Since July 2021, the S&P 500 has delivered a total return of 74.3%. But one standout stock has nearly doubled the market - over the past five years, Nicolet Bankshares has surged 132% to $165.54 per share. Its momentum hasn’t stopped as it’s also gained 25.9% in the last six months thanks to its solid quarterly results, beating the S&P by 17.2%.

Following the strength, is NIC a buy right now? Or is the market overestimating its value? Find out in our full research report, it’s free.

Why Is Nicolet Bankshares a Good Business?

Starting as Green Bay Financial Corporation in 2000 before rebranding in 2002, Nicolet Bankshares (NYSE: NIC) is a regional bank holding company that provides commercial, agricultural, and consumer banking services primarily in Wisconsin, Michigan, and Minnesota.

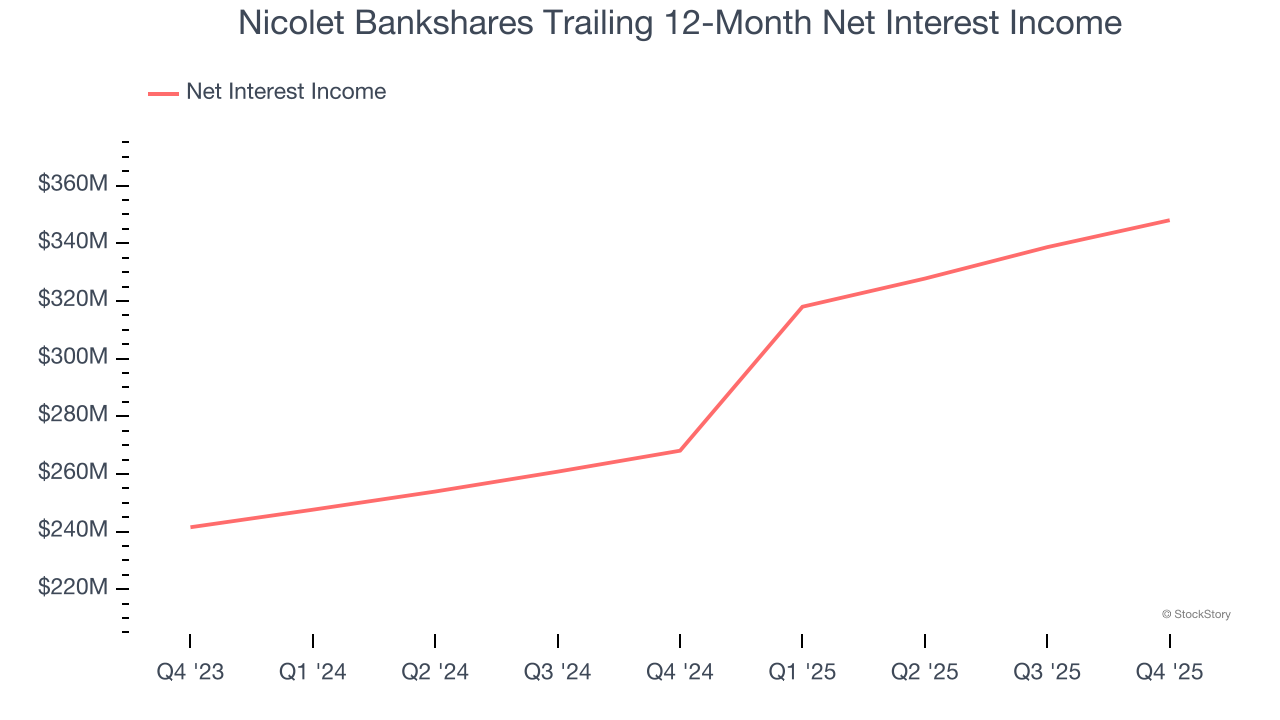

1. Net Interest Income Skyrockets, Fueling Growth Opportunities

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Nicolet Bankshares’s net interest income has grown at a 21.9% annualized rate over the last five years, much better than the broader banking industry and faster than its total revenue.

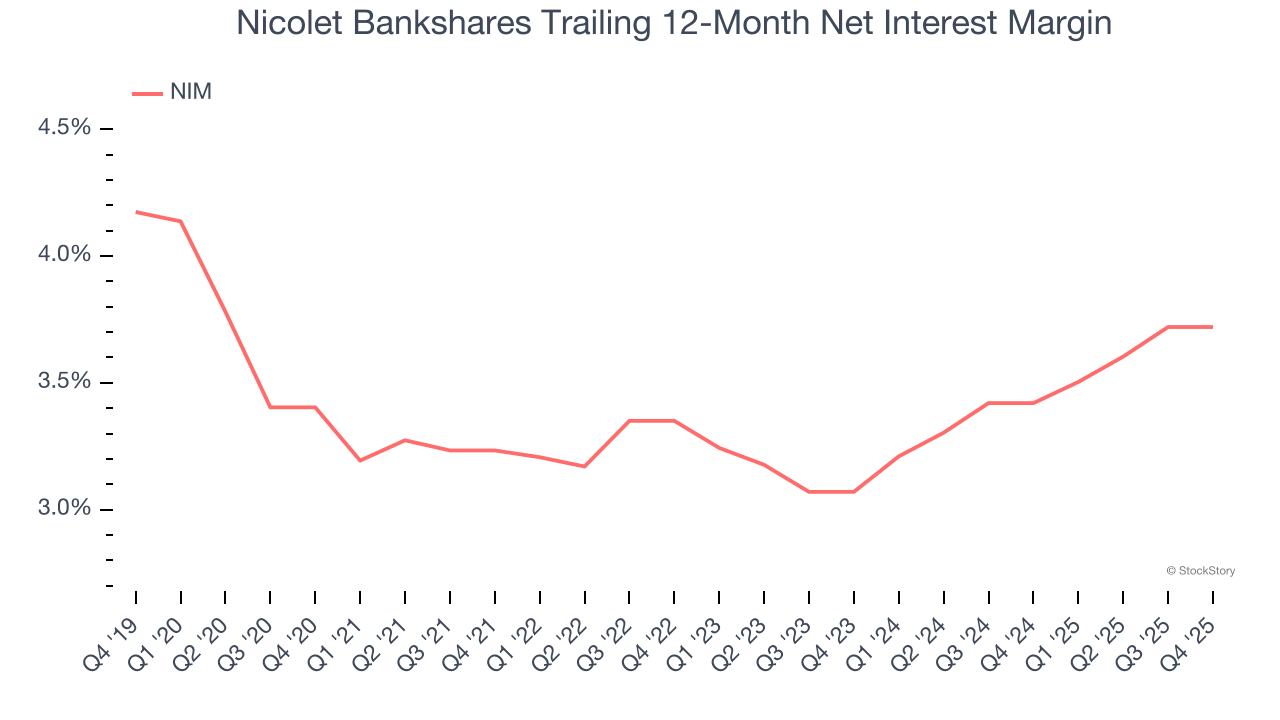

2. Increasing Net Interest Margin Juices Financials

The net interest margin (NIM) is a key profitability indicator that measures the difference between what a bank earns on its loans and what it pays on its deposits. This metric measures how efficiently it can generate income from its core lending activities.

Over the past two years, Nicolet Bankshares’s net interest margin averaged 3.6%, climbing by 65 basis points (100 basis points = 1 percentage point) over that period.

This expansion was a tailwind for its net interest income, and while prevailing interest rates matter the most for industry net interest margins, banks that consistently increase this figure generally boast higher-earning loan books (all else equal such as the risk of those loans) or provide differentiated services that give them the ability to charge higher rates (pricing power).

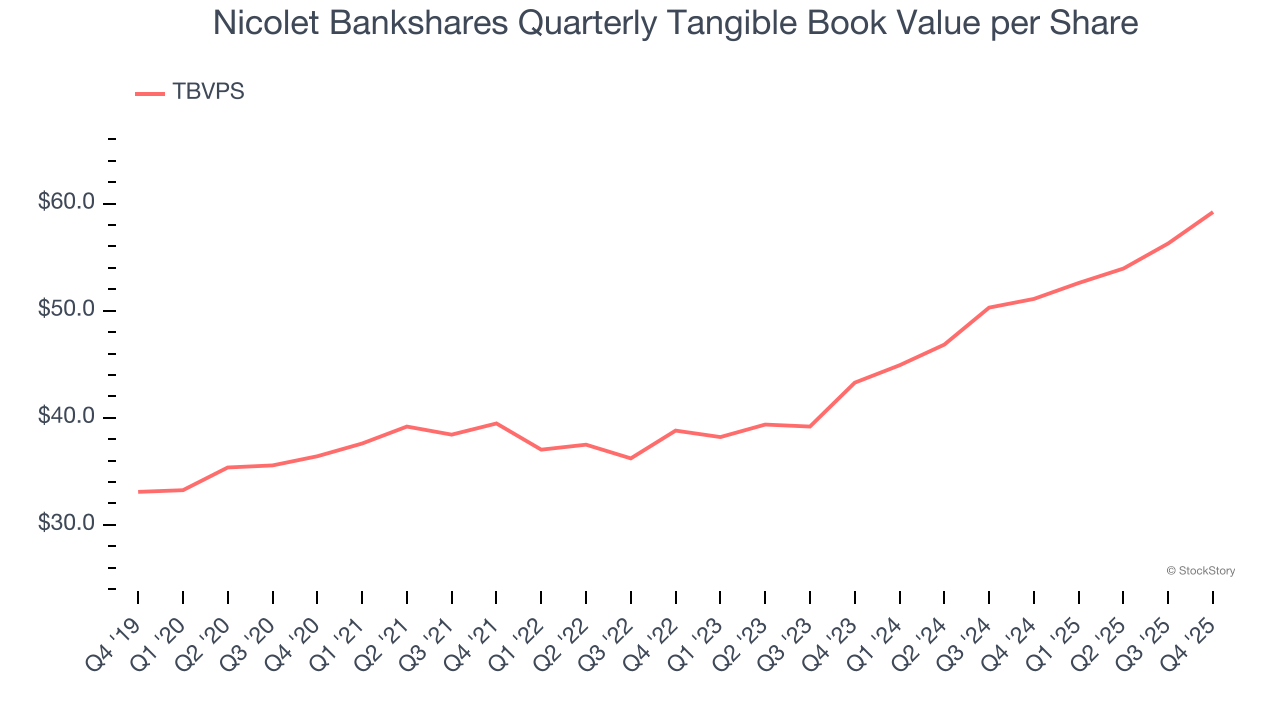

3. Growing TBVPS Reflects Strong Asset Base

In the banking industry, tangible book value per share (TBVPS) provides the clearest picture of shareholder value, as it focuses on concrete assets while excluding intangible items that may not hold value during challenging times.

Nicolet Bankshares’s TBVPS increased by 10.2% annually over the last five years, and growth has recently accelerated as TBVPS grew at an excellent 17% annual clip over the past two years (from $43.28 to $59.21 per share).

Final Judgment

These are just a few reasons Nicolet Bankshares is a rock-solid business worth owning, and with its shares beating the market recently, the stock trades at 1.5× forward P/B (or $165.54 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,460% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,552% between June 2020 and June 2025). Find your next big winner with StockStory today.