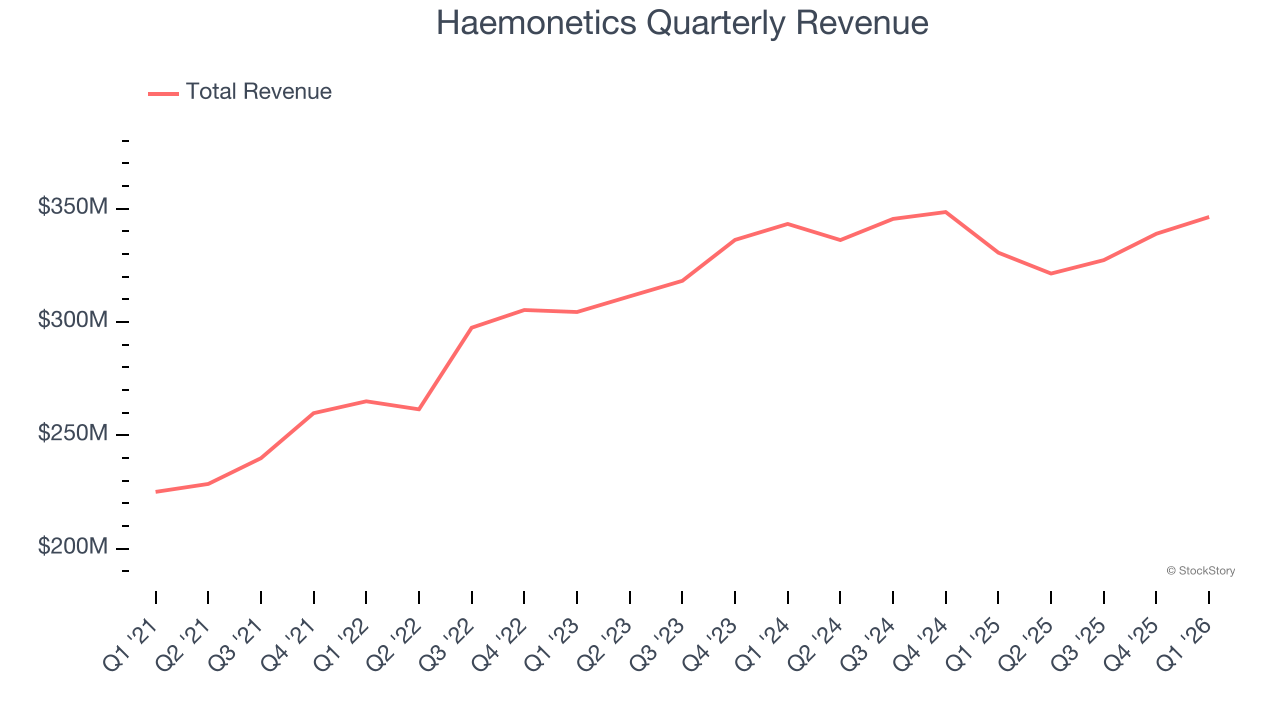

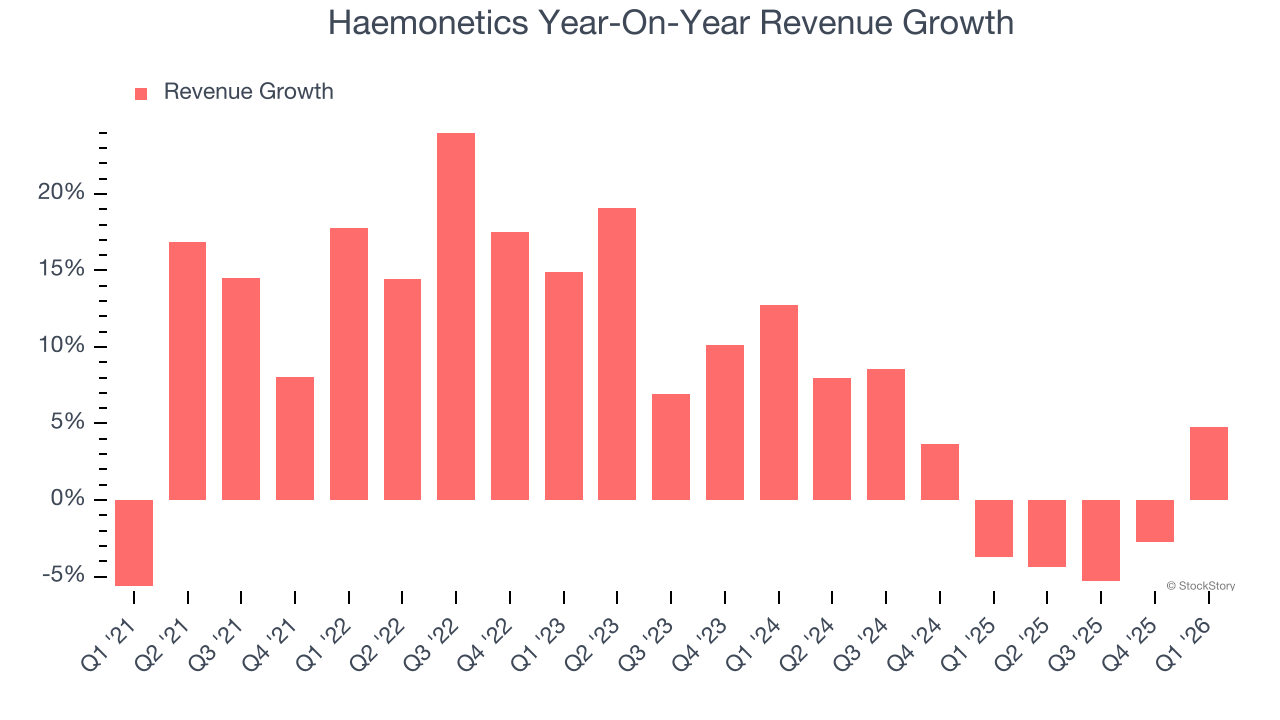

Blood products company Haemonetics (NYSE: HAE). reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 4.8% year on year to $346.4 million. Its non-GAAP profit of $1.29 per share was 1.4% above analysts’ consensus estimates.

Is now the time to buy Haemonetics? Find out by accessing our full research report, it’s free.

Haemonetics (HAE) Q1 CY2026 Highlights:

- Revenue: $346.4 million vs analyst estimates of $336.1 million (4.8% year-on-year growth, 3% beat)

- Adjusted EPS: $1.29 vs analyst estimates of $1.27 (1.4% beat)

- Operating Margin: -6.6%, down from 21.6% in the same quarter last year

- Free Cash Flow Margin: 15.4%, down from 30.5% in the same quarter last year

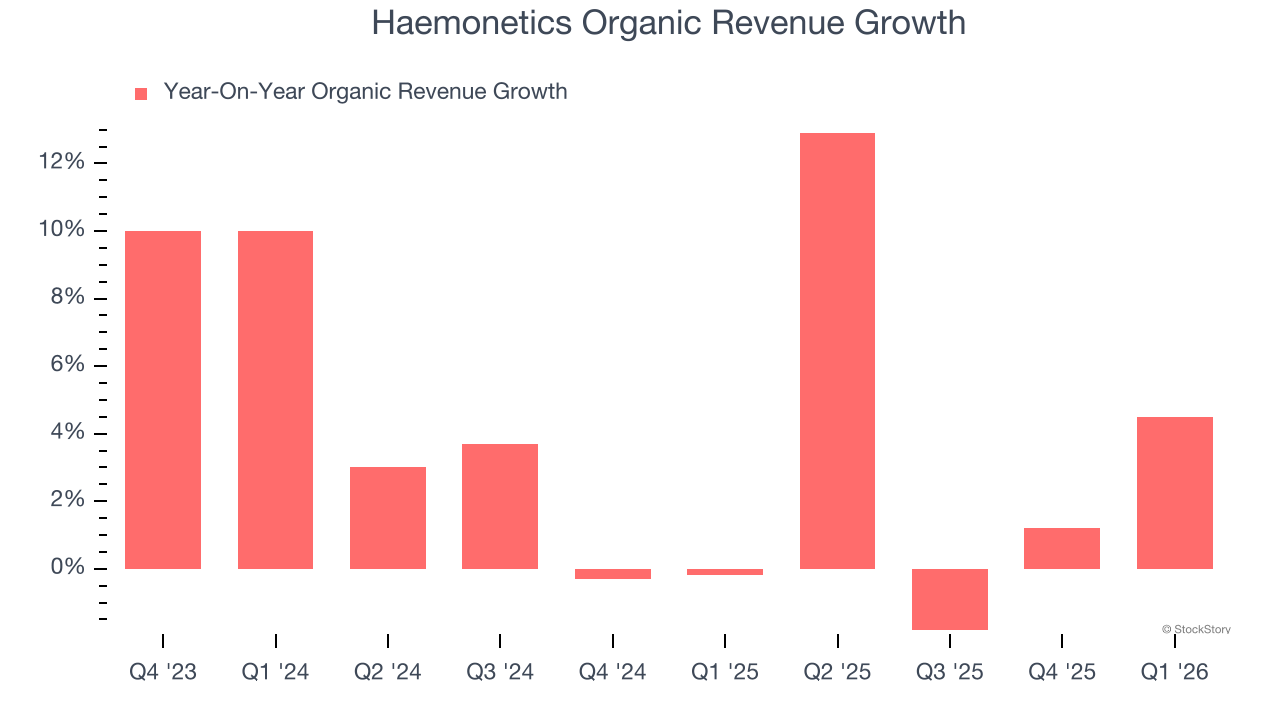

- Organic Revenue rose 4.5% year on year (beat)

- Market Capitalization: $2.45 billion

Company Overview

With roots dating back to 1971 and a mission to improve blood-related healthcare, Haemonetics (NYSE: HAE) provides specialized medical devices and software for blood collection, processing, and management across plasma centers, blood banks, and hospitals.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Haemonetics grew its sales at a decent 8.9% compounded annual growth rate. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Haemonetics’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

Haemonetics also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Haemonetics’s organic revenue averaged 2.9% year-on-year growth. Because this number is better than its two-year revenue growth, we can see that some mixture of divestitures and foreign exchange rates dampened its headline results.

This quarter, Haemonetics reported modest year-on-year revenue growth of 4.8% but beat Wall Street’s estimates by 3%.

Looking ahead, sell-side analysts expect revenue to grow 4.5% over the next 12 months. While this projection implies its newer products and services will catalyze better top-line performance, it is still below average for the sector.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

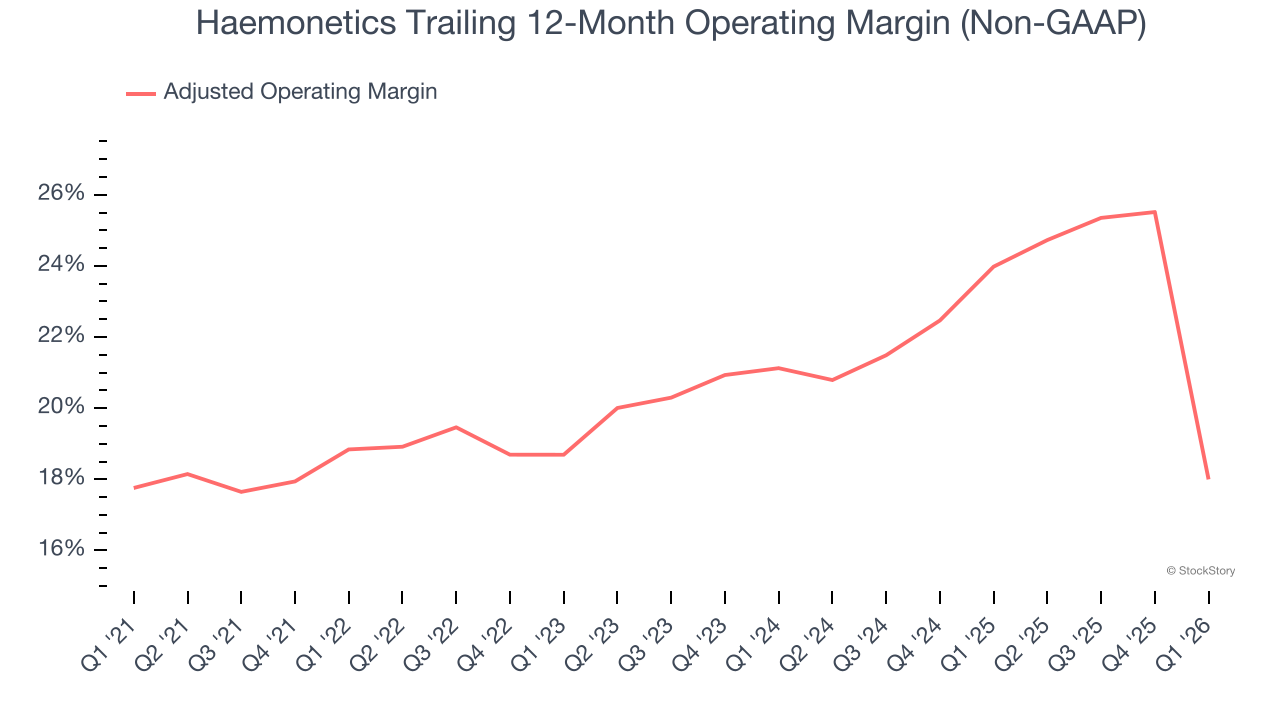

Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

Haemonetics’s adjusted operating margin has generally stayed the same over the last 12 months, averaging 20.2% over the last five years. This profitability was top-notch for a healthcare business, showing it’s an well-run company with an efficient cost structure.

Analyzing the trend in its profitability, Haemonetics’s adjusted operating margin of 18% for the trailing 12 months may be around the same as five years ago, but it has decreased by 3.1 percentage points over the last two years. This dynamic unfolded because it struggled to adjust its fixed costs while its demand plateaued.

In Q1, Haemonetics generated an adjusted operating margin profit margin of negative 4%, down 28.9 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

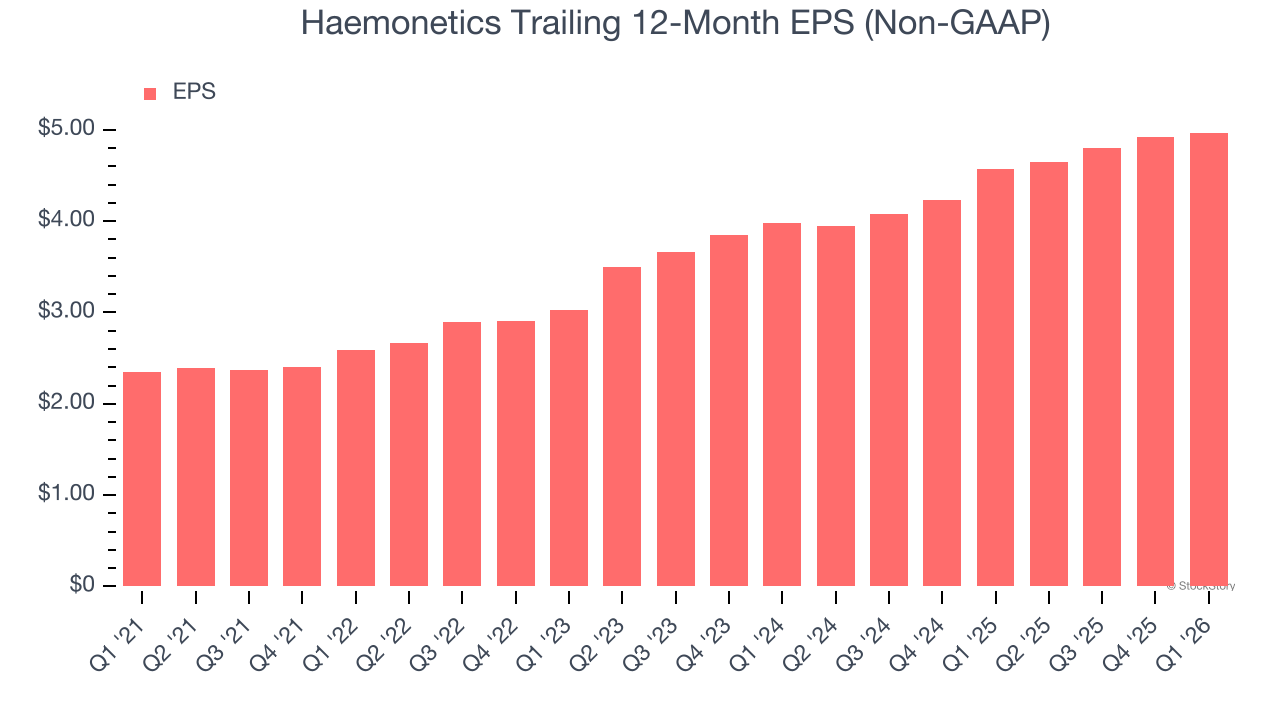

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Haemonetics’s EPS grew at 16.2% compounded annual growth rate over the last five years, higher than its 8.9% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its adjusted operating margin didn’t improve.

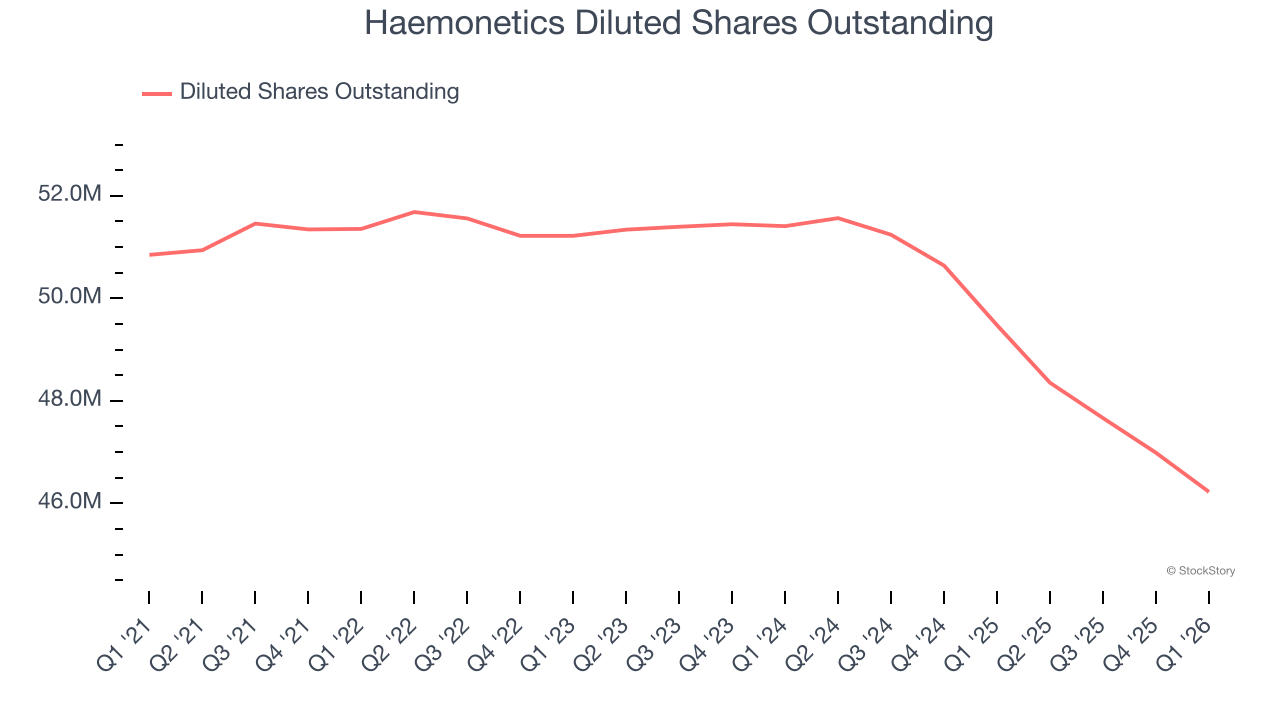

Diving into Haemonetics’s quality of earnings can give us a better understanding of its performance. A five-year view shows that Haemonetics has repurchased its stock, shrinking its share count by 9.1%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q1, Haemonetics reported adjusted EPS of $1.29, up from $1.24 in the same quarter last year. This print beat analysts’ estimates by 1.4%. Over the next 12 months, Wall Street expects Haemonetics’s full-year EPS of $4.97 to grow 6.4%.

Key Takeaways from Haemonetics’s Q1 Results

We enjoyed seeing Haemonetics beat analysts’ organic revenue expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Overall, we think this was a solid quarter with some key areas of upside. Investors were likely hoping for more, and shares traded down 1.2% to $52 immediately following the results.

So do we think Haemonetics is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).