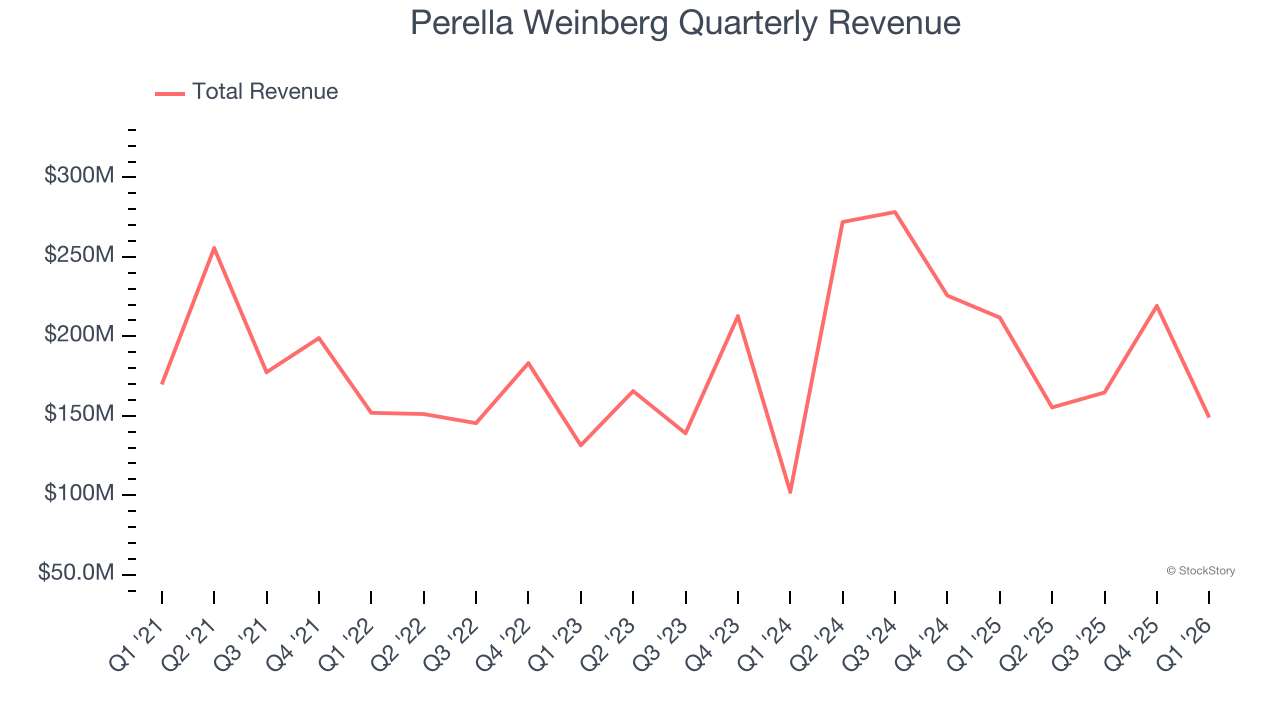

Financial advisory firm Perella Weinberg Partners (NASDAQ: PWP) missed Wall Street’s revenue expectations in Q1 CY2026, with sales falling 29.7% year on year to $148.9 million. Its non-GAAP profit of $0.05 per share was 69.7% below analysts’ consensus estimates.

Is now the time to buy Perella Weinberg? Find out by accessing our full research report, it’s free.

Perella Weinberg (PWP) Q1 CY2026 Highlights:

- Revenue: $148.9 million vs analyst estimates of $166.3 million (29.7% year-on-year decline, 10.5% miss)

- Pre-tax Profit: -$10.64 million (-7.1% margin)

- Adjusted EPS: $0.05 vs analyst expectations of $0.17 (69.7% miss)

- Market Capitalization: $1.60 billion

“We continue to see momentum across our business – client dialogue remains exceptionally strong and our announced and pending backlog is at a two-year quarterly high. Our acquisition of Gleacher Shacklock adds meaningful presence in the UK – Europe's largest advisory market – and alongside our senior talent additions and the integration of Devon Park, we are more scaled and diversified geographically and by industry and product than at any point in our history. We remain focused on our clear and simple strategy to scale our business,” stated Andrew Bednar, Chief Executive Officer.

Company Overview

Founded in 2006 by veteran investment bankers Joseph Perella and Peter Weinberg during a wave of boutique advisory firm launches, Perella Weinberg Partners (NASDAQ: PWP) is a global independent advisory firm that provides strategic and financial advice to corporations, financial sponsors, and government institutions.

Revenue Growth

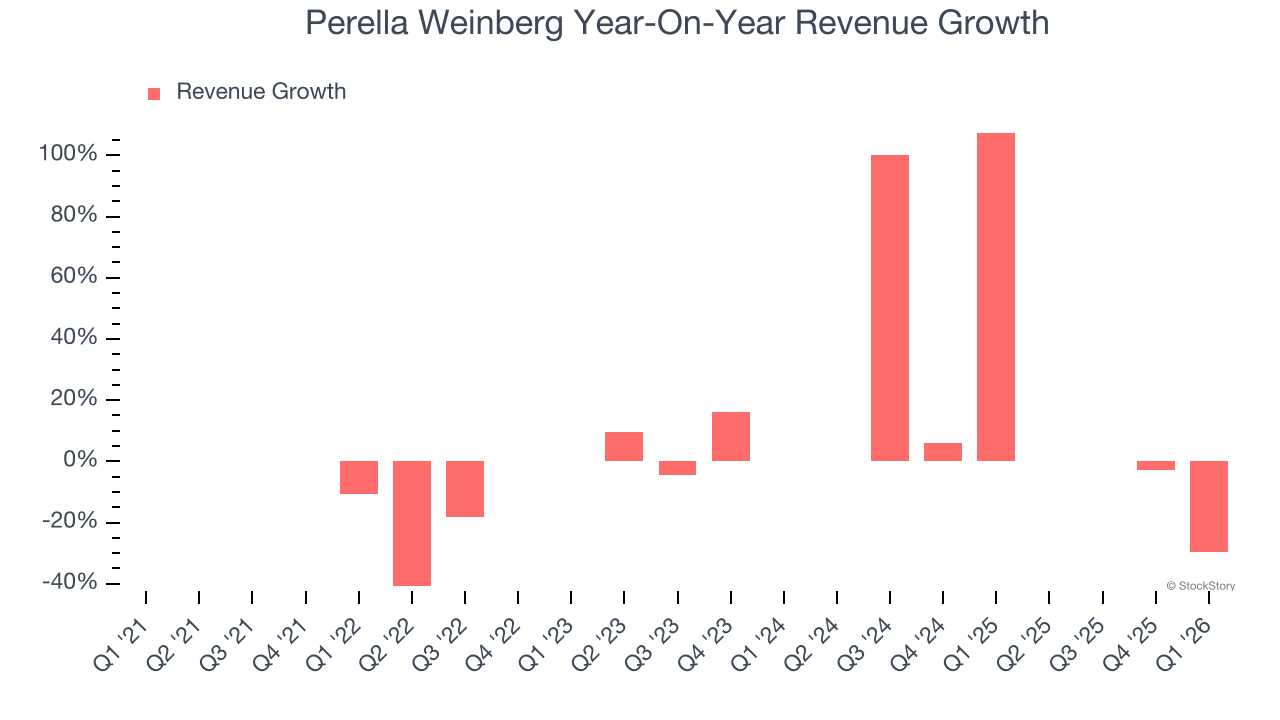

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Perella Weinberg grew its revenue at a sluggish 2.9% compounded annual growth rate. This fell short of our benchmarks and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Perella Weinberg’s annualized revenue growth of 5.4% over the last two years is above its five-year trend, which is encouraging.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Perella Weinberg missed Wall Street’s estimates and reported a rather uninspiring 29.7% year-on-year revenue decline, generating $148.9 million of revenue.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Key Takeaways from Perella Weinberg’s Q1 Results

We struggled to find many positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. Still, the stock traded up 1% to $22.65 immediately following the results.

Is Perella Weinberg an attractive investment opportunity right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).