Adobe (ADBE) is about to step back into the spotlight. The San Jose, California-based software giant is set to report its fiscal first-quarter 2026 earnings on March 12. And after a strong finish to fiscal year 2025, investors have real reason to pay attention.

Wall Street is watching closely for clues about whether Adobe's artificial intelligence push is finally becoming a serious revenue engine.

What Analysts Expect From Adobe's Q1 Results

The consensus among analysts heading into March 12 is cautiously optimistic.

- According to estimates compiled by Yahoo Finance, analysts project first-quarter revenue of about $6.28 billion, up roughly 9.85% from the $5.71 billion that Adobe posted in the same period a year ago.

- On the earnings side, the average estimate calls for normalized earnings per share of $5.87, compared to $5.08 a year earlier, indicating a jump of more than 15%.

- That squares up well with Adobe's own guidance. The company told investors to expect Q1 revenue between $6.25 billion and $6.30 billion, along with non-GAAP EPS of $5.85 to $5.90.

In short, Adobe is setting a bar it believes it can clear.

For the full fiscal year 2026, analysts are modeling revenue of around $26.04 billion and EPS of $23.49. Adobe's own targets are $25.9 billion to $26.1 billion in revenue and $23.30 to $23.50 in non-GAAP EPS, putting the company and the Street largely in agreement.

Adobe's AI Momentum Is the Real Story

Adobe isn't just a creative software company anymore. Over the past two years, the company has aggressively transformed its products around AI.

At Adobe MAX in October 2025, the company unveiled expanded capabilities across Photoshop, Premiere, Illustrator, and its Firefly generative AI app, integrating more than 25 partner AI models from companies like Google, OpenAI, and Runway alongside Adobe's own Firefly models.

The payoff is starting to show up in the data.

Adobe CEO Shantanu Narayen pointed out during the company's Q4 fiscal 2025 earnings call in December that generative credit consumption, a key measure of how heavily users rely on AI features, grew threefold from the prior quarter.

Monthly active users across Adobe's freemium products, including Firefly, Express, and Premiere Mobile, surpassed 70 million, up more than 35% year-over-year (YoY).

"Q4 was an inflection in the early indicators, which we continue to track," Narayen said on the call.

Adobe also said that more than one-third of its total book of business now qualifies as AI-influenced, meaning customers are actively using or paying for AI-powered features. That's no small thing. Adobe ended fiscal 2025 with total annual recurring revenue of $25.66 billion, and the company is targeting over 10% growth in that figure for fiscal 2026.

Adobe's Expanding Ecosystem Adds New Growth Levers

Beyond the core Creative Cloud business, Adobe has been building out what it calls "customer experience orchestration" a suite of tools for marketers to create, manage, and measure content at scale.

Adobe Experience Platform and its AI agents now process over 70 billion profile activations per day, according to the company. Subscription revenue for those apps grew by more than 40% YoY in fiscal 2025.

Adobe also announced in November 2025 its intent to acquire Semrush Holdings for approximately $1.9 billion in cash.

- The deal, expected to close in the first half of fiscal 2026 pending regulatory approval, would give Adobe a stronger foothold in search engine optimization and brand visibility tools.

- These verticals should gain massive traction as AI-powered search engines reshape how consumers discover brands.

It's worth noting that Adobe's fiscal 2026 financial targets do not include any contribution from Semrush. That means if the deal closes on schedule, it could provide upside to full-year results.

What to Watch on March 12

When Adobe reports on March 12, here are the three things worth paying close attention to:

- First, watch generative credit consumption. The three-times quarter-over-quarter jump in Q4 was a headline number. Investors will want to see whether that momentum carried into Q1 or if it was a one-time spike.

- Second, watch Digital Media's annual recurring revenue. Adobe exited fiscal 2025 with $19.2 billion in Digital Media ARR. Any sign of re-acceleration there would likely be well-received.

- Third, watch for any updates on the Semrush acquisition timeline. If Adobe signals a faster-than-expected close, that could boost investor confidence in the fiscal 2026 revenue outlook.

Adobe has spent years building the infrastructure for an AI-driven content economy. March 12 may be the next moment investors find out just how far along that journey has come.

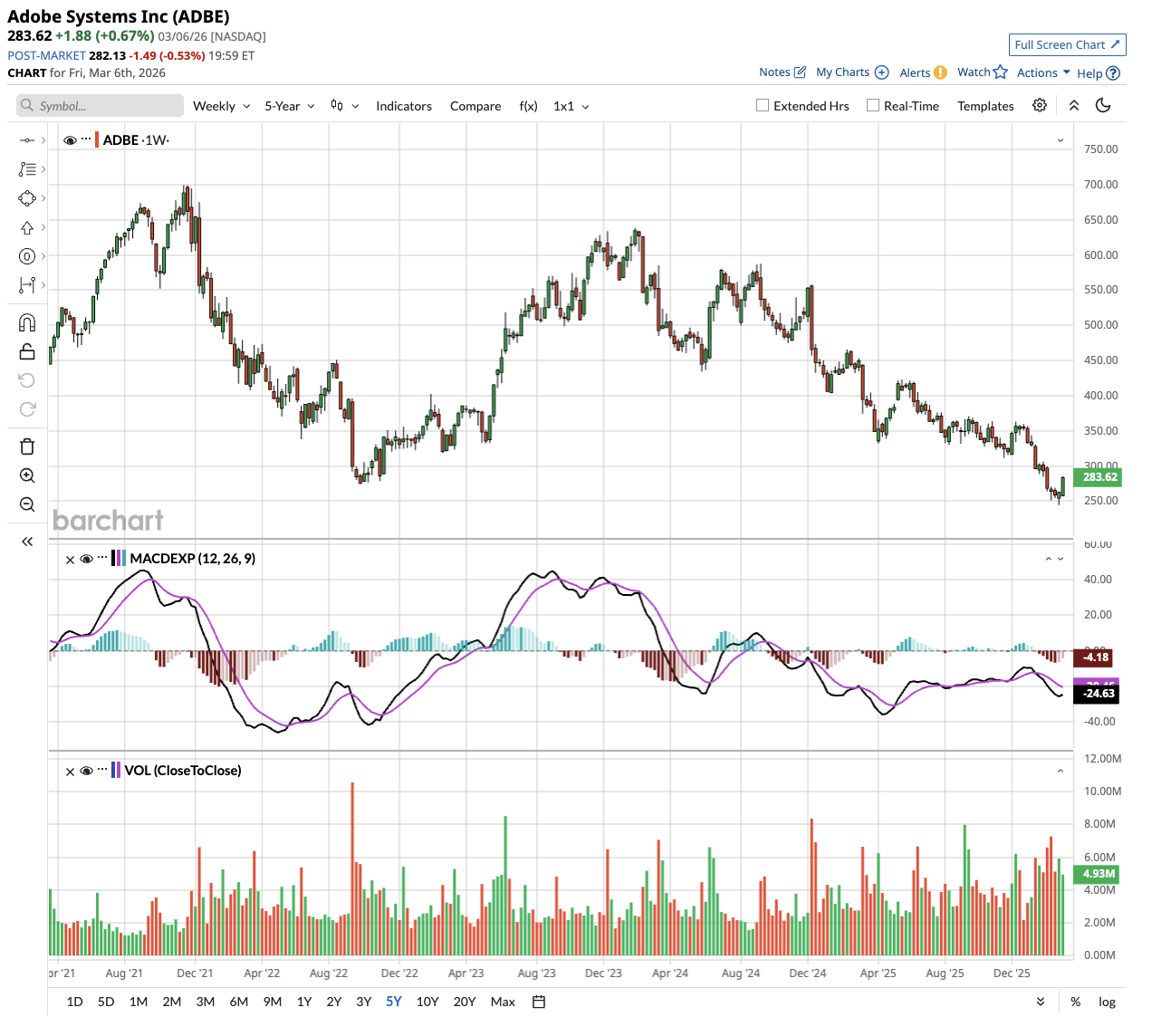

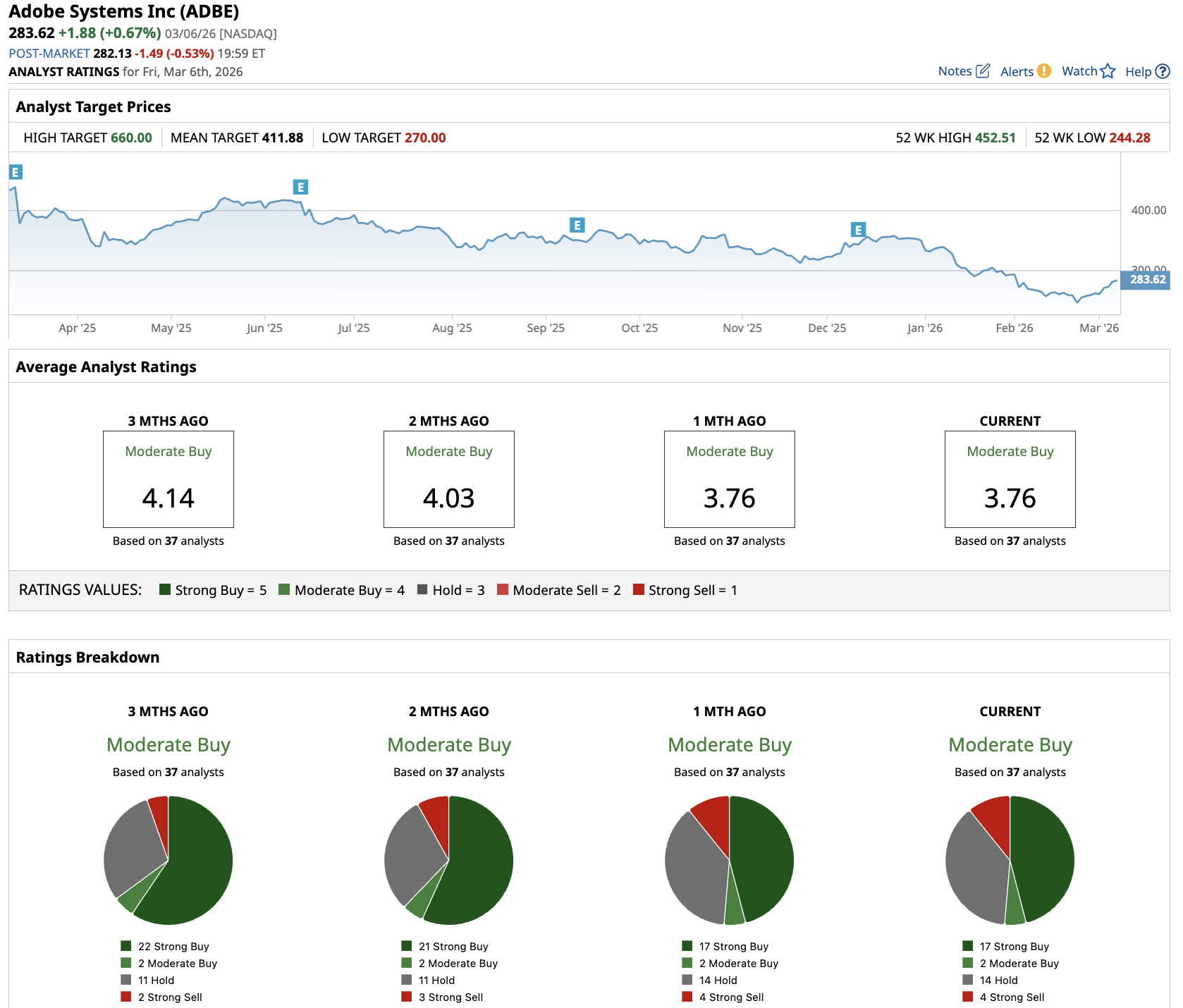

Valued at a market cap of $115 billion, ADBE stock is down 59% from its all-time highs and has underperformed the broader markets over the past five years. Out of the 37 analysts covering ADBE stock, 17 recommend “Strong Buy,” two recommend “Moderate Buy,” 14 recommend “Hold,” and four recommend “Strong Sell.” The average ADBE stock price target is $411.88, above the current price of about $284.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart