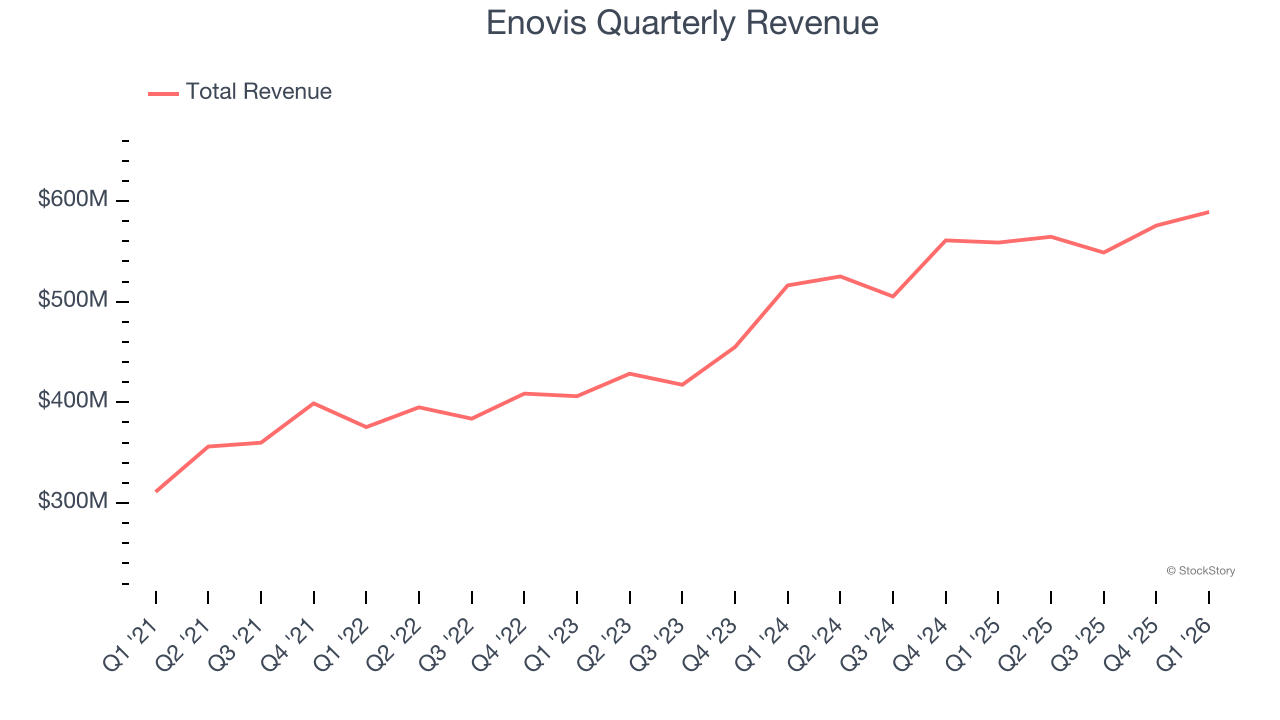

Medical technology company Enovis Corporation (NYSE: ENOV) announced better-than-expected revenue in Q1 CY2026, with sales up 5.4% year on year to $589.2 million. The company expects the full year’s revenue to be around $2.34 billion, close to analysts’ estimates. Its non-GAAP profit of $0.89 per share was 9.9% above analysts’ consensus estimates.

Is now the time to buy Enovis? Find out by accessing our full research report, it’s free.

Enovis (ENOV) Q1 CY2026 Highlights:

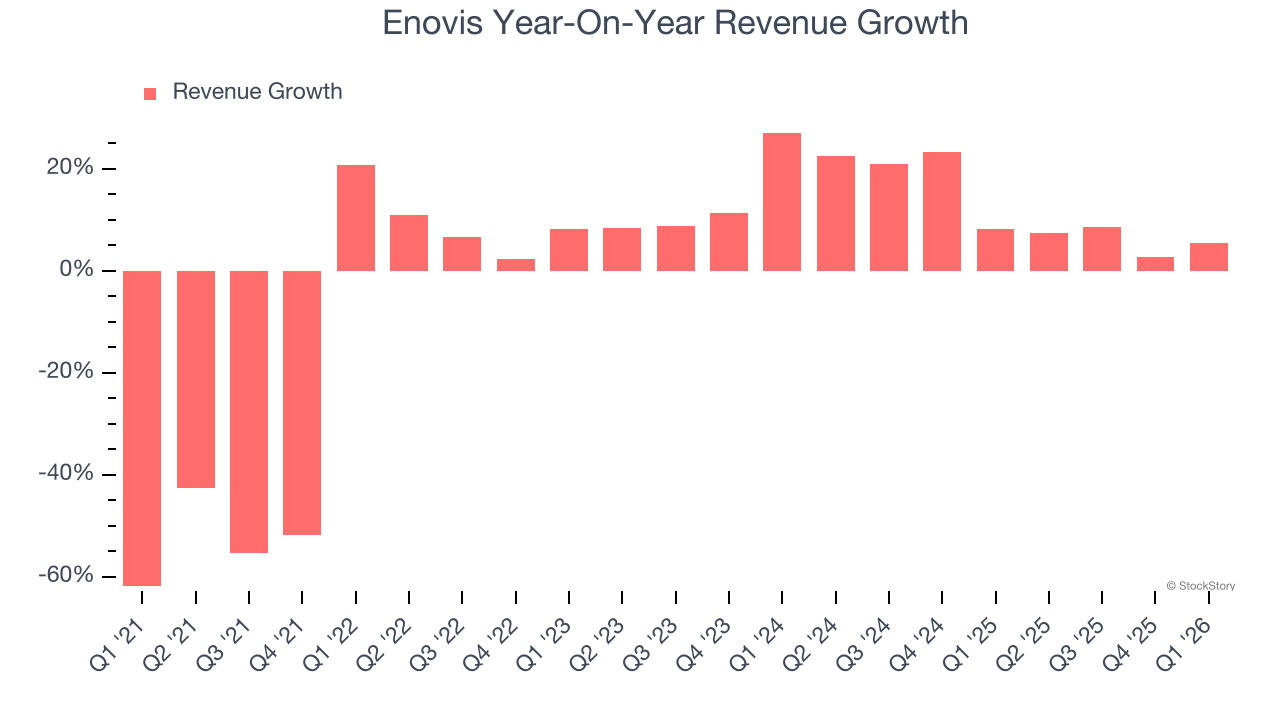

- Revenue: $589.2 million vs analyst estimates of $571.3 million (5.4% year-on-year growth, 3.1% beat)

- Adjusted EPS: $0.89 vs analyst estimates of $0.81 (9.9% beat)

- Adjusted EBITDA: $103.6 million vs analyst estimates of $96.37 million (17.6% margin, 7.5% beat)

- The company reconfirmed its revenue guidance for the full year of $2.34 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $3.63 at the midpoint

- EBITDA guidance for the full year is $430 million at the midpoint, in line with analyst expectations

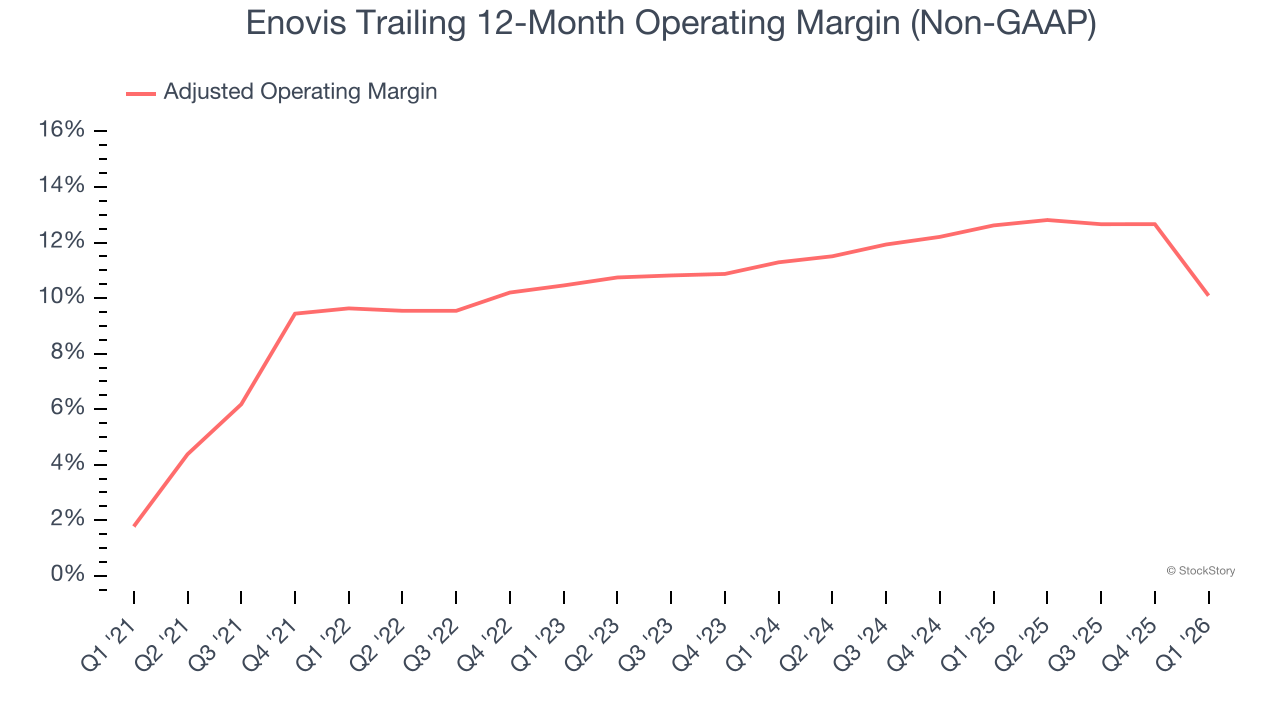

- Operating Margin: 1.1%, up from -8.4% in the same quarter last year

- Free Cash Flow was -$28.85 million compared to -$44.86 million in the same quarter last year

- Market Capitalization: $1.43 billion

"Our first-quarter results reflect solid execution and continued progress advancing our innovation-led strategy,” said Damien McDonald, Chief Executive Officer of Enovis.

Company Overview

With a focus on helping patients regain or maintain their natural motion, Enovis (NYSE: ENOV) develops and manufactures medical devices for orthopedic care, from injury prevention and pain management to joint replacement and rehabilitation.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Enovis’s demand was weak over the last five years as its sales fell at a 2.3% annual rate. This was below our standards and suggests it’s a low quality business.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Enovis’s annualized revenue growth of 12% over the last two years is above its five-year trend, suggesting some bright spots.

This quarter, Enovis reported year-on-year revenue growth of 5.4%, and its $589.2 million of revenue exceeded Wall Street’s estimates by 3.1%.

Looking ahead, sell-side analysts expect revenue to grow 4.3% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will see some demand headwinds.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted Operating Margin

Enovis’s adjusted operating margin has generally stayed the same over the last 12 months, averaging 10.9% over the last five years. This profitability was higher than the broader healthcare sector, showing it did a decent job managing its expenses.

Analyzing the trend in its profitability, Enovis’s adjusted operating margin of 10.1% for the trailing 12 months may be around the same as five years ago, but it has decreased by 1.2 percentage points over the last two years.

In Q1, Enovis generated an adjusted operating margin profit margin of 2.6%, down 10 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

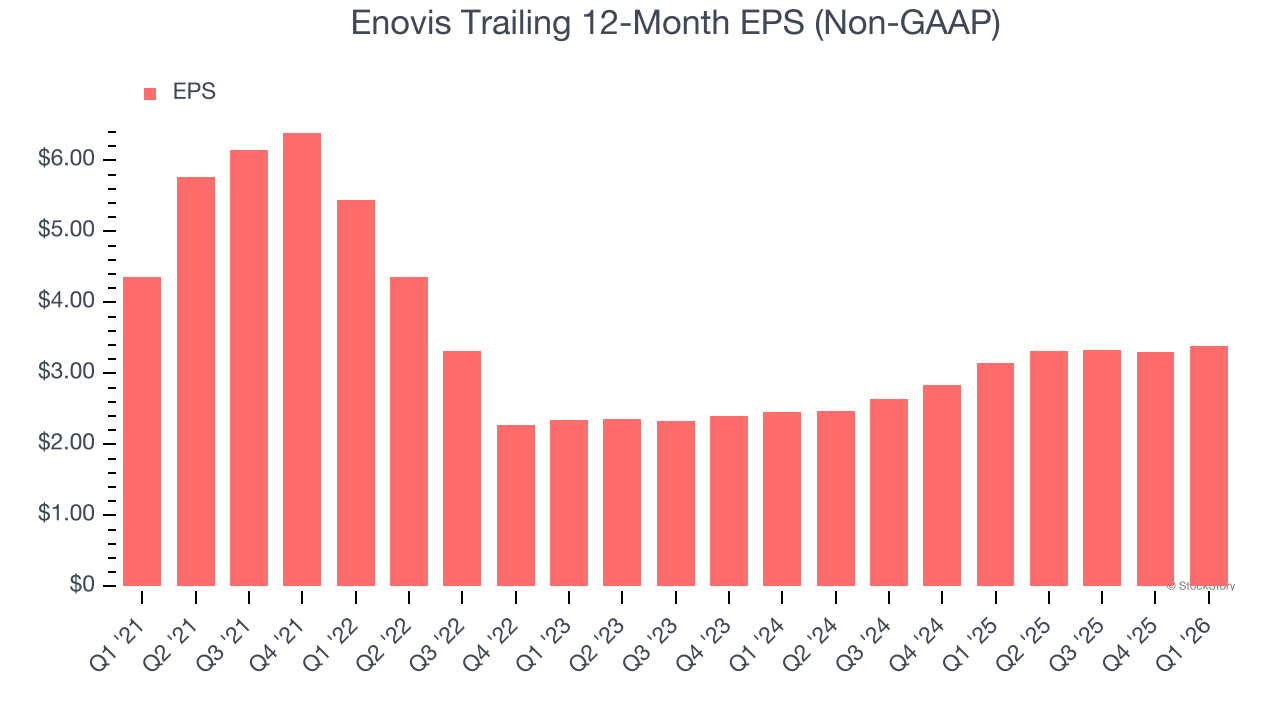

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Enovis, its EPS declined by 4.9% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

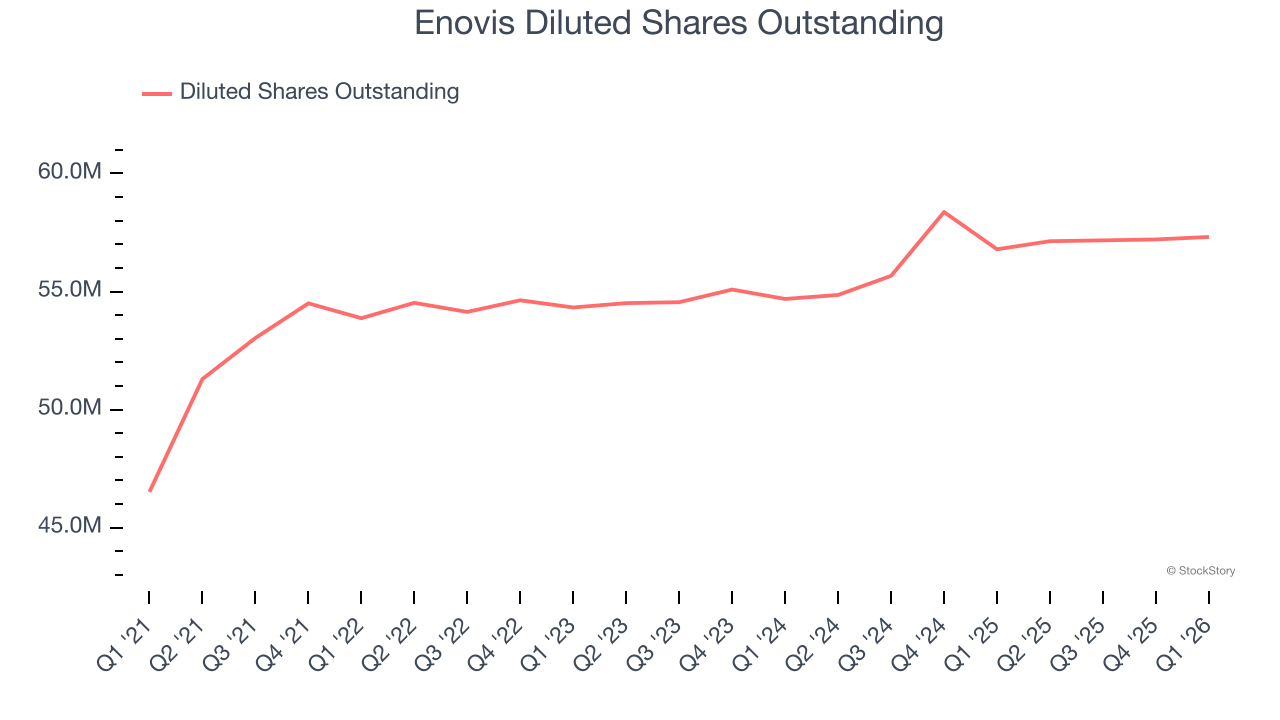

We can take a deeper look into Enovis’s earnings to better understand the drivers of its performance. A five-year view shows Enovis has diluted its shareholders, growing its share count by 23.2%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, Enovis reported adjusted EPS of $0.89, up from $0.81 in the same quarter last year. This print beat analysts’ estimates by 9.9%. Over the next 12 months, Wall Street expects Enovis’s full-year EPS of $3.38 to grow 11.6%.

Key Takeaways from Enovis’s Q1 Results

We enjoyed seeing Enovis beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock traded up 3.7% to $25.76 immediately after reporting.

Is Enovis an attractive investment opportunity at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).