Shares of Southwest Airlines (NYSE: LUV) are trading lower in today's trading session, declining by as much as 6.5% following the company's first quarter of 2023 earnings announcement. While investors and markets are reacting negatively to the current figures and perhaps to some conservative management outlooks for the rest of the year, Southwest Airlines analyst ratings still hold the stock dear at a consensus price target of $47 per share. Implying a 61% upside from today's sell-off, investors will be well served by leaning into curiosity and finding out just why there is so much perceived value to be unlocked in this airline.

Some were Ready

Bob Jora, President and CEO of Southwest, stated in the press release for first quarter 2023 earnings, "As expected, we incurred a first-quarter 2023 net loss that resulted from the negative financial impact of approximately $380 million pre-tax, or $294 after-tax, related to the December 2022 operational disruption."

Southwest was faced, just like any other airline at the time, with severe weather conditions and spiking cancellation rates as a result, apart from financial damage, goodwill and reputational damage from upset customers who could not get to their holiday destinations in time added to the bearish sentiment in the stock price. Value investors know that this still needs to change the underlying business fundamentals, especially with the root of the problem being an industry-wide issue.

Unsurprisingly, the remaining quarter produced an annual revenue advance of 21.6%, or as the CEO expressed, "Our operational performance was also strong in the first quarter of 2023. Southwest ranked number two in domestic on-time performance year-to-date through March 2023." Adding to the optimism comes some fundamental bullish indicators in Southwest Airlines' financials.

The company's balance sheet will reflect that accounts receivable days outstanding are at a historically high level of 18.4 days, coming off from 2020's 45.6 days. This indicator means that the company still has a lot of revenue upside to be reflected in the second quarter, as accounts receivable are booked flights which will reflect as revenue once the flight service is delivered, in this case, within the next month. In addition, a typical ratio for Southwest stands below ten days, implying there is still potential for double-digit revenue growth for the next quarter.

The Real Results and Future Outlook

Management expressed in the press release that revenue figures were impacted by a non-recurring negative impact of approximately $325 million due to December's weather conditions. Despite unexpected service and network disruptions, Southwest achieved its upper-end guidance and a record quarterly revenue result. If investors are willing to be flexible in assumptions, adding back this $325 million non-recurring impact would have translated into over $6 billion in revenue, keeping everything else constant; such a top-line result would have yielded positive earnings per share of $0.28 rather than a $0.27 loss.

Despite the actual value of earnings being impacted by uncontrollable factors, management is still opting for the conservative route for 2023. Guidance suggests a revenue decline between 8-11% as they are currently experiencing delays on new Boeing (NYSE: BA) jet orders, hindering capacity and revenue generation. Regarding capacity utilization within the company, investors may spot another reason to consider buying this stock. Historically speaking, utilization has been above the 100% mark save for 2020, when the travel industry felt the impacts of COVID-19 lockdowns. The 2021 to 2023 period saw a recovery to a current 137% utilization rate, which may signal that the value reflected in the market price may be disconnected from reality.

Pinpointing Upside Potential

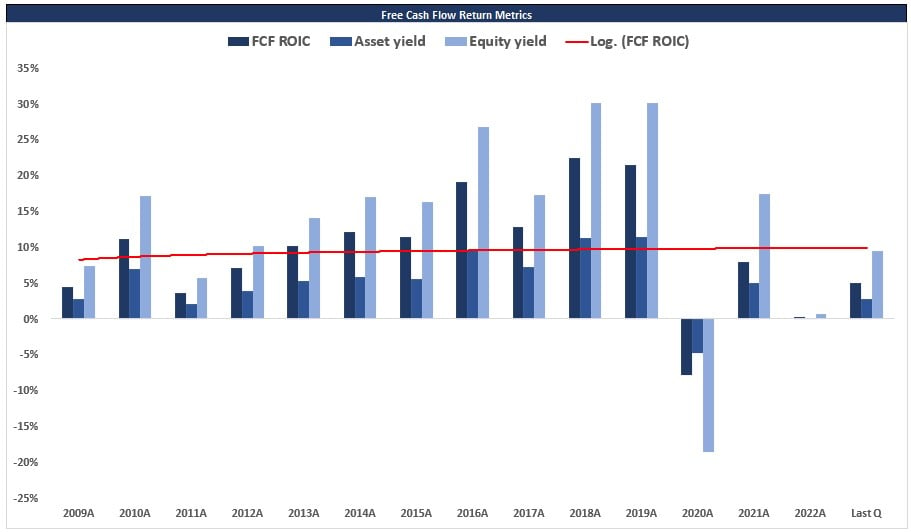

Taking free cash flow returns rather than net income, giving Southwest's profit cycle a more everyday scale, investors may notice that the business is performing at 2011-2012 levels. What followed after 2011-2011 was double-digit revenue growth rates, share buybacks, and a monster rally from $9 per share up to $47 two years later. History rhymes a lot of the time, and Southwest's business is as strong as ever. Can investors be in for another monster rally?

Regarding spotting a bottom, fundamentally, investors are facing a significant discount. Net asset value per share (NAV), computed as total assets minus total debt, is $44.25. Thus, investors can buy Southwest Airlines for a nearly 35% discount. Technically speaking, there is a strong support level within the $28-$30 per share, serving as a Fibonacci retracement ratio past the 'golden ratio' of 61-78% retracement. Fundamentally speaking, the company is performing as if it was still bringing in 2011's revenue of $15 billion; technically, it is trading back at 2020 prices as if the entire travel industry was shut down due to a pandemic. At some point, logic and real value have to kick in and bring Southwest to the valuation it deserves, thus keeping analysts safe in their jobs.