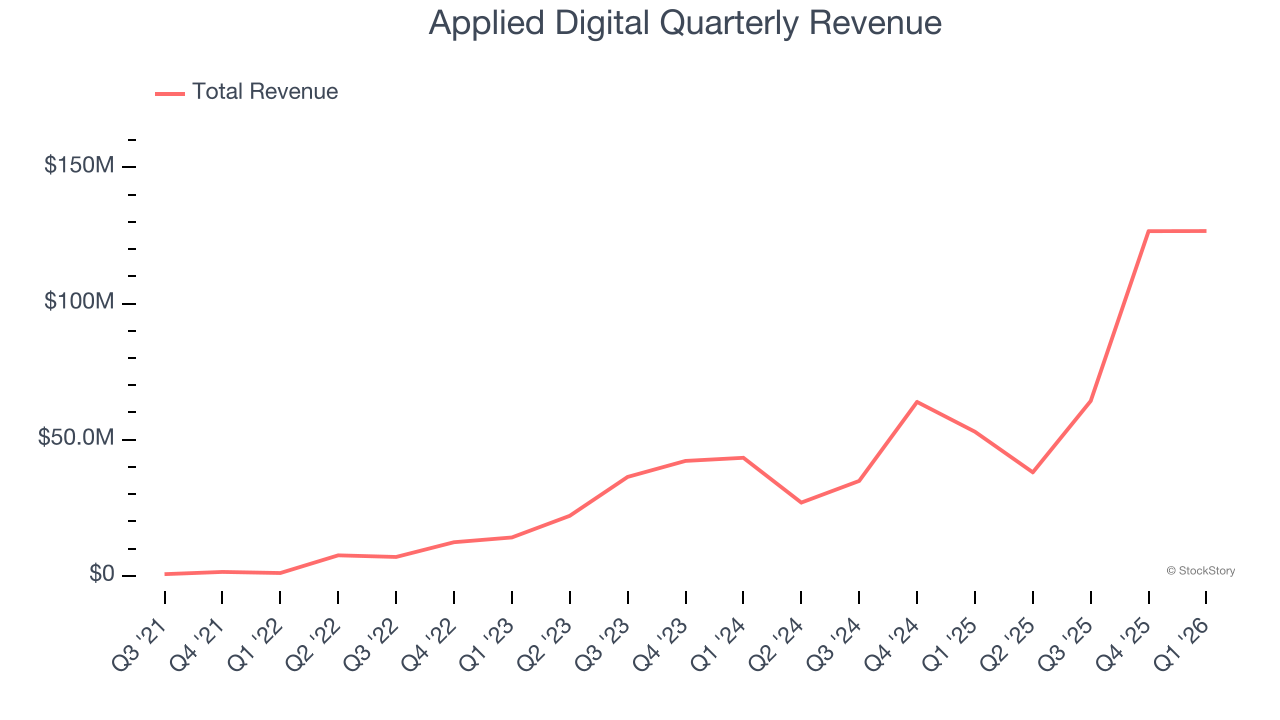

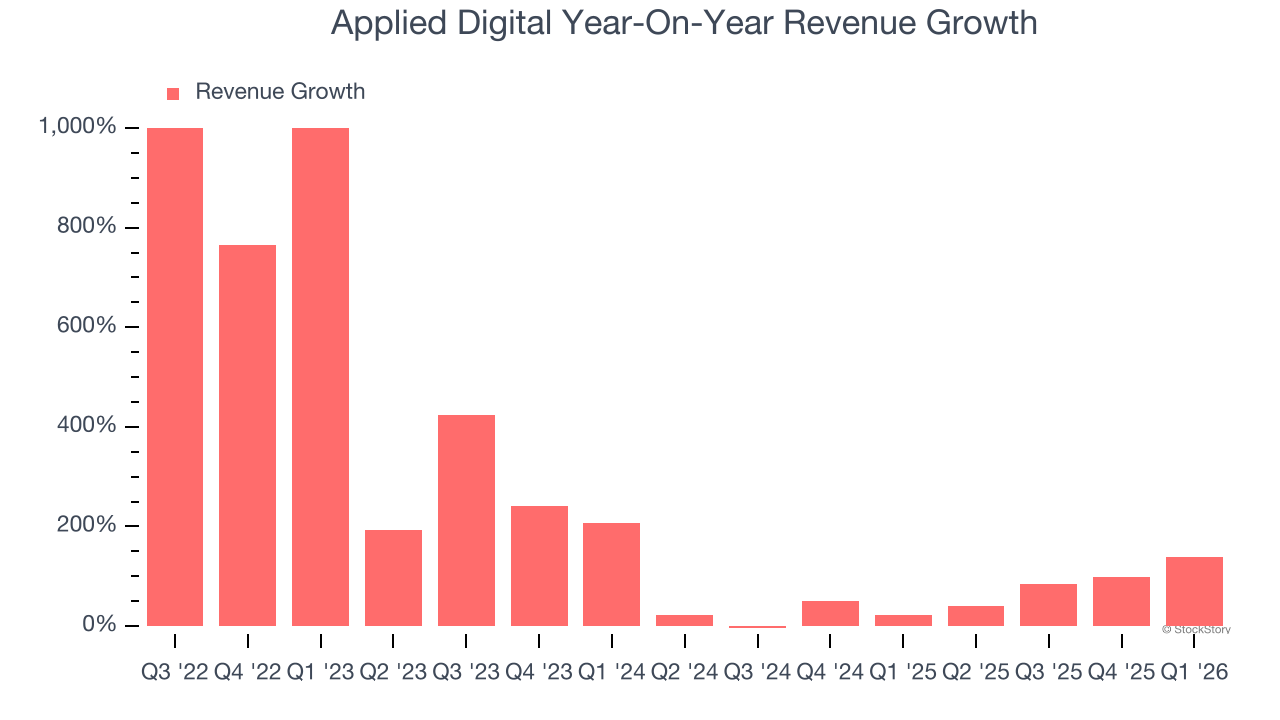

Digital infrastructure provider Applied Digital (NASDAQ: APLD) announced better-than-expected revenue in Q1 CY2026, with sales up 139% year on year to $126.6 million. Its non-GAAP profit of $0.09 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Applied Digital? Find out by accessing our full research report, it’s free.

Applied Digital (APLD) Q1 CY2026 Highlights:

- Revenue: $126.6 million vs analyst estimates of $75.69 million (139% year-on-year growth, 67.3% beat)

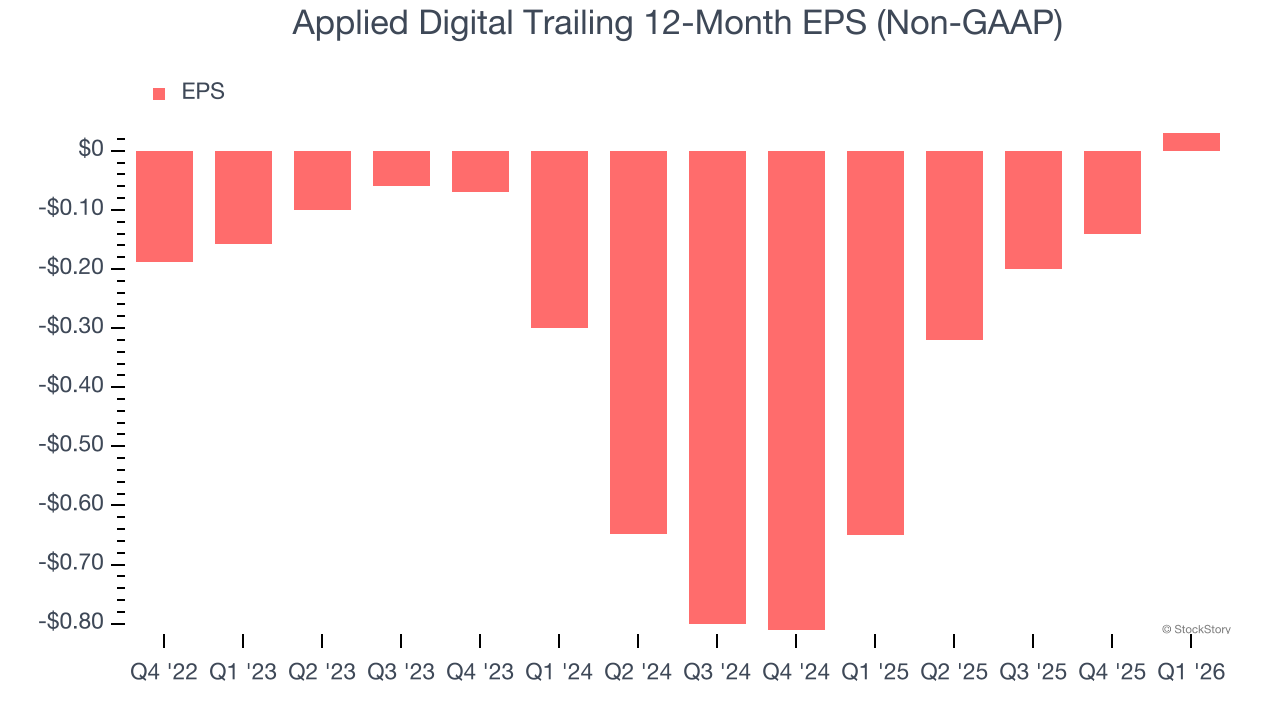

- Adjusted EPS: $0.09 vs analyst estimates of -$0.21 (significant beat)

- Adjusted EBITDA: $44.14 million vs analyst estimates of $16.19 million (34.9% margin, significant beat)

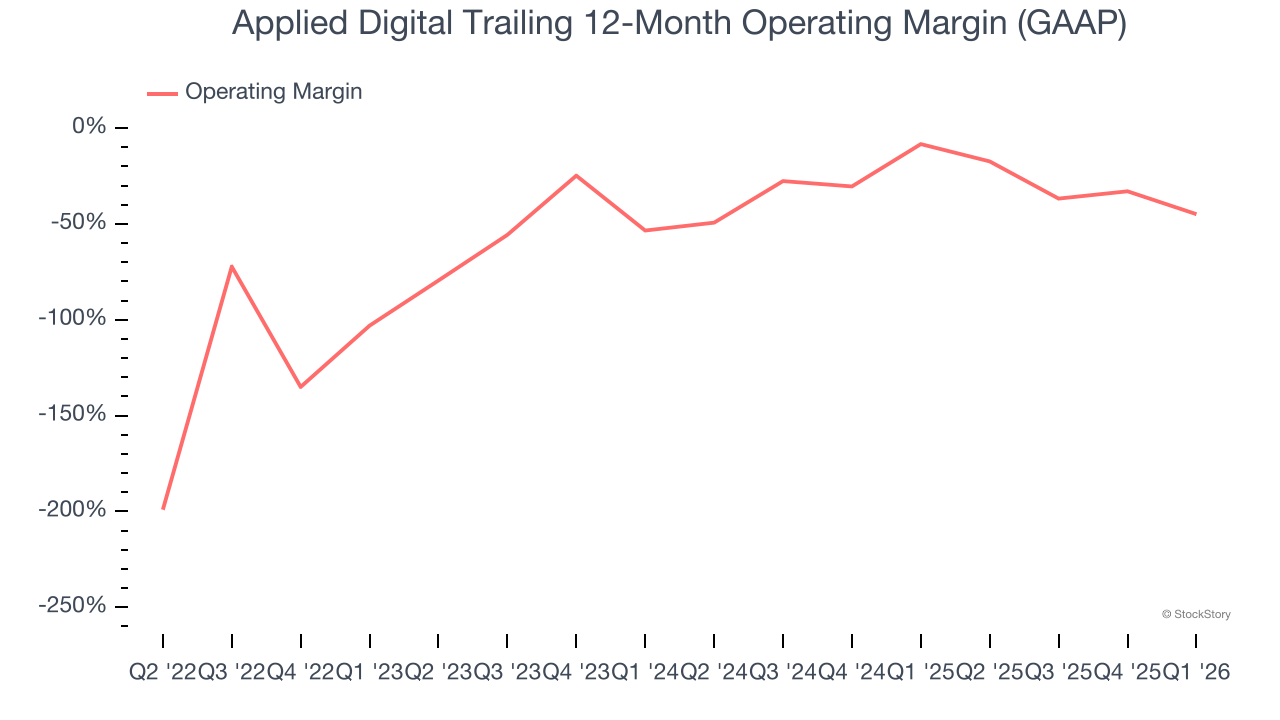

- Operating Margin: -67.6%, down from -35.8% in the same quarter last year

- Free Cash Flow was -$720.2 million compared to -$251.6 million in the same quarter last year

- Market Capitalization: $7.04 billion

“We now operate one of the only 100 MW direct-to-chip liquid-cooled data centers online today, and more importantly, it is fully operational. We believe that's what matters to our customers – turning power into live AI capacity, delivered on time and performing as expected. We are also starting to see the earnings power of our platform come through, with a full quarter of revenue from our first building now recognized. That initial 100 MW represents approximately one-sixth of our contracted capacity and one-tenth of what is operating or under construction, but we believe it begins to show what's possible from here as we continue to bring additional capacity online in the coming quarters,” said Wes Cummins, Chairman and Chief Executive Officer.

Company Overview

Pivoting from its origins in cryptocurrency mining to become a key player in the AI infrastructure boom, Applied Digital (NASDAQ: APLD) designs and operates specialized data centers that provide high-performance computing infrastructure for artificial intelligence and blockchain applications.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $355.5 million in revenue over the past 12 months, Applied Digital is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, Applied Digital grew its sales at an incredible 219% compounded annual growth rate over the last four years. This shows it had high demand, a useful starting point for our analysis.

Long-term growth is the most important, but within business services, a stretched historical view may miss new innovations or demand cycles. Applied Digital’s annualized revenue growth of 57.2% over the last two years is below its four-year trend, but we still think the results suggest healthy demand.

This quarter, Applied Digital reported magnificent year-on-year revenue growth of 139%, and its $126.6 million of revenue beat Wall Street’s estimates by 67.3%.

Looking ahead, sell-side analysts expect revenue to grow 36.8% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is healthy and implies the market is baking in success for its products and services.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Applied Digital’s high expenses have contributed to an average operating margin of negative 43% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, Applied Digital’s operating margin rose over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

Applied Digital’s operating margin was negative 67.6% this quarter.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Applied Digital’s full-year EPS flipped from negative to positive over the last three years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Applied Digital, its two-year annual EPS growth of 44.9% was higher than its three-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, Applied Digital reported adjusted EPS of $0.09, up from negative $0.08 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Applied Digital to perform poorly. Analysts forecast its full-year EPS of $0.03 will invert to negative negative $0.85.

Key Takeaways from Applied Digital’s Q1 Results

It was good to see Applied Digital beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 2.7% to $28.40 immediately following the results.

Applied Digital put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).