Since November 2025, Preferred Bank has been in a holding pattern, posting a small return of 1.3% while floating around $94.09. The stock also fell short of the S&P 500’s 11.3% gain during that period.

Is now the time to buy Preferred Bank, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Preferred Bank Not Exciting?

We're swiping left on Preferred Bank for now. Here are three reasons you should be careful with PFBC and a stock we'd rather own.

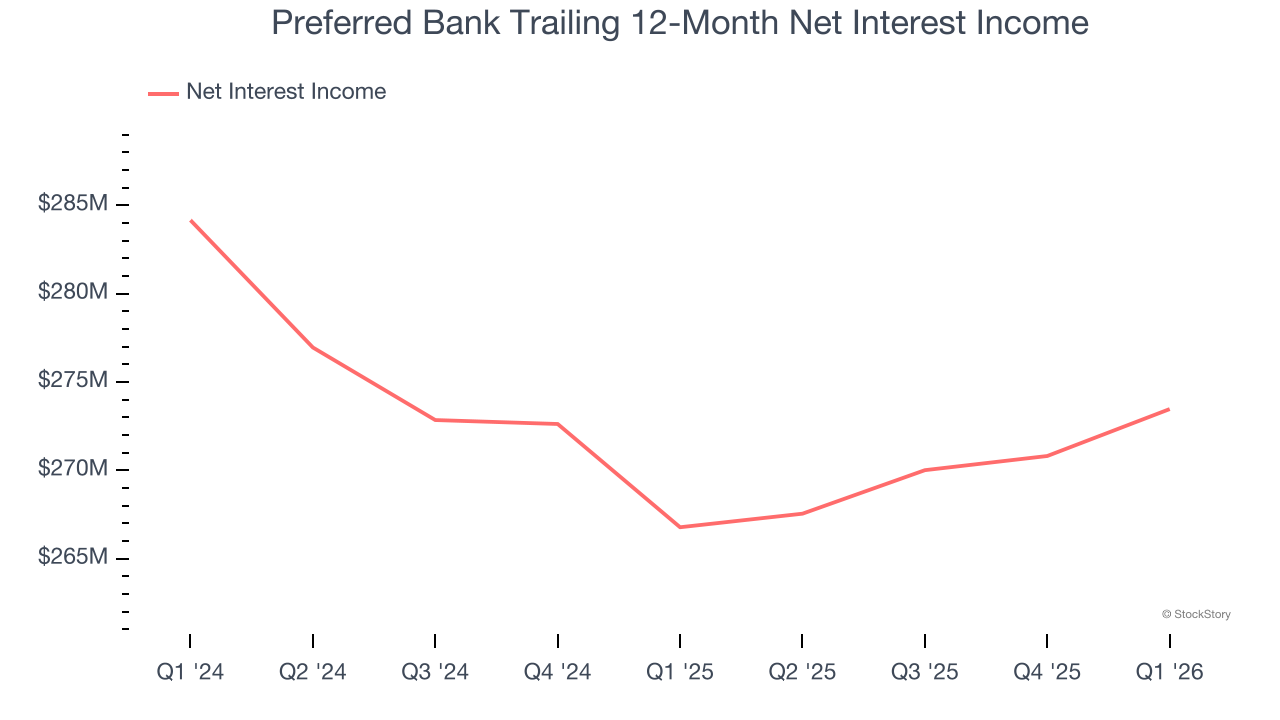

1. Net Interest Income Points to Soft Demand

While bank generate revenue from multiple sources, investors view net interest income as a cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of one-time fees.

Preferred Bank’s net interest income has grown at a 9% annualized rate over the last five years, slightly worse than the broader banking industry and in line with its total revenue.

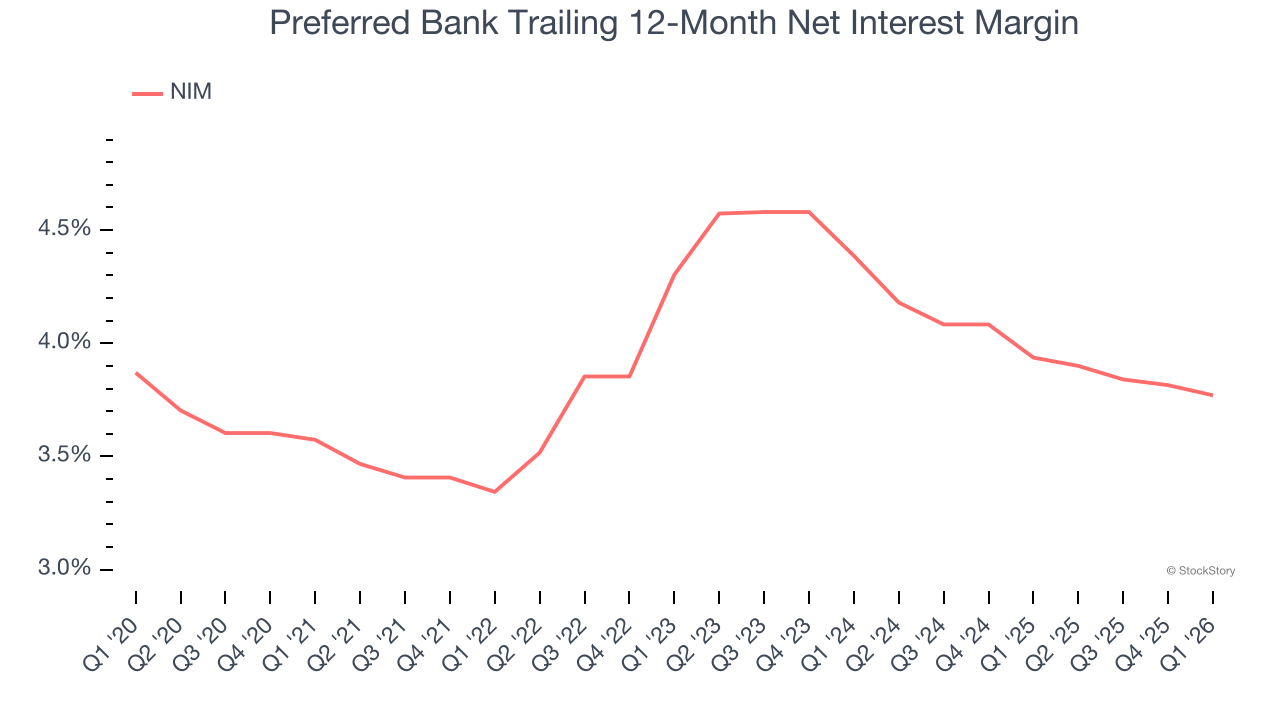

2. Net Interest Margin Dropping

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It's one of the most important metrics to track because it shows how a bank's loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, Preferred Bank’s net interest margin averaged 3.8%. However, its margin contracted by 61.7 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean Preferred Bank either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

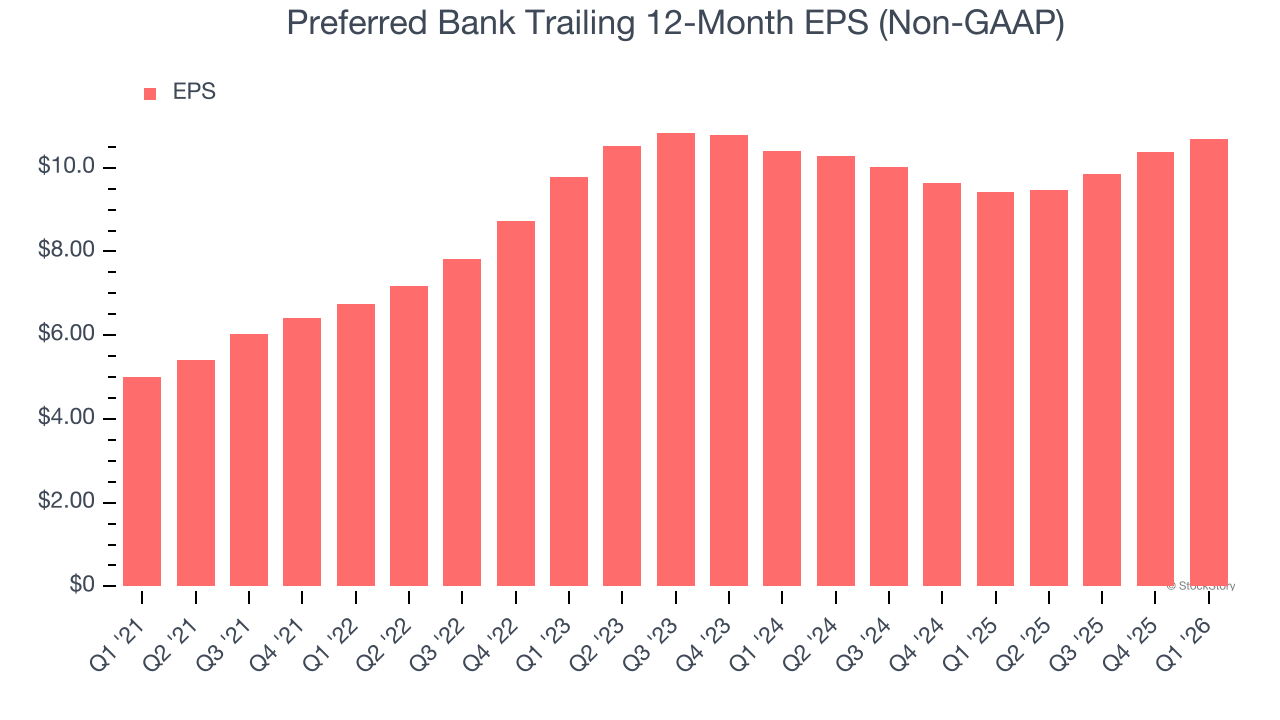

3. Recent EPS Growth Below Our Standards

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Preferred Bank’s weak 1.3% annual EPS growth over the last two years aligns with its revenue trend. On the bright side, this tells us its incremental sales were profitable.

Final Judgment

Preferred Bank isn’t a terrible business, but it isn’t one of our picks. With its shares underperforming the market lately, the stock trades at 1.3× forward P/B (or $94.09 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at the most dominant software business in the world.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month - FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.