After staging a remarkable rebound this year from its earlier lows, Intel Corporation (INTC) is once again in the spotlight this week. According to a recent Wall Street Journal report, iPhone maker Apple (AAPL) has reached a preliminary agreement with Intel to manufacture chips for future Apple devices. The report, citing people familiar with the matter, said the two companies spent more than a year in intensive discussions before formalizing a deal in recent months. Of course, investors cheered the development, sending Intel shares soaring nearly 14% higher on May 8.

And Wall Street’s optimism has only grown louder since then. Following the report, Lynx Equity issued a new Street-high price target on Intel, saying the Apple partnership “adds more fire to a stock that has already been on fire this year.” The analyst reiterated a preference for Intel over Advanced Micro Devices (AMD) and raised the price target to $175, arguing that the involvement of two major industry leaders should ease investor concerns about the long-term sustainability of Intel Foundry Service (IFS).

So, given the wave of bullish sentiment now surrounding the stock, here’s a closer look at the chip giant’s remarkable turnaround story.

About Intel Stock

Founded in 1968 and headquartered in Santa Clara, Intel Corporation has long been one of the most influential names in the global semiconductor industry. Best known for designing and manufacturing the processors that power millions of personal computers and data centers worldwide, Intel has evolved far beyond its PC roots in recent years. The company now operates across several key segments, including client computing, data center and artificial intelligence (AI) chips, networking and edge computing, and Intel Foundry Services, its rapidly expanding contract chip manufacturing business.

As demand for AI and advanced computing continues to reshape the tech landscape, Intel is working to reinvent itself as both a leading chip designer and a major global semiconductor manufacturer. Yet not long ago, Intel looked like a fallen giant with little hope of reclaiming its former dominance. As fabless chipmakers such as Nvidia (NVDA) and AMD raced ahead in the AI boom, Intel was steadily losing market share and struggling to keep up.

The once-dominant semiconductor leader had become a slow-growth company weighed down by declining earnings, shrinking margins, and fading investor confidence. Things became so difficult that Intel cut its dividend in 2023 before suspending it entirely in 2024. Shares continued to bleed, billions in market value evaporated, and many investors believed the company had completely missed the biggest technology shift of the decade. Fast forward to 2026, and Intel’s turnaround has been nothing short of stunning.

The chip giant has delivered a massive triple-digit recovery over the past year, forcing skeptics to rethink the company’s future. Aggressive cost-cutting measures, large-scale restructuring, new leadership, expanding IFS and a series of high-profile partnerships have dramatically changed the narrative. The turnaround gained even more credibility after the U.S. federal government took nearly a 10% stake in the company last year, reinforcing confidence in Intel’s strategic importance and long-term potential.

Backed by surging investor confidence and growing strategic support, Intel has rapidly transformed from one of the market’s biggest laggards into one of its hottest comeback stories. The chip giant is gaining momentum through advances in AI-focused technologies and next-generation semiconductor manufacturing, and investors have taken notice in a big way.

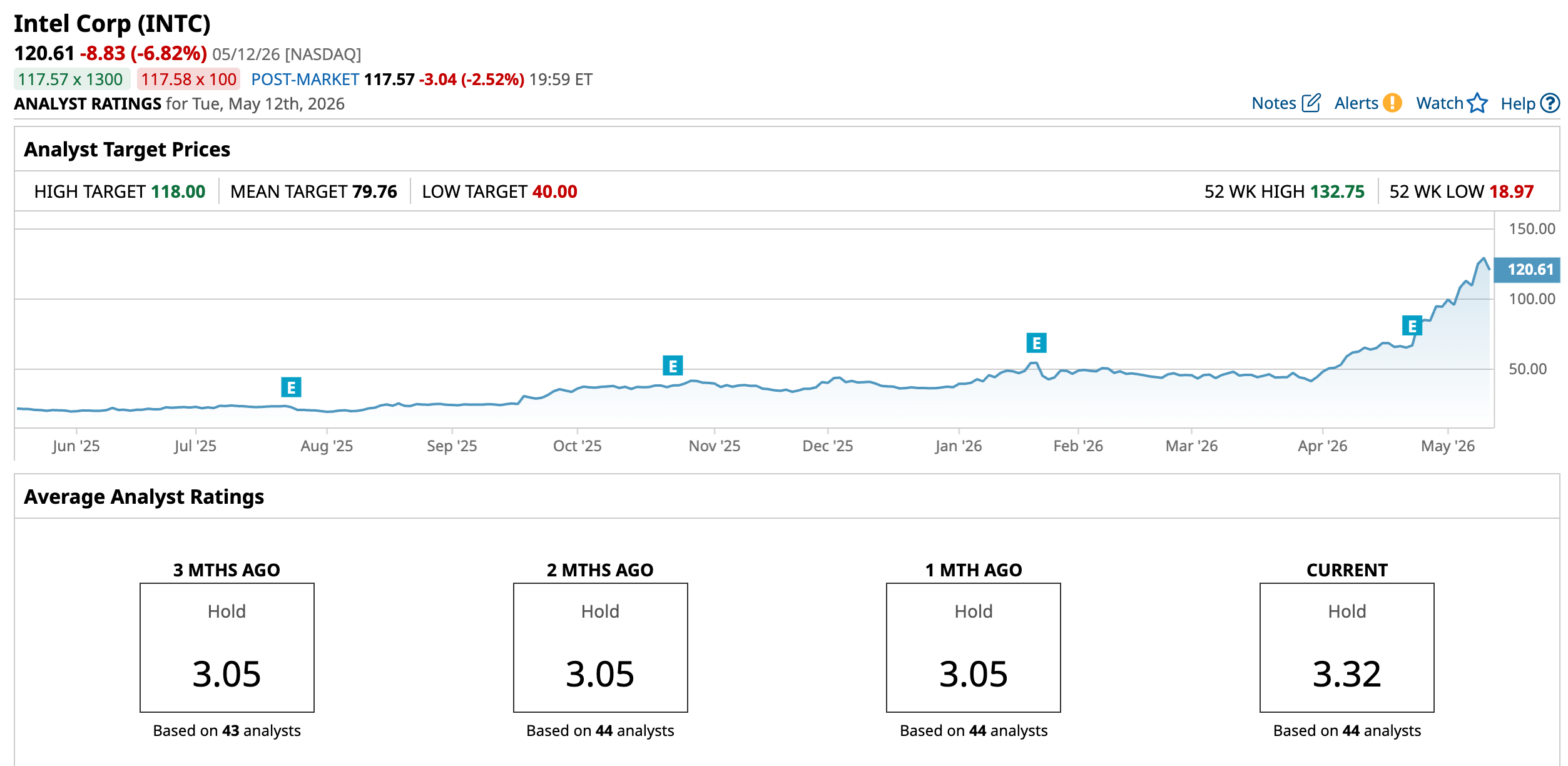

Now valued at roughly $650.57 billion by market capitalization, Intel shares have delivered a jaw-dropping 443.78% return over the past year, crushing the broader S&P 500 Index ($SPX), which climbed 26.24% over the same stretch. The rally has remained explosive so far in 2026, with the stock soaring 226.86% year-to-date (YTD) compared to the broader market’s far smaller 8.11% gain. The momentum recently drove Intel shares to a new 52-week high of $132.75 on May 11, and the stock remains firmly near those levels, slipping only 9.15% from its recent peak.

Inside Intel’s Q1 Earnings Report

Intel’s improving financial performance is adding real substance to its comeback story. On April 23, the chip giant delivered a surprisingly strong fiscal 2026 first-quarter earnings report that topped Wall Street expectations across nearly every major metric, sparking a massive 23.6% rally in the stock the very next trading session. Revenue, gross margin, and earnings per share all came in above the high end of management’s guidance, marking Intel’s sixth consecutive quarter of outperforming its own financial expectations.

Intel reported non-GAAP revenue of $13.58 billion, up 7% year-over-year (YOY) and comfortably ahead of analysts’ consensus estimate of $12.39 billion. However, the biggest surprise came from the bottom line. The company posted non-GAAP earnings of $0.29 per share, crushing expectations of just $0.01 per share. The huge earnings beat was largely driven by aggressive cost-cutting efforts and a more profitable, high-margin product mix.

Even so, the turnaround is still very much a work in progress. On a GAAP basis, Intel reported a net loss of $3.7 billion, primarily due to one-time charges tied to goodwill impairment and ongoing restructuring expenses. One of the strongest areas of growth came from Intel’s data center business, where the company is beginning to gain traction in AI-related workloads amid rising demand for central processing units (CPUs). Revenue in the segment jumped 22% YOY to $5.1 billion.

Meanwhile, the Client Computing Group (CCG), which houses Intel’s PC chip business, generated $7.7 billion in revenue, representing a modest 1% increase from the prior year. Intel’s ambitious foundry business also showed encouraging momentum. Revenue at Intel Foundry climbed 16% to $5.4 billion, reflecting growing interest in the company’s manufacturing capabilities.

The segment’s operating loss narrowed slightly to $2.4 billion, improving by $72 million sequentially as stronger yields across Intel 4, Intel 3, and Intel 18A helped boost gross margins. That improvement was partially offset by higher operating expenses tied to a deliberate increase in investments for Intel 14A, aimed at supporting evaluations from both internal teams and external customers.

Looking ahead, Intel struck an optimistic tone for the second quarter. The company projected revenue between $13.8 billion and $14.8 billion, comfortably above prior Wall Street expectations. Intel also expects a non-GAAP gross margin of roughly 39% as it continues balancing the heavy costs of expanding manufacturing capacity with the profitable ramp-up of its next-generation AI and consumer chips.

How Are Analysts Viewing Intel Stock?

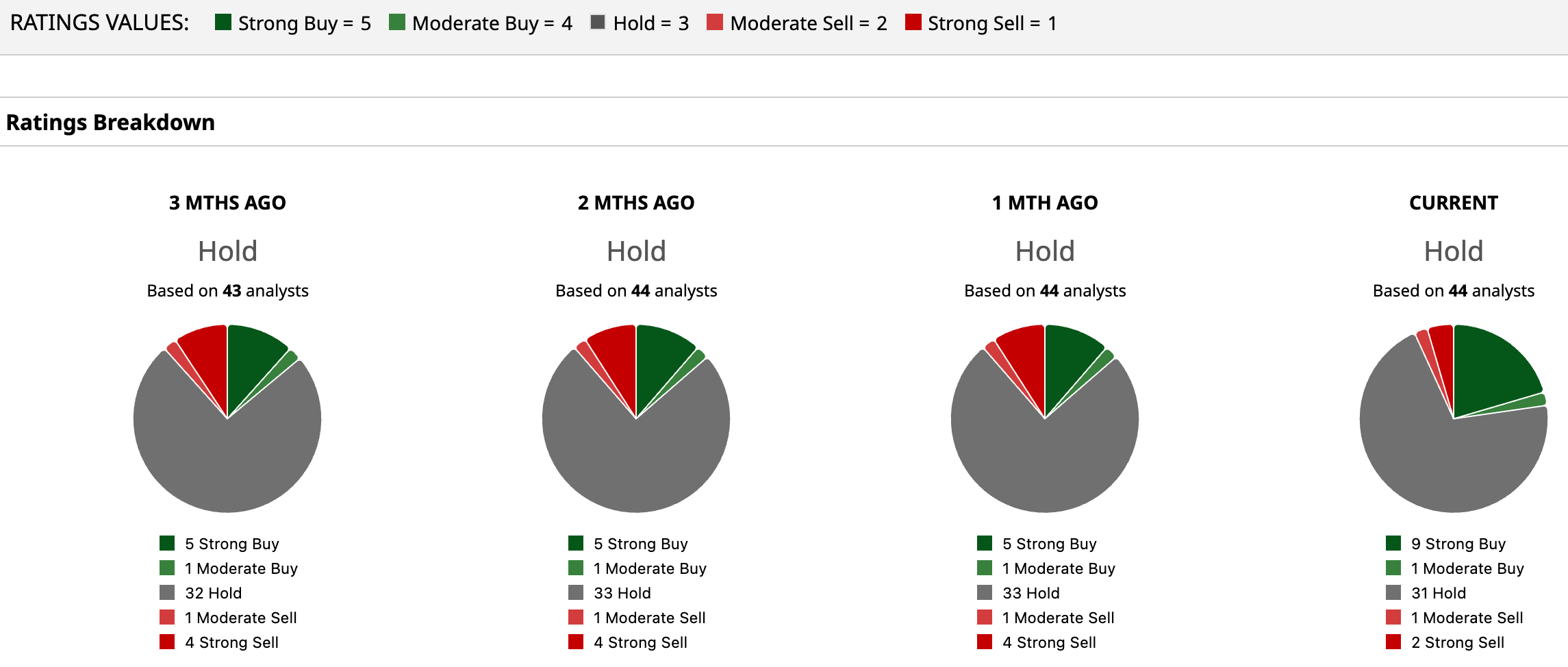

Even after Intel’s stunning turnaround and explosive rally, Wall Street has yet to fully embrace the comeback story. The stock currently carries a consensus “Hold” rating, reflecting a market that is increasingly impressed by Intel’s progress but still cautious about whether the momentum can be sustained over the long term. Out of 44 analysts covering the chip giant, nine rate the stock a “Strong Buy,” while one has assigned a “Moderate Buy” rating. However, the vast majority of 31 analysts remain on the sidelines with “Hold” recommendations. Meanwhile, one analyst rates the stock “Moderate Sell,” and only two remain firmly bearish with “Strong Sell” ratings.

Intel shares have already surged far beyond the average analyst price target of $79.76, highlighting the dramatic shift in sentiment for the company in recent months. However, Lynx Equity’s Street-high price target of $175 implies that Intel stock could still climb another 45% from current levels, underscoring growing confidence that the company’s foundry and AI ambitions may finally be gaining real traction.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Lululemon Stock Just Hit Another 52-Week Low. History Tells Us It Could Lose Another $25 from Here.

- The DRAM ETF’s Record Success Warns of a Dot-Com Bubble Burst. We’re Just Waiting for the Explosion.

- NVDA Stock Watch: What to Expect as Jensen Huang Joins Trump-Xi Summit

- Plug Power Stock Climbed 96% YTD and Hit New Highs After a Solid Q1 Beat. The Turnaround Might Be Finally Sticking.