People’s 15.9% return over the past six months has outpaced the S&P 500 by 7.2%, and its stock price has climbed to $45.79 per share. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in People, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think People Will Underperform?

We’re happy investors have made money, but we’re cautious about People. Here are three reasons why PPLI doesn’t excite us, plus one stock we’d rather own.

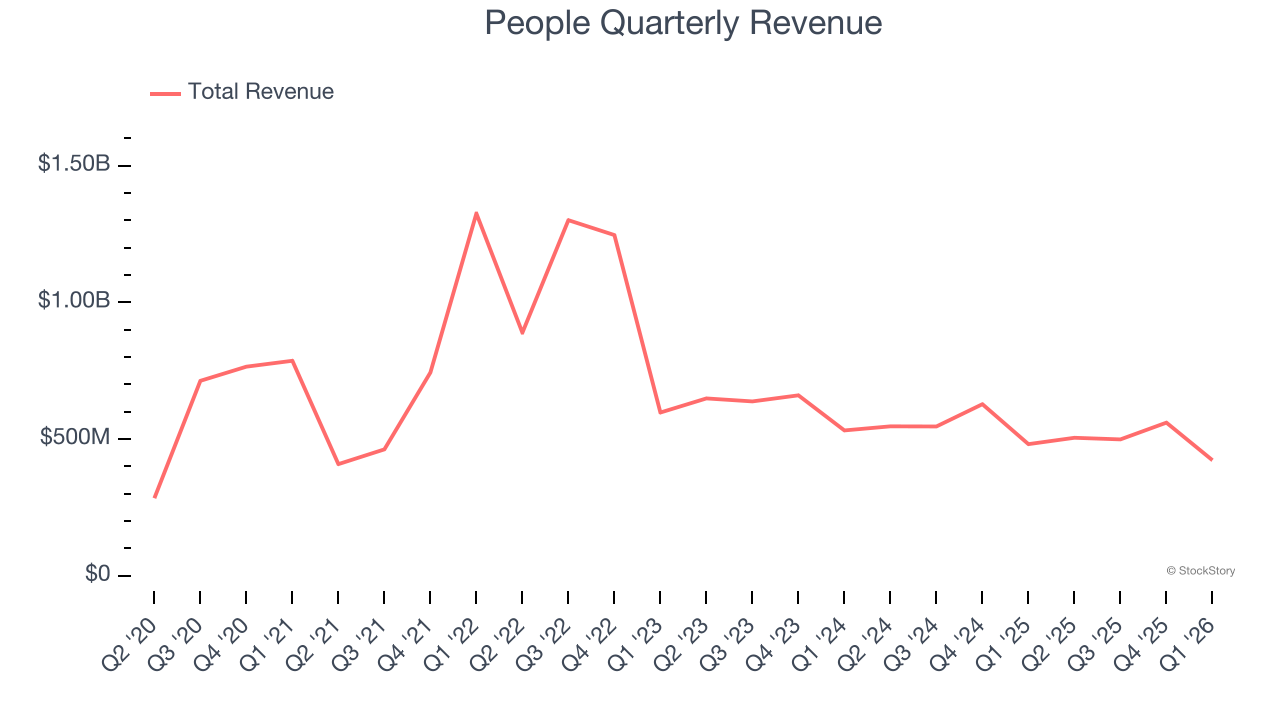

1. Revenue Spiraling Downwards

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, People’s demand was weak and its revenue declined by 4.9% per year. This was below our standards and is a sign of poor business quality.

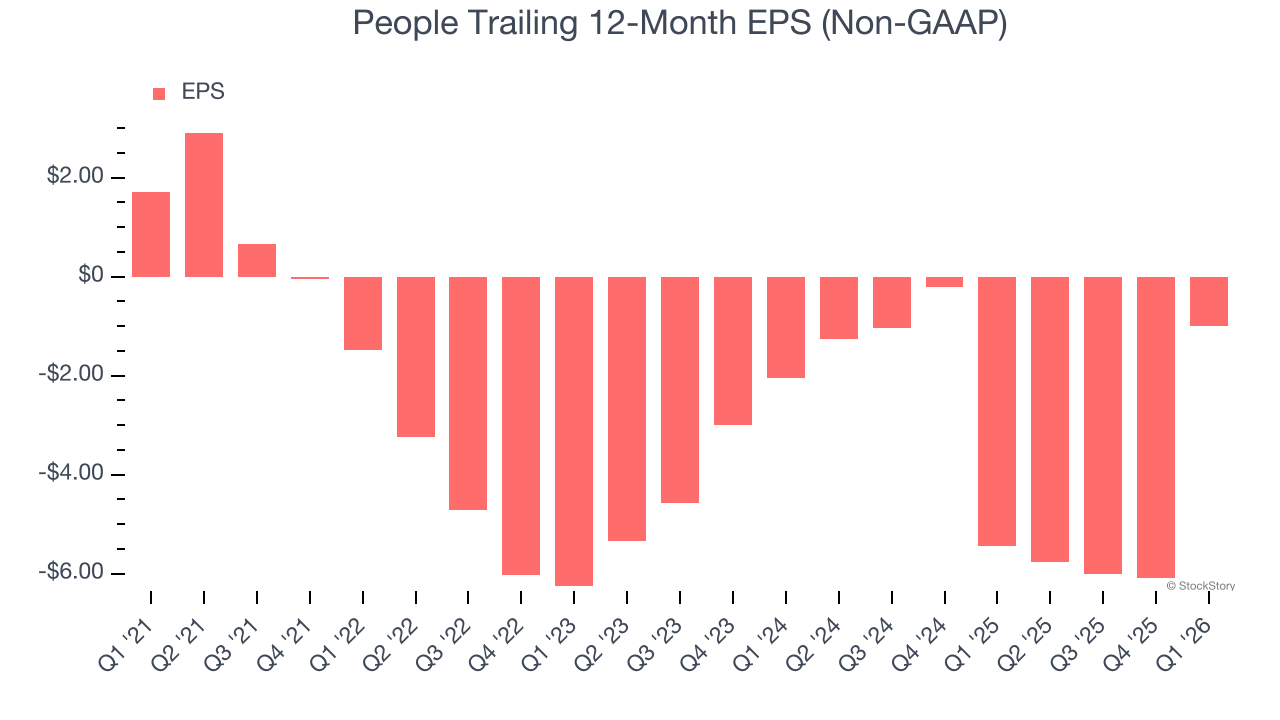

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for People, its EPS declined by 21% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

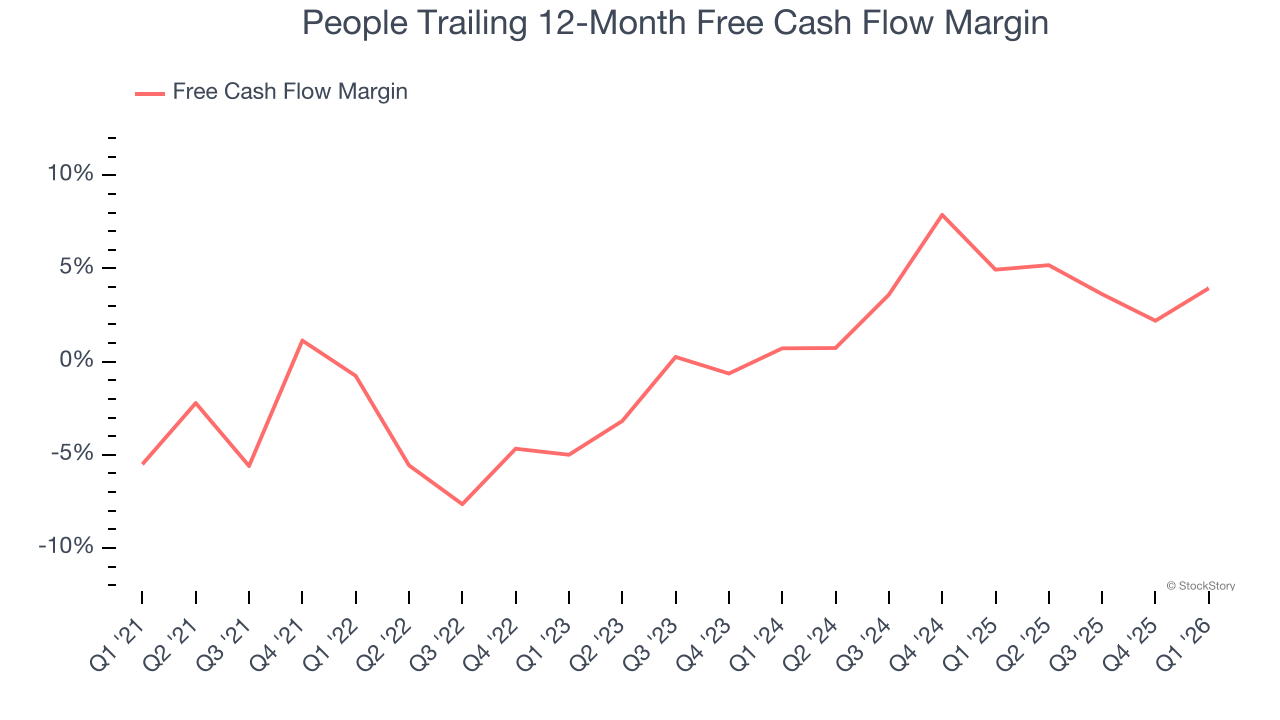

3. Breakeven Free Cash Flow Limits Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

People broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

Final Judgment

People doesn’t pass our quality test. With its shares topping the market in recent months, the stock trades at 19.1× forward P/E (or $45.79 per share). This valuation tells us a lot of optimism is priced in - you can find more timely opportunities elsewhere. Let us point you toward one of our top software and edge computing picks.

Stocks We Like More Than People

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,460% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+271% between June 2020 and June 2025). Find your next big winner with StockStory today.