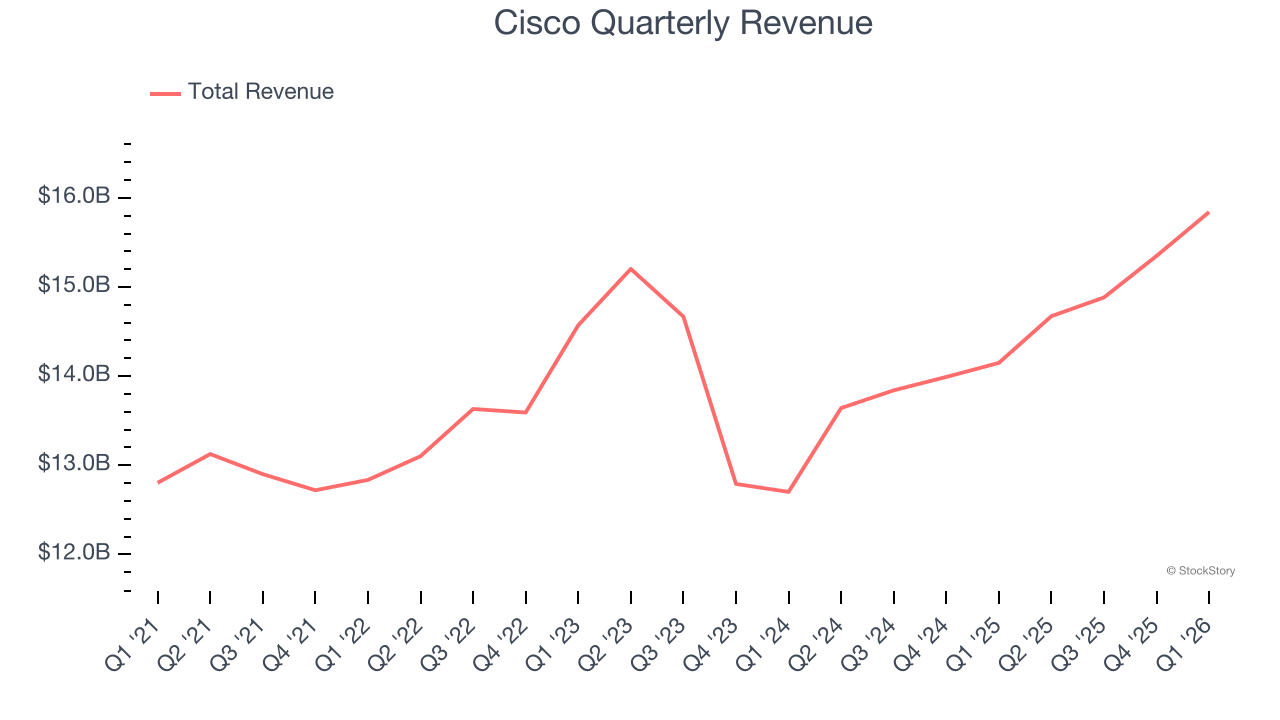

Networking technology giant Cisco (NASDAQ: CSCO) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 12% year on year to $15.84 billion. On top of that, next quarter’s revenue guidance ($16.8 billion at the midpoint) was surprisingly good and 6.5% above what analysts were expecting. Its non-GAAP profit of $1.06 per share was 2.3% above analysts’ consensus estimates.

Is now the time to buy Cisco? Find out by accessing our full research report, it’s free.

Cisco (CSCO) Q1 CY2026 Highlights:

- Revenue: $15.84 billion vs analyst estimates of $15.55 billion (12% year-on-year growth, 1.9% beat)

- Adjusted EPS: $1.06 vs analyst estimates of $1.04 (2.3% beat)

- Adjusted EBITDA: $5.51 billion vs analyst estimates of $5.93 billion (34.8% margin, 7.1% miss)

- Revenue Guidance for Q2 CY2026 is $16.8 billion at the midpoint, above analyst estimates of $15.78 billion

- Management raised its full-year Adjusted EPS guidance to $4.28 at the midpoint, a 3.1% increase

- Operating Margin: 25%, up from 22.6% in the same quarter last year

- Free Cash Flow Margin: 21.1%, down from 26.8% in the same quarter last year

- Market Capitalization: $392.2 billion

Company Overview

Founded in 1984 by a husband and wife team who wanted computers at Stanford to talk to computers at UC Berkeley, Cisco (NASDAQ: CSCO) designs and sells networking equipment, security solutions, and collaboration tools that help businesses connect their systems and secure their digital operations.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $60.75 billion in revenue over the past 12 months, Cisco is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because it’s challenging to maintain high growth rates when you’ve already captured a large portion of the addressable market. For Cisco to boost its sales, it likely needs to adjust its prices, launch new offerings, or lean into foreign markets.

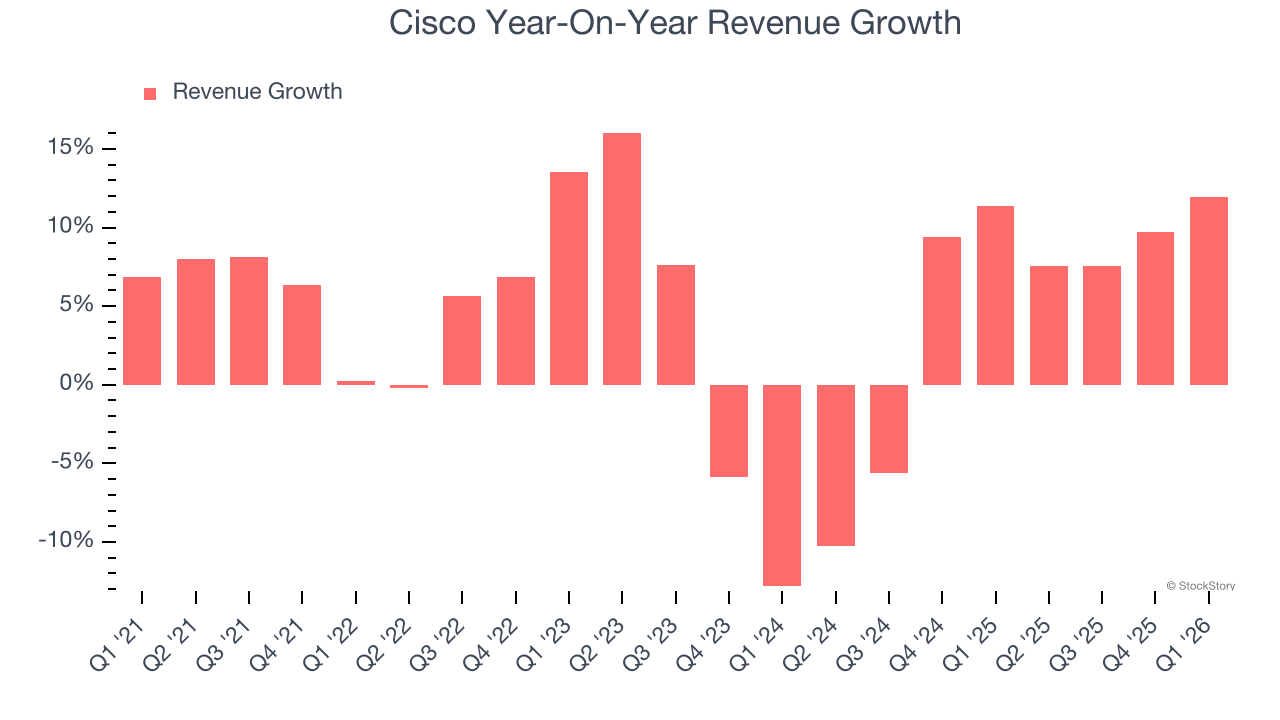

As you can see below, Cisco grew its sales at a mediocre 4.5% compounded annual growth rate over the last five years. This shows it couldn’t generate demand in any major way and is a tough starting point for our analysis.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Cisco’s annualized revenue growth of 4.7% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Cisco reported year-on-year revenue growth of 12%, and its $15.84 billion of revenue exceeded Wall Street’s estimates by 1.9%. Company management is currently guiding for a 14.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.4% over the next 12 months, similar to its two-year rate. This projection is above average for the sector and indicates its newer products and services will help sustain its recent top-line performance.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Adjusted Operating Margin

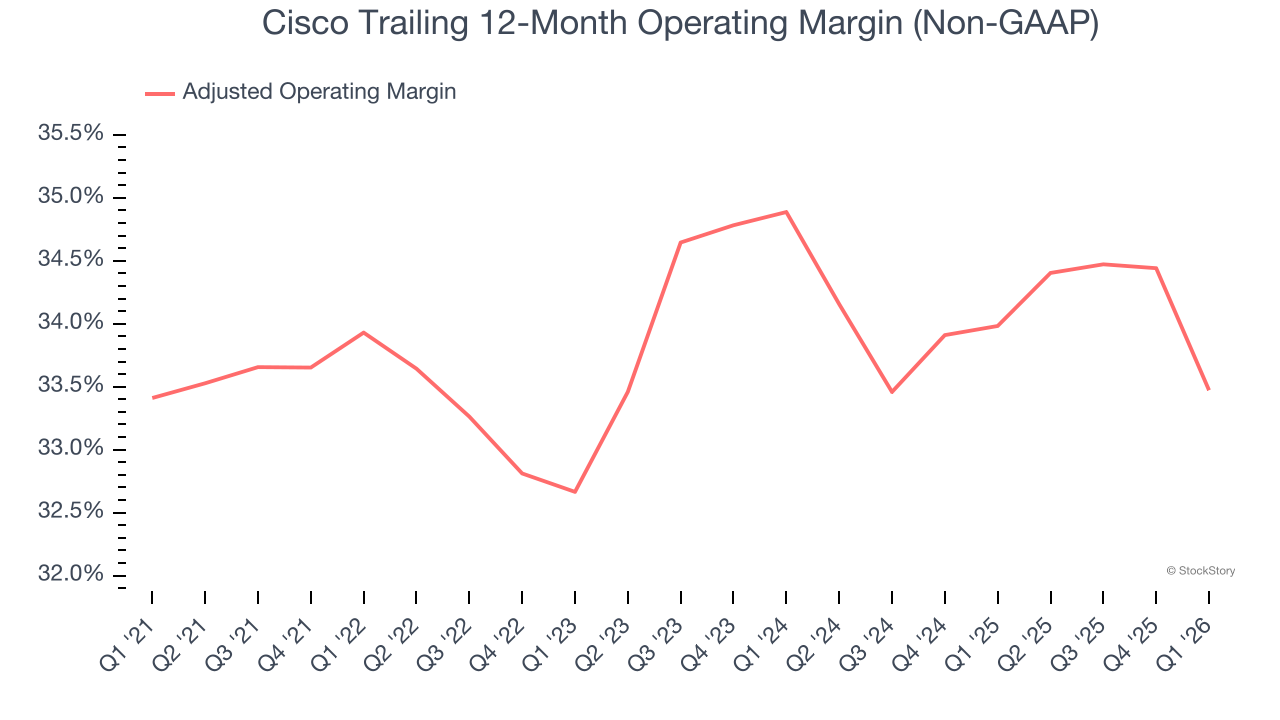

Cisco’s adjusted operating margin has more or less stayed the same over the last 12 months , averaging 33.8% over the last five years. This profitability was elite for a business services business thanks to its efficient cost structure and economies of scale.

Looking at the trend in its profitability, Cisco’s adjusted operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Cisco generated an adjusted operating margin profit margin of 30.8%, down 3.7 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

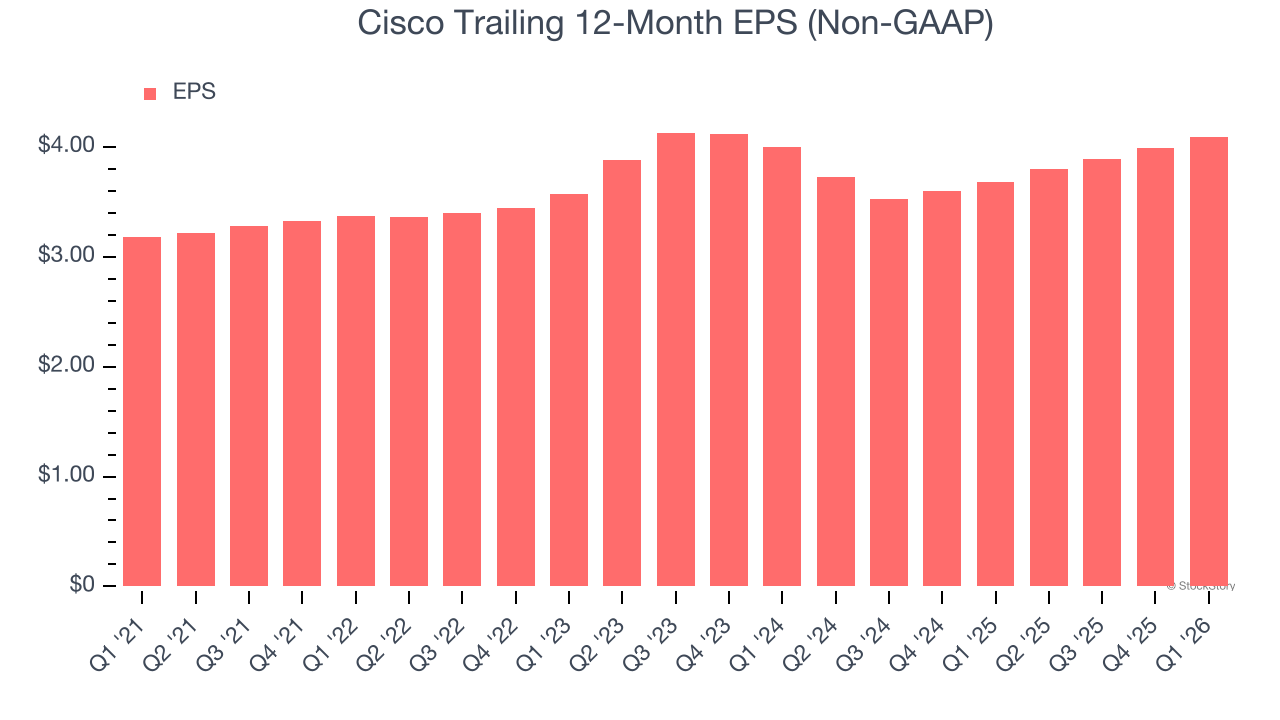

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Cisco’s unimpressive 5.2% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Cisco’s two-year annual EPS growth of 1.1% was subpar and lower than its 4.7% two-year revenue growth.

Diving into the nuances of Cisco’s earnings can give us a better understanding of its performance. Cisco’s adjusted operating margin has declined over the last two years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Cisco reported adjusted EPS of $1.06, up from $0.96 in the same quarter last year. This print beat analysts’ estimates by 2.3%. Over the next 12 months, Wall Street expects Cisco’s full-year EPS of $4.09 to grow 7.1%.

Key Takeaways from Cisco’s Q1 Results

We were impressed by how significantly Cisco blew past analysts’ EPS guidance for next quarter expectations this quarter. We were also glad its revenue guidance for next quarter trumped Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 12.3% to $115.15 immediately after reporting.

Sure, Cisco had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).