From Nvidia (NVDA) and Advanced Micro Devices (AMD) to Apple (AAPL) and Broadcom (AVGO), most of the world’s tech titans rely on one company to manufacture their advanced chips. As the world’s largest semiconductor foundry, Taiwan Semiconductor Manufacturing Company (TSM) manufactures the most cutting-edge chips. This dominant position has made TSMC the backbone of the global semiconductor industry and one of the most important suppliers fueling the AI revolution. TSM stock has surged 33.8% year-to-date, outperforming the broader market gain of 8.4%.

For investors who want their $500 put to work, TSMC may be one of the smartest long-term AI investments now.

TSMC Has a Competitive Advantage Few Can Match

TSMC's ability to manufacture advanced chips at scale makes it an indispensable partner for the biggest names in tech. Its advanced process technologies, particularly the 3-nanometer and upcoming 2-nanometer nodes, are considered among the most sophisticated semiconductor manufacturing capabilities in the industry. AI accelerators, GPUs, high-performance CPUs, and data-centers all require this level of advanced tech.

In its most recent first quarter, TSMC’s revenue surged 40.6% year-over-year (YoY) to $35.9 billion, led by strong demand for its leading-edge process technologies. Its high-performance computing (HPC) segment’s revenue surged 20% sequentially, and accounted for 61% of total first-quarter revenue. The HPC segment includes AI accelerators, data center chips, and advanced processors that power the generative AI revolution.

TSMC’s technology leadership remains one of its biggest competitive advantages. Its 3-nanometer chips contributed 25% of wafer revenue, while 5-nanometer chips accounted for 36% and 7-nanometer represented 13%. Advanced technologies, including 7-nanometer and more advanced nodes, accounted for 74% of TSMC’s total wafer revenue. Management believes its upcoming N2 family, along with enhanced variants like N2P and A16, could become another “large and long-lasting node” for the company. Its future A14 technology is also progressing on schedule.

TSMC is dramatically expanding global manufacturing capacity to meet a multi-year AI demand pipeline. It expects 2026 capital expenditure to be around $56 billion. It is adding new fabs in Tainan Science Park, Arizona, and Japan. Despite spending aggressively on expansion, TSMC’s ability to generate enormous profit is commendable. Earnings per share increased by 58.3% YoY in the quarter, with gross margin landing at 66.2%.

For the second quarter, TSMC expects gross margin between 65.5% and 67.5%, while revenue potentially increasing by 32% YoY at the mid-point to range between $39 billion and $40.2 billion. Management emphasized that the AI demand remains “extremely robust” as the industry transitions from generative AI toward agentic AI systems, increasing the requirement for advanced semiconductors. That said, management also pointed out some short-term headwinds such as higher component prices and macroeconomic uncertainty in consumer-focused end markets

Why TSMC Could Be One of the Smartest AI Investments

Building advanced fabrication plants involves huge investments and decades of research and engineering expertise. TSMC has spent years building its reputation that competitors like Intel (INTC) and Samsung (SMSN.L.EB) now struggle to match. As AI models become larger and more complex, demand for high-end semiconductor production may keep rising for years. TSMC’s long-term relevance in the semiconductor industry remains untouched for now. This competitive moat makes TSMC a very powerful long-term AI investment.

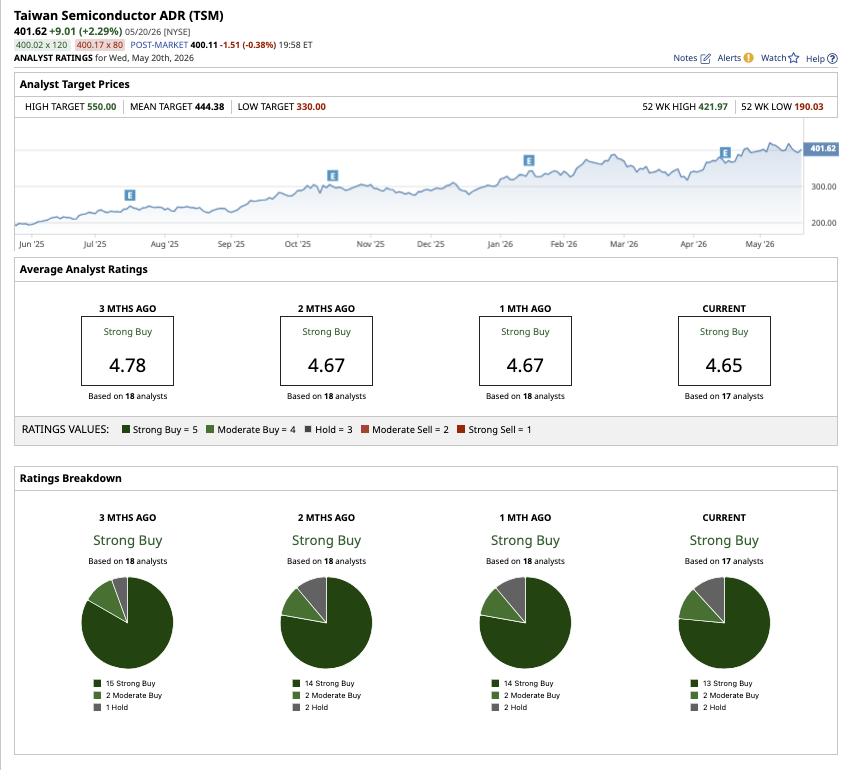

On Wall Street, the stock hold a consensus “Strong Buy” rating. Out of the 17 analysts that cover the stock, 13 rate it a “Strong Buy,” two say it is a “Moderate Buy,” and two rate it a “Hold.” Based on the average price target of $444.38, the stock has an upside potential of 11% from current levels. Plus, its high target price of $550 implies a potential upside of 37% over the next 12 months.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart