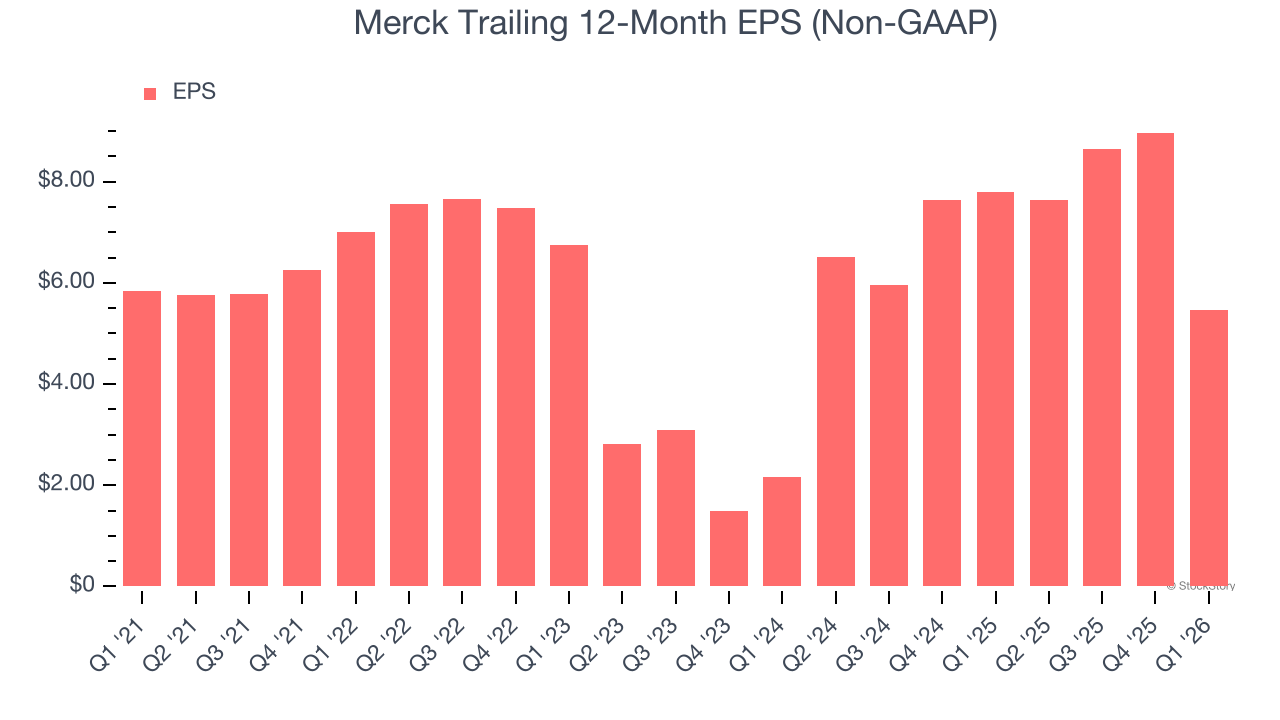

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Merck, its EPS declined by 1.3% annually over the last five years while its revenue grew by 8.8%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

We can take a deeper look into Merck’s earnings to better understand the drivers of its performance. As we mentioned earlier, Merck’s adjusted operating margin declined by 9.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Merck reported adjusted EPS of negative $1.28, down from $2.22 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Merck’s full-year EPS of $5.47 to grow 58.2%.

Key Takeaways from Merck’s Q1 Results

This was a beat and raise quarter. We enjoyed seeing Merck beat analysts’ revenue and EPS expectations this quarter. We were also glad that the company raised full-year guidance for revenue and EPS as well. Overall, this print had some key positives. The stock traded up 4.6% to $116.15 immediately after reporting.

Indeed, Merck had a rock-solid quarterly earnings result, but is this stock a good investment here? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).