Over the last six months, Pinterest’s shares have sunk to $21.95, producing a disappointing 18.9% loss - a stark contrast to the S&P 500’s 7.7% gain. This may have investors wondering how to approach the situation.

Following the pullback, is this a buying opportunity for PINS? Find out in our full research report, it’s free.

Why Is Pinterest a Good Business?

Created with the idea of virtually replacing paper catalogues, Pinterest (NYSE: PINS) is an online image and social discovery platform.

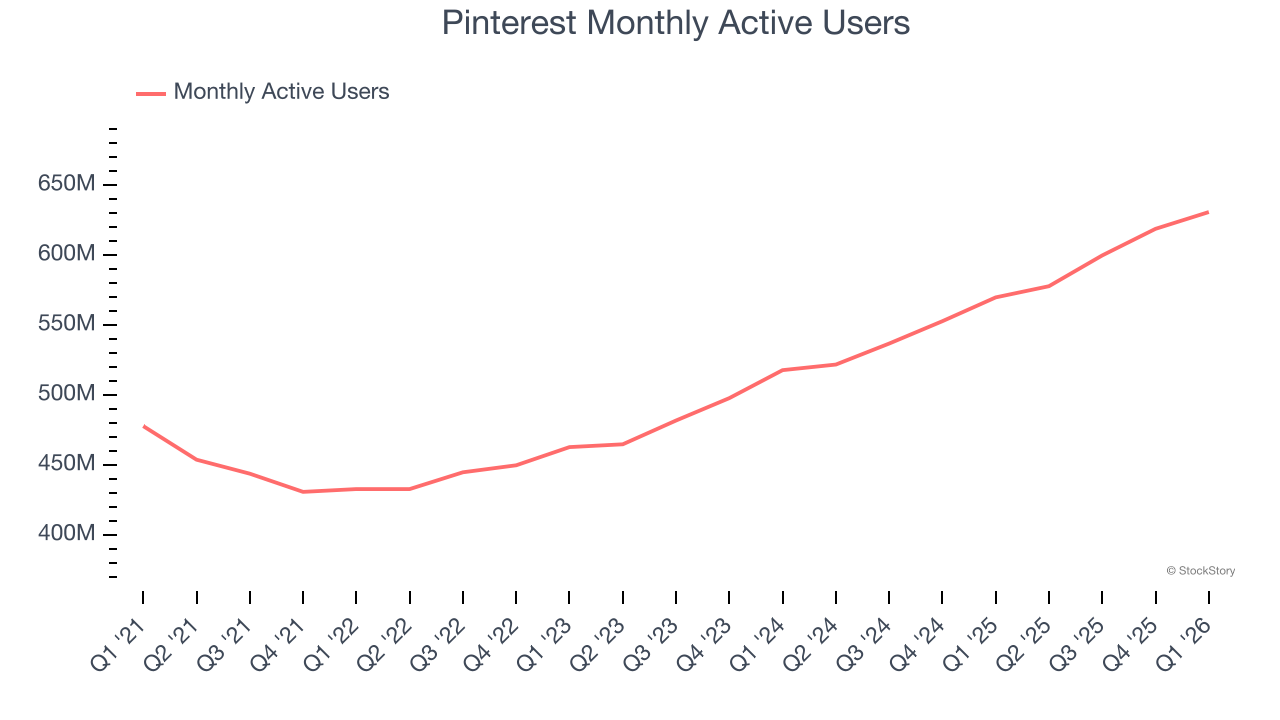

1. Monthly Active Users Skyrocket, Fueling Growth Opportunities

As a social network, Pinterest generates revenue growth by increasing its user base and charging advertisers more for the ads each user is shown.

Over the last two years, Pinterest’s monthly active users, a key performance metric for the company, increased by 11.2% annually to 631 million in the latest quarter. This growth rate is strong for a consumer internet business and indicates people love using its offerings.

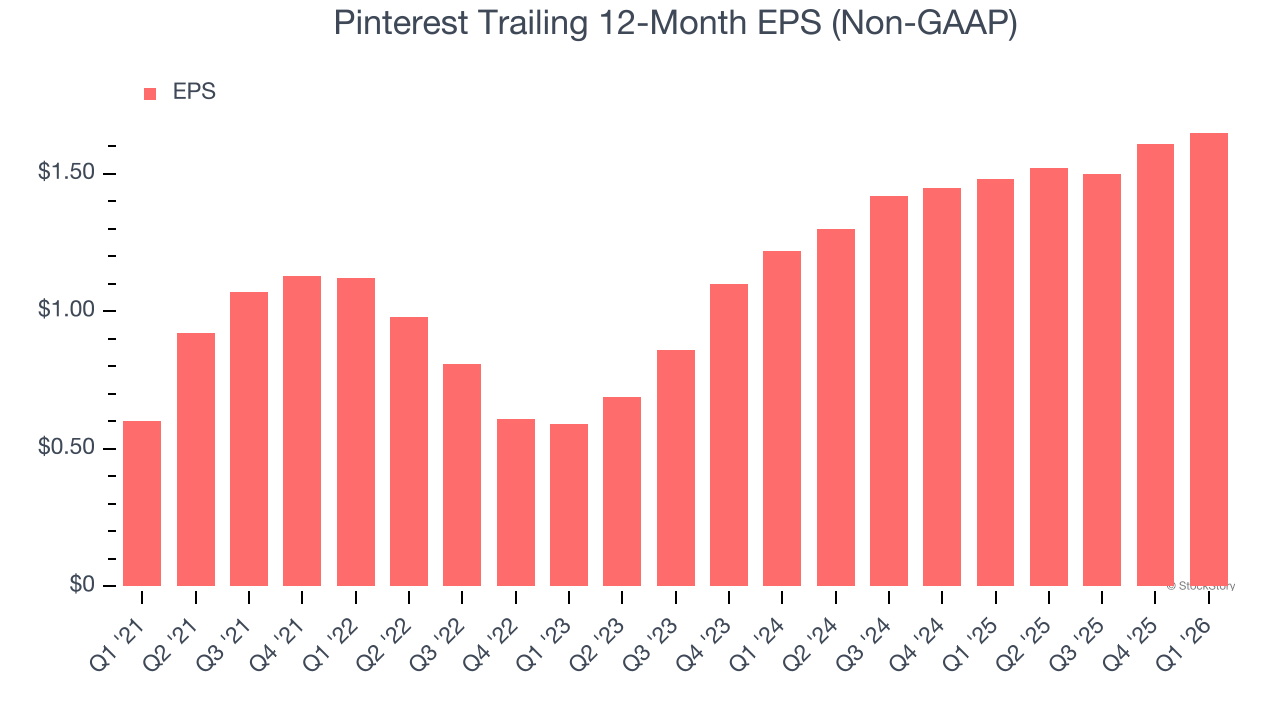

2. Outstanding Long-Term EPS Growth

Analyzing the long-term change in earnings per share (EPS) shows whether a company’s incremental sales were profitable — for example, revenue could be inflated through excessive spending on advertising and promotions.

Pinterest’s EPS grew at 40.9% compounded annual growth rate over the last three years, higher than its 15.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

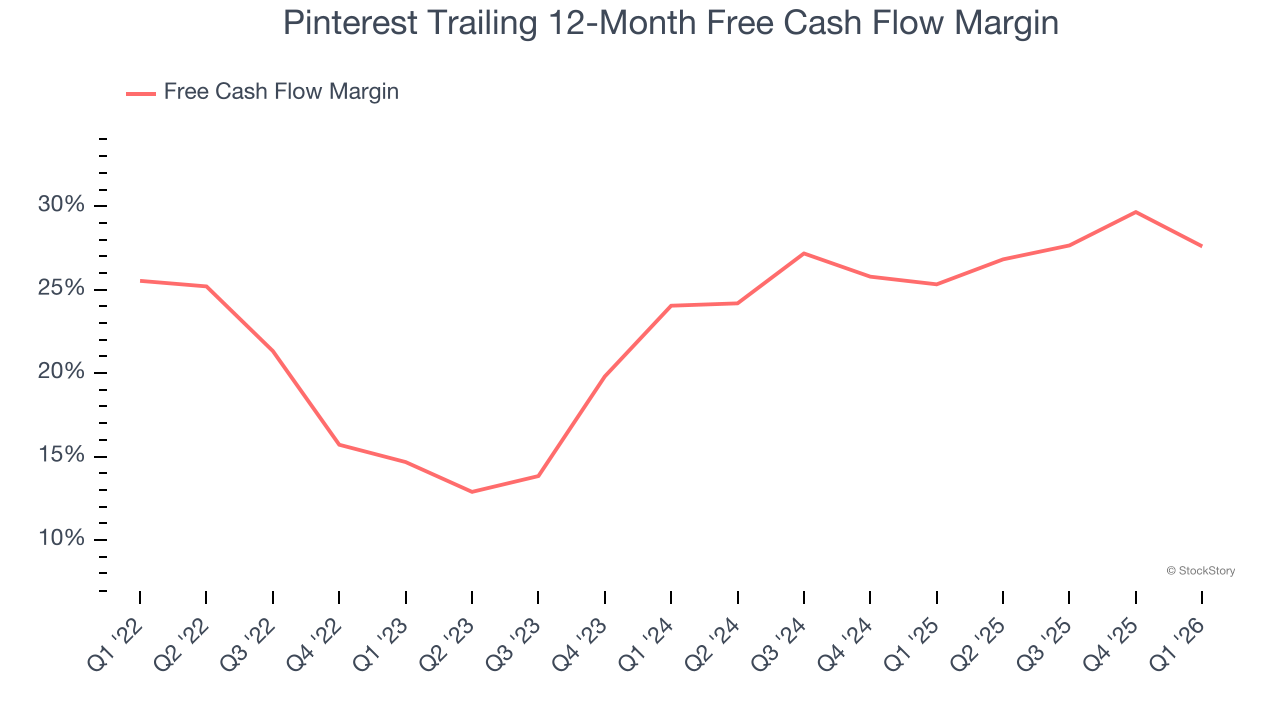

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Pinterest has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging 26.5% over the last two years.

Final Judgment

These are just a few reasons why we think Pinterest is a great business. After the recent drawdown, the stock trades at 9.7× forward EV/EBITDA (or $21.95 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Pinterest

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.