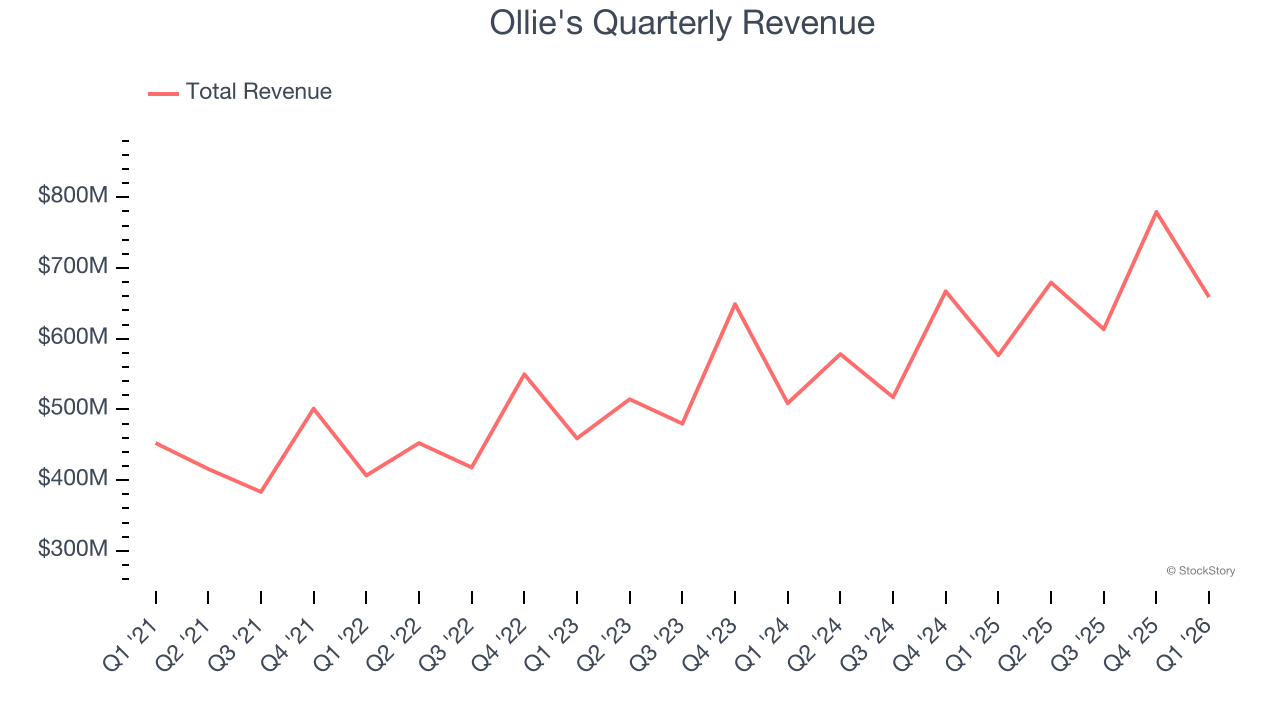

Discount retail company Ollie’s Bargain Outlet (NASDAQ: OLLI) missed Wall Street’s revenue expectations in Q1 CY2026, but sales rose 14.2% year on year to $658.9 million. On the other hand, the company’s outlook for the full year was close to analysts’ estimates with revenue guided to $2.99 billion at the midpoint. Its non-GAAP profit of $0.91 per share was 4.4% above analysts’ consensus estimates.

Is now the time to buy Ollie's? Find out by accessing our full research report, it’s free.

Ollie's (OLLI) Q1 CY2026 Highlights:

- Revenue: $658.9 million vs analyst estimates of $663.5 million (14.2% year-on-year growth, 0.7% miss)

- Adjusted EPS: $0.91 vs analyst estimates of $0.87 (4.4% beat)

- The company reconfirmed its revenue guidance for the full year of $2.99 billion at the midpoint

- Management raised its full-year Adjusted EPS guidance to $4.50 at the midpoint, a 1.1% increase

- Operating Margin: 10.6%, in line with the same quarter last year

- Free Cash Flow Margin: 3%, up from 0.3% in the same quarter last year

- Locations: 672 at quarter end, up from 584 in the same quarter last year

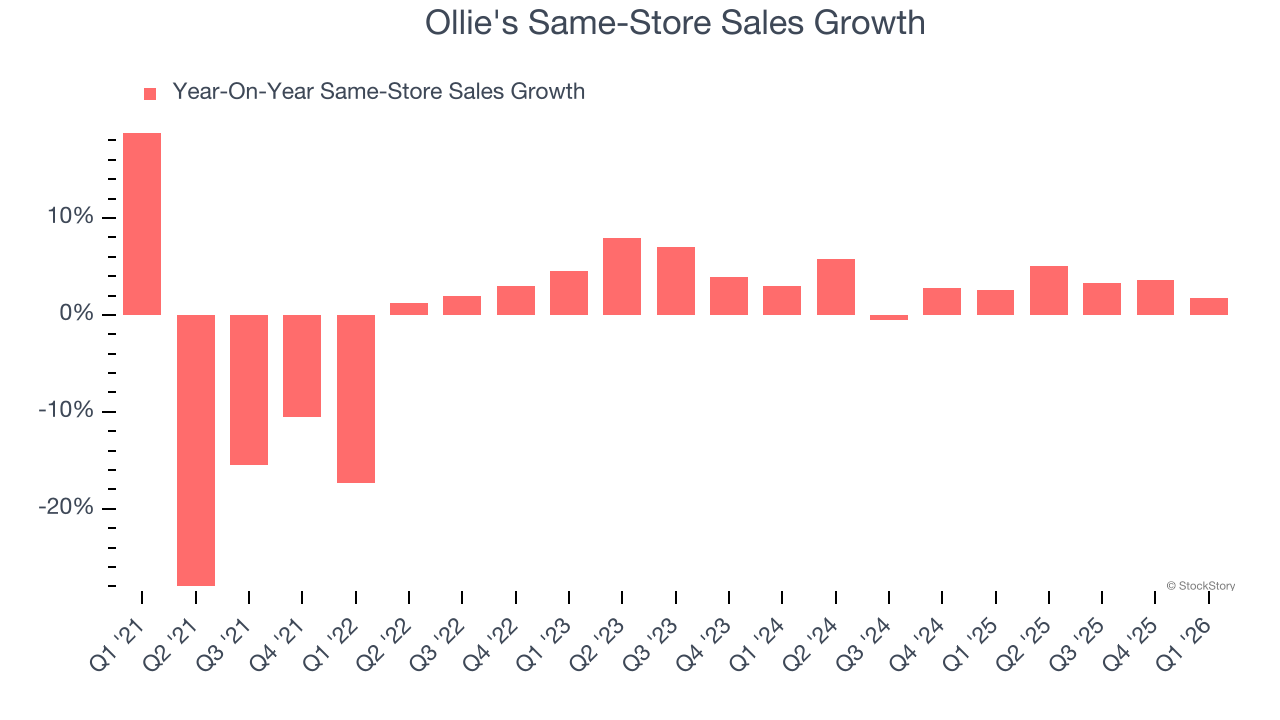

- Same-Store Sales rose 1.7% year on year, in line with the same quarter last year

- Market Capitalization: $4.81 billion

“We are very pleased with our first quarter results and the outstanding performance of our team,” said Eric van der Valk, President and Chief Executive Officer.

Company Overview

Often located in suburban or semi-rural shopping centers, Ollie’s Bargain Outlet (NASDAQ: OLLI) is a discount retailer that acquires excess inventory then sells at meaningful discounts.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $2.73 billion in revenue over the past 12 months, Ollie's is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers. On the bright side, it can grow faster because it has more white space to build new stores.

As you can see below, Ollie's grew its sales at a solid 13.3% compounded annual growth rate over the last three years as it opened new stores and increased sales at existing, established locations.

This quarter, Ollie’s revenue grew by 14.2% year on year to $658.9 million but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 12.8% over the next 12 months, similar to its three-year rate. This projection is eye-popping and suggests the market sees success for its products.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Store Performance

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

Ollie's sported 672 locations in the latest quarter. Over the last two years, it has opened new stores at a rapid clip by averaging 13.1% annual growth, among the fastest in the consumer retail sector. This gives it a chance to scale into a mid-sized business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

A company’s store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Ollie’s demand has been healthy for a retailer over the last two years. On average, the company has grown its same-store sales by a robust 3% per year. This performance gives it the confidence to meaningfully expand its store base.

In the latest quarter, Ollie’s same-store sales rose 1.7% year on year. This growth was a deceleration from its historical levels, showing the business is still performing well but losing a bit of steam.

Key Takeaways from Ollie’s Q1 Results

While revenue missed, full-year revenue guidance was reaffirmed. EPS beat and EPS guidance was raised. Overall, this print had some key positives. The stock traded up 7.4% to $85.10 immediately following the results.

Is Ollie's an attractive investment opportunity right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).