Over the past six months, Coursera’s stock price fell to $5.90. Shareholders have lost 18.8% of their capital, which is disappointing considering the S&P 500 has climbed by 7.7%. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Given the weaker price action, is now the time to buy COUR? Find out in our full research report, it’s free.

Why Does Coursera Spark Debate?

Founded by two Stanford University computer science professors, Coursera (NYSE: COUR) is an online learning platform that offers courses, specializations, and degrees from top universities and organizations around the world.

Two Things to Like:

1. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Coursera’s revenue to rise by 82.6%, an improvement versus This projection is eye-popping and indicates its newer products and services will spur better top-line performance.

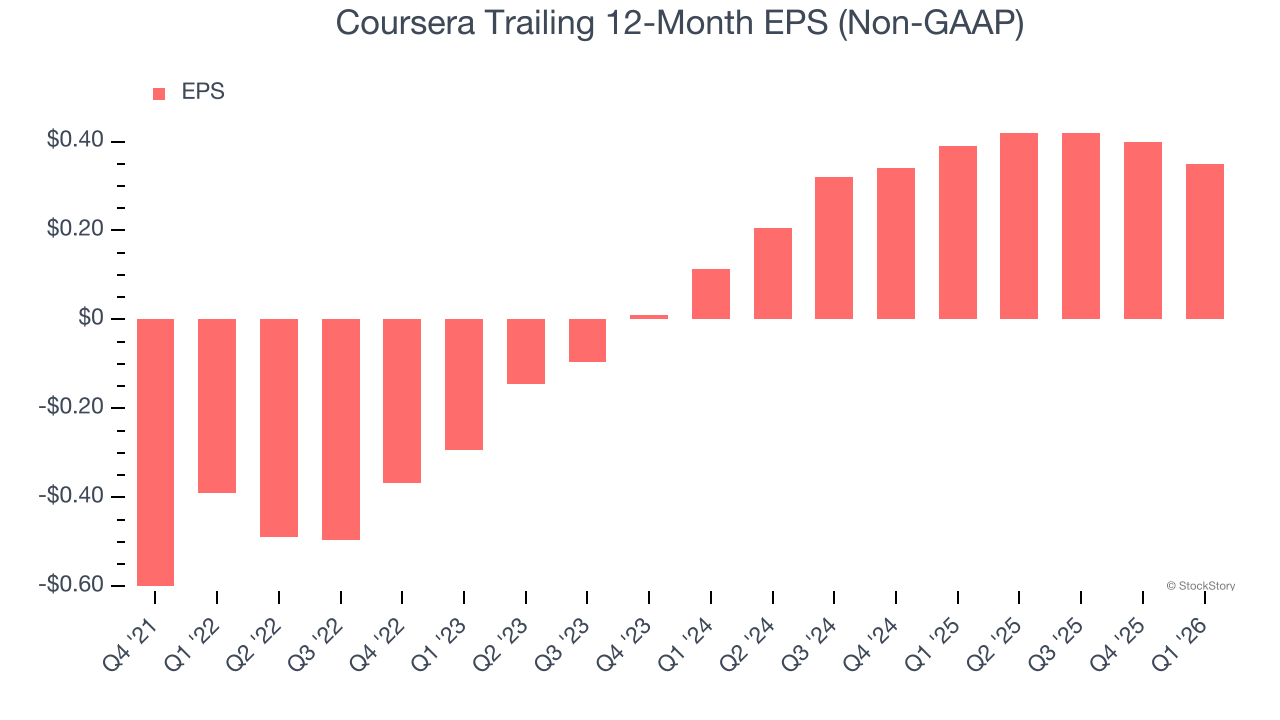

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Coursera’s full-year EPS flipped from negative to positive over the last three years. This is a good sign and shows it’s at an inflection point.

One Reason to Be Careful:

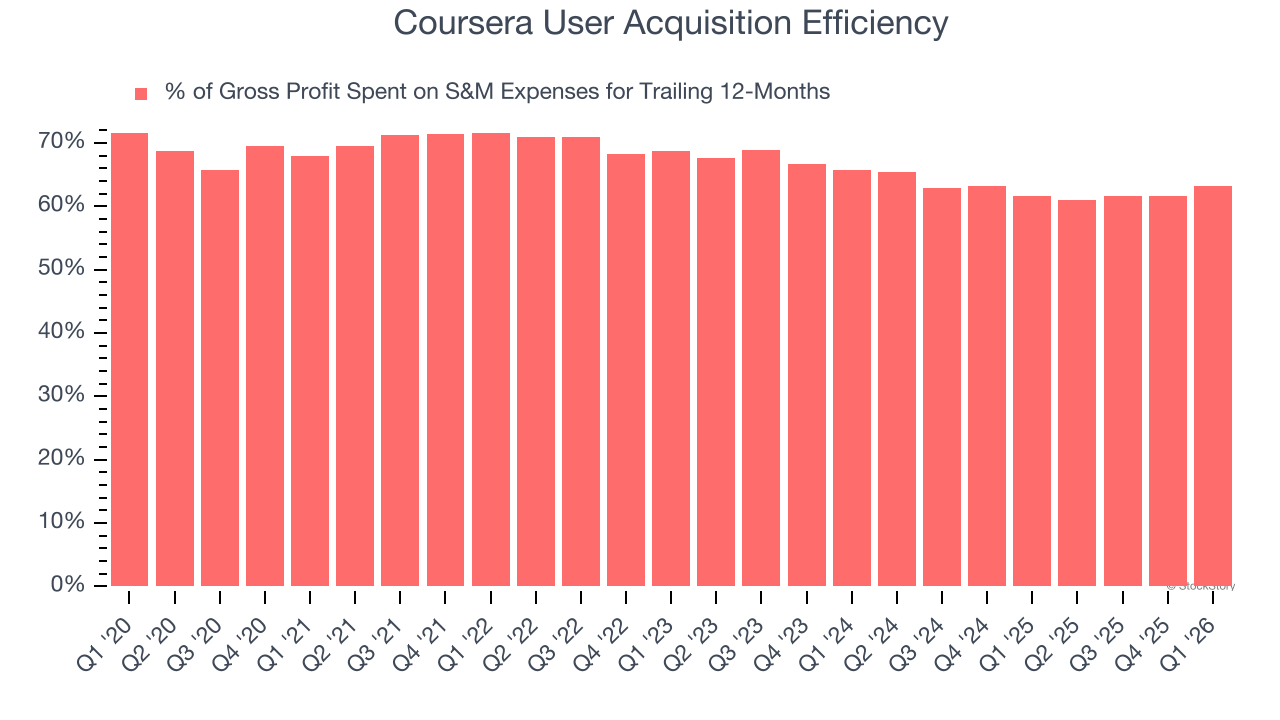

Poor Marketing Efficiency Drains Profits

Consumer internet businesses like Coursera grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

It’s very expensive for Coursera to acquire new users as the company has spent 63.1% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates a highly competitive environment with little differentiation between Coursera and its peers.

Final Judgment

Coursera’s positive characteristics outweigh the negatives. With the recent decline, the stock trades at 2.6× forward EV/EBITDA (or $5.90 per share). Is now the right time to buy? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.