While the S&P 500 is up 16.8% since August 2024, Gap (currently trading at $22.90 per share) has lagged behind, posting a return of 10.9%. This might have investors contemplating their next move.

Is there a buying opportunity in Gap, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We're cautious about Gap. Here are three reasons why you should be careful with GAP and a stock we'd rather own.

Why Do We Think Gap Will Underperform?

Operating under the Gap, Old Navy, Banana Republic, and Athleta brands, Gap (NYSE: GAP) is an apparel and accessories retailer selling casual clothing to men, women, and children.

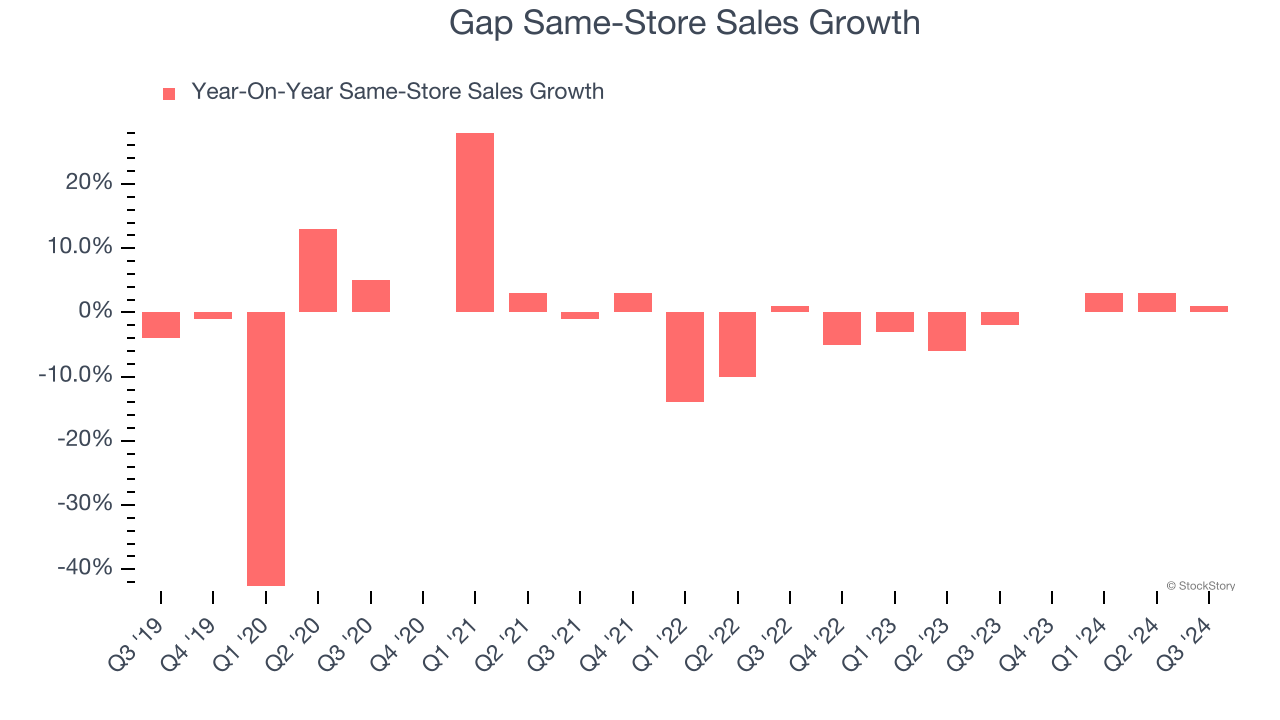

1. Shrinking Same-Store Sales Indicate Waning Demand

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Gap’s demand has been shrinking over the last two years as its same-store sales have averaged 1.1% annual declines.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Gap’s revenue to stall, close to its 1.4% annualized declines for the past five years. This projection doesn't excite us and indicates its newer products will not accelerate its top-line performance yet.

3. Previous Growth Initiatives Haven’t Paid Off Yet

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Gap historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 3%, lower than the typical cost of capital (how much it costs to raise money) for consumer retail companies.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of Gap, we’ll be cheering from the sidelines. With its shares underperforming the market lately, the stock trades at 12× forward price-to-earnings (or $22.90 per share). This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are more exciting stocks to buy at the moment. Let us point you toward the most dominant software business in the world.

Stocks We Like More Than Gap

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.