Earnings results often indicate what direction a company will take in the months ahead. With Q1 behind us, let’s have a look at Hercules Capital (NYSE: HTGC) and its peers.

Specialty finance companies provide targeted lending or financial services for specific industries or needs. They benefit from expertise in particular sectors, often reduced competition in specialized niches, and tailored underwriting that can yield higher margins. Challenges include concentration risk in specific industries, difficulty achieving scale efficiencies, and potential vulnerability during sector-specific downturns affecting their specialized markets.

The 9 specialty finance stocks we track reported a mixed Q1. As a group, revenues beat analysts’ consensus estimates by 2.1%.

While some specialty finance stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 3.7% since the latest earnings results.

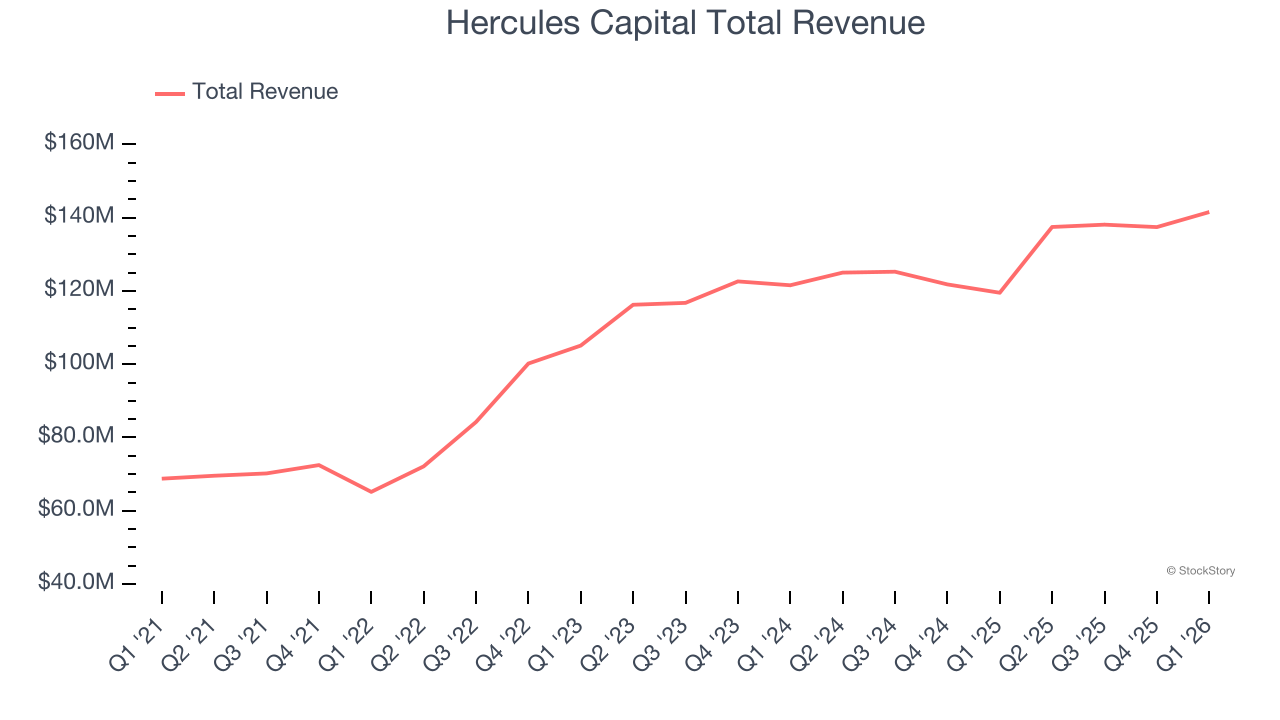

Hercules Capital (NYSE: HTGC)

Named after the mythological hero known for his strength, Hercules Capital (NYSE: HTGC) is a business development company that provides debt financing to venture capital-backed and growth-stage technology and life sciences companies.

Hercules Capital reported revenues of $141.5 million, up 18.4% year on year. This print was in line with analysts’ expectations, but overall, it was a mixed quarter for the company with EPS in line with analysts’ estimates.

Unsurprisingly, the stock is down 6.8% since reporting and currently trades at $15.45.

Is now the time to buy Hercules Capital? Access our full analysis of the earnings results here, it’s free.

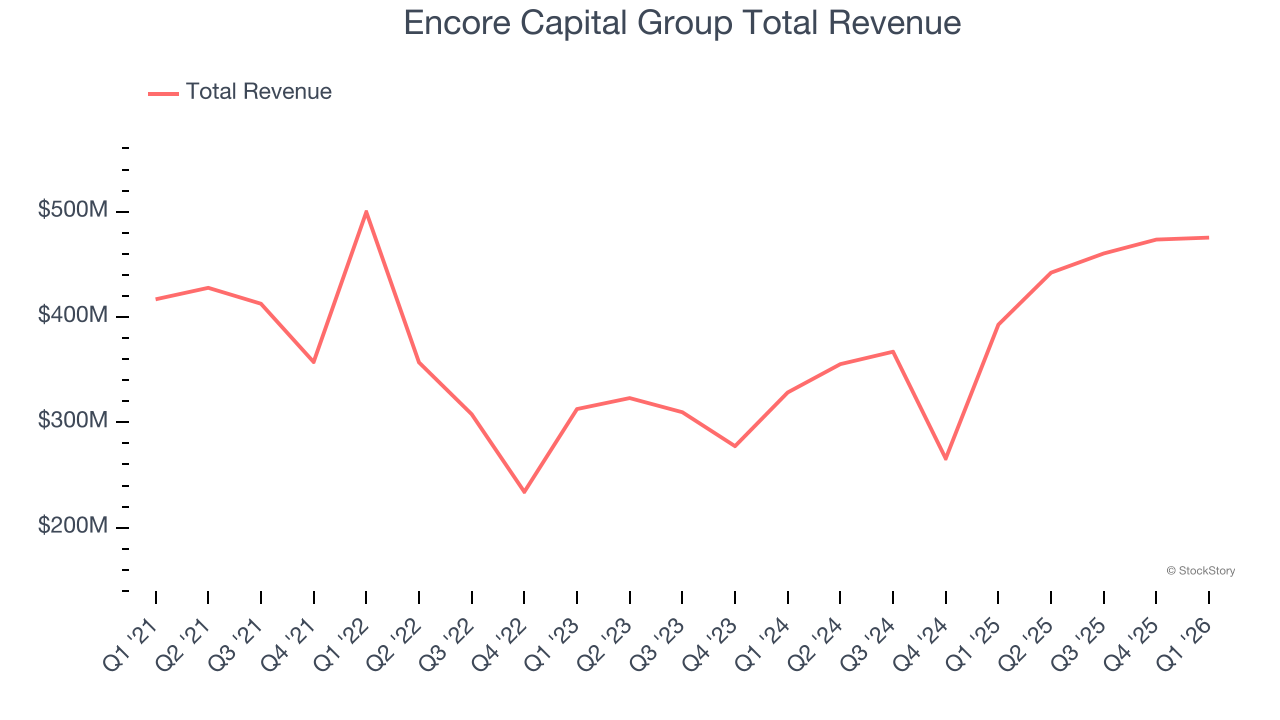

Best Q1: Encore Capital Group (NASDAQ: ECPG)

Operating in the often misunderstood world of debt collection since 1999, Encore Capital Group (NASDAQ: ECPG) purchases portfolios of defaulted consumer debt at deep discounts and works with individuals to recover these obligations while helping them toward financial recovery.

Encore Capital Group reported revenues of $475.4 million, up 21% year on year, outperforming analysts’ expectations by 6.5%. The business had a stunning quarter with a beat of analysts’ EPS and EBITDA estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 4.8% since reporting. It currently trades at $80.20.

Is now the time to buy Encore Capital Group? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Sixth Street Specialty Lending (NYSE: TSLX)

Originally launched as TPG Specialty Lending before rebranding in 2020, Sixth Street Specialty Lending (NYSE: TSLX) is a business development company that provides customized financing solutions to middle-market companies across various industries.

Sixth Street Specialty Lending reported revenues of $93.4 million, down 19.7% year on year, falling short of analysts’ expectations by 9.3%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue and EPS estimates.

Sixth Street Specialty Lending delivered the weakest performance against analyst estimates and slowest revenue growth in the group. As expected, the stock is down 12% since the results and currently trades at $17.25.

Read our full analysis of Sixth Street Specialty Lending’s results here.

Farmer Mac (NYSE: AGM)

Created by Congress in 1987 to build a bridge between Wall Street and rural America, Farmer Mac (NYSE: AGM) provides a secondary market for agricultural and rural loans, helping lenders increase their liquidity and lending capacity to serve rural America.

Farmer Mac reported revenues of $104.1 million, up 14.2% year on year. This print missed analysts’ expectations by 6%. Overall, it was a slower quarter as it also logged a significant miss of analysts’ revenue estimates.

The stock is up 3.7% since reporting and currently trades at $177.61.

Read our full, actionable report on Farmer Mac here, it’s free.

Capital Southwest (NASDAQ: CSWC)

Originally founded in 1961 as a venture capital investor that helped launch Texas Instruments, Capital Southwest (NASDAQ: CSWC) is a business development company that provides debt and equity financing to middle-market companies primarily in the United States.

Capital Southwest reported revenues of $57.77 million, up 10.2% year on year. This number came in 7% below analysts' expectations. It was a softer quarter as it also produced a significant miss of analysts’ revenue and EPS estimates.

The stock is down 2.9% since reporting and currently trades at $22.76.

Read our full, actionable report on Capital Southwest here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.