Over the past six months, Jackson Financial’s shares (currently trading at $87.98) have posted a disappointing 8.8% loss, well below the S&P 500’s 5.8% gain. This might have investors contemplating their next move.

Is now the time to buy Jackson Financial, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Jackson Financial Not Exciting?

Despite the more favorable entry price, we don't have much confidence in Jackson Financial. Here are three reasons why there are better opportunities than JXN and a stock we'd rather own.

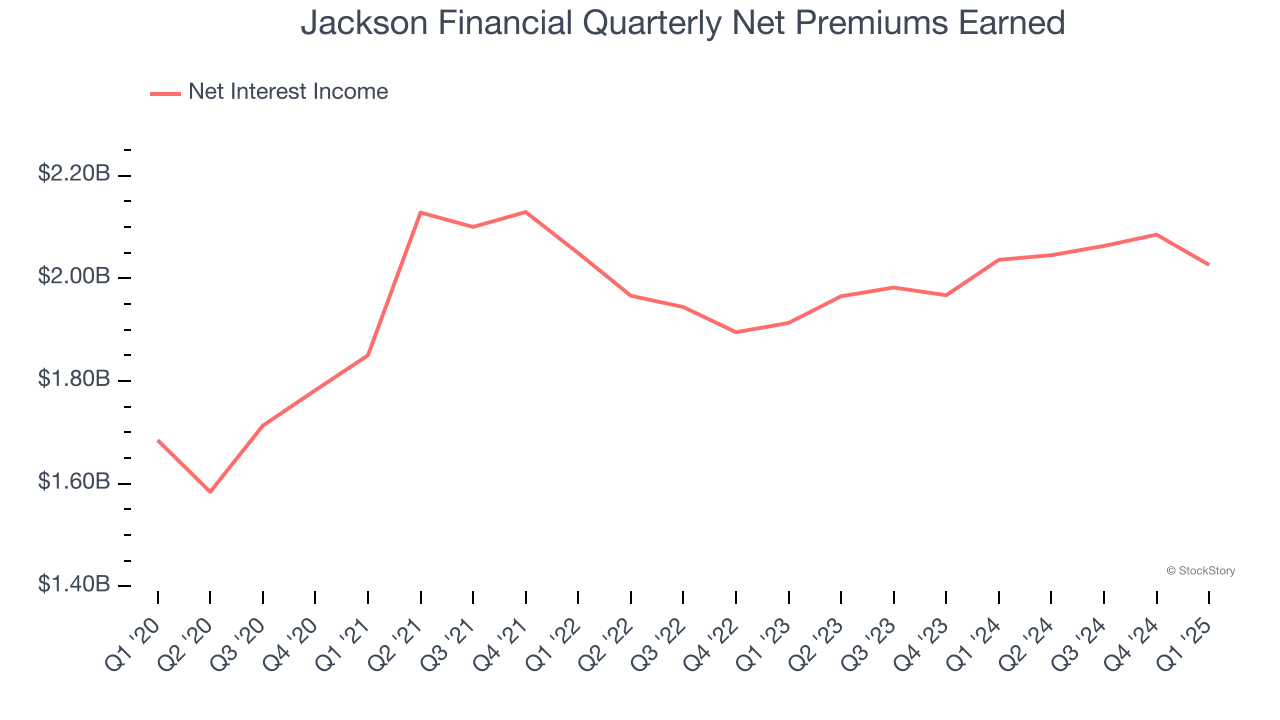

1. Net Premiums Earned Points to Soft Demand

Net premiums earned commands greater market attention due to its reliability and consistency, whereas investment and fee income are often seen as more volatile revenue streams that fluctuate with market conditions.

Jackson Financial’s net premiums earned has grown at a 3.2% annualized rate over the last two years, worse than the broader insurance industry and slower than its total revenue.

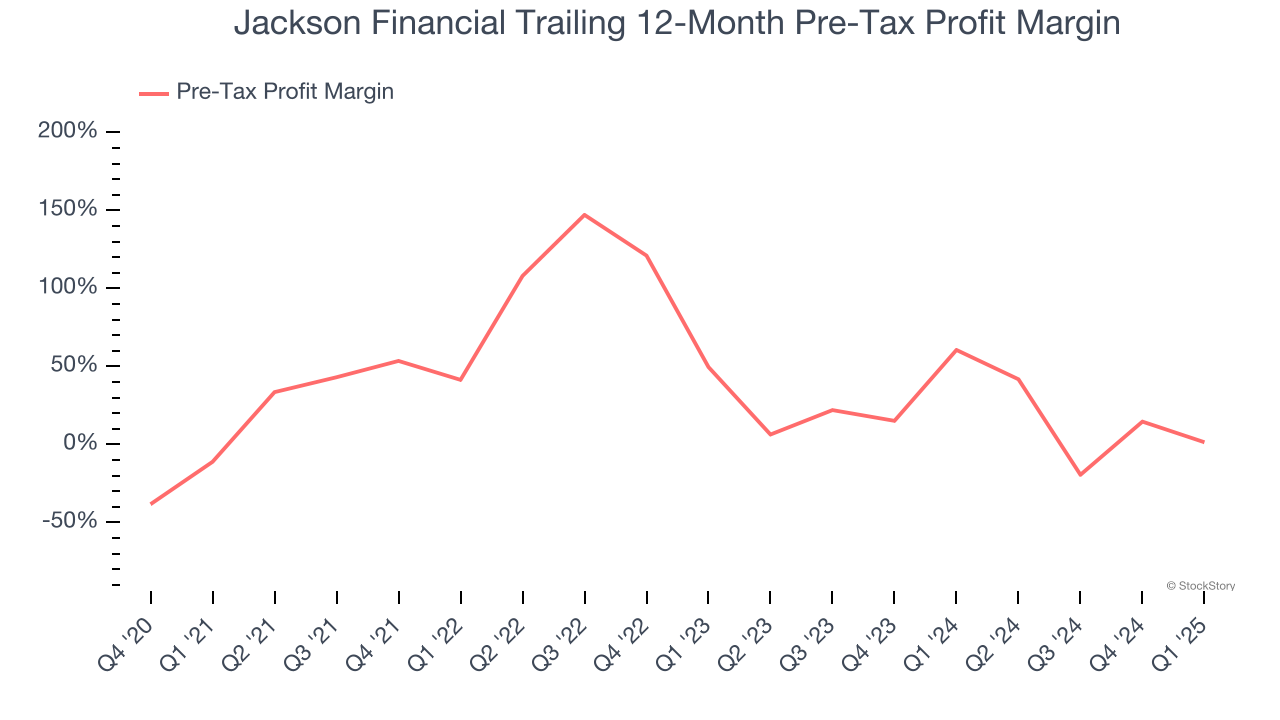

2. Deteriorating Pre-tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

This is because insurers are balance sheet businesses, where assets and liabilities define the core economics. This means that interest income and expense should be factored into the definition of profit but taxes - which are largely out of a company’s control - should not.

Over the last four years, Jackson Financial’s pre-tax profit margin has risen by 12.5 percentage points, clocking in at 1.4% for the past 12 months. Said differently, the company’s expenses have grown at a slower rate than revenue, which is always a positive sign.

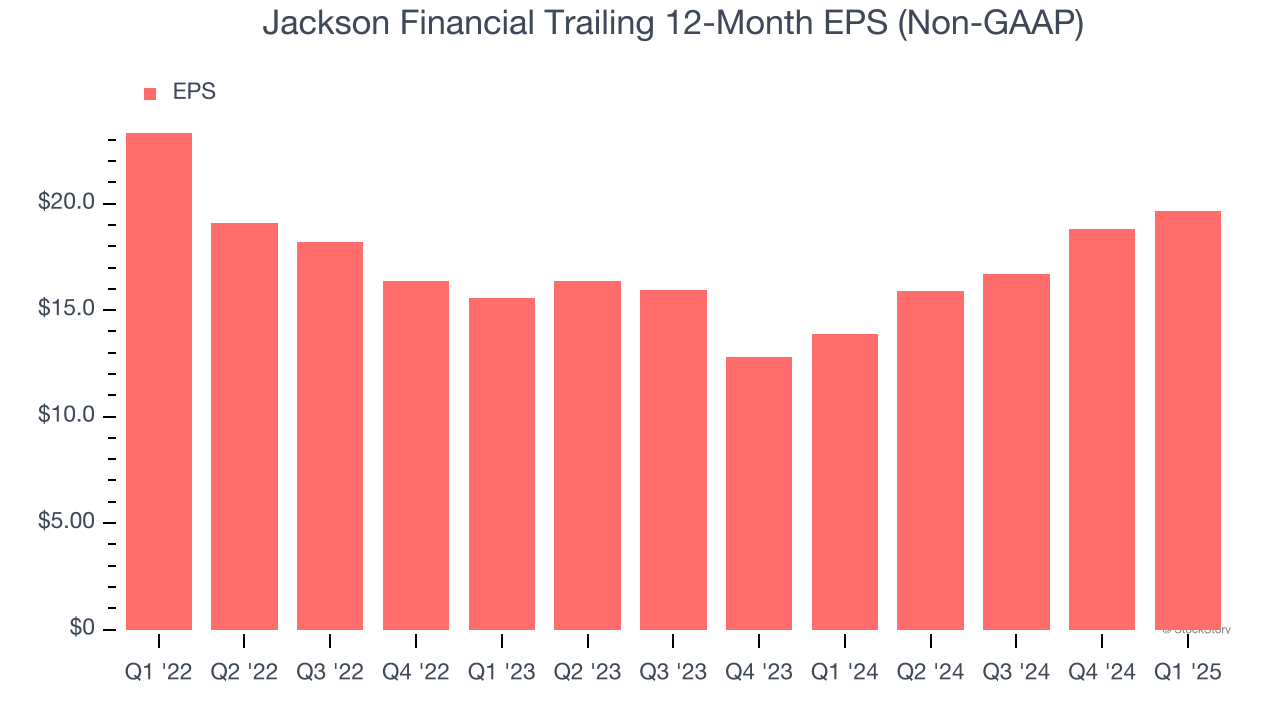

3. EPS Trending Down

We track the change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Jackson Financial’s full-year EPS dropped 18.7%, or 5.9% annually, over the last three years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Jackson Financial’s low margin of safety could leave its stock price susceptible to large downswings.

Final Judgment

Jackson Financial isn’t a terrible business, but it doesn’t pass our bar. Following the recent decline, the stock trades at 0.6× forward P/B (or $87.98 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Like More Than Jackson Financial

When Trump unveiled his aggressive tariff plan in April 2025, markets tanked as investors feared a full-blown trade war. But those who panicked and sold missed the subsequent rebound that’s already erased most losses.

Don’t let fear keep you from great opportunities and take a look at Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.