Buy now and pay later (BNPL) online purchase financing platform Affirm (NASDAQ: AFRM) is trying to maintain a foothold in a mudslide. The BNPL leader is facing a complete consumer paradigm shift as rising inflation hurts spending and a recession raises default risk. Consumer spending is getting toppled by inflation and its being felt across the board from retailers including Target (NYSE: TGT), Walmart (NYSE: WMT), and Best Buy (NYSE: BBY). Affirm is partnered with many of these big brands and relies heavily on some of its largest e-commerce partners like Amazon (NASDAQ: AMZN), Peloton (NASDAQ: PTON), and Shopify (NASDAQ: SHOP. It also faces stiff competition with other BNPL players including Afterpay (NASDAQ: SQ) and PayPal (NASDAQ: PYPL). With shares down (-76%) on the year, our hero has been all but left for dead. Shares have not been able to get one spur out of the grave as threats surround it from all fronts. It’s like a spaghetti western and Affirm is the (beaten down) underdog about to get ambushed (again). Cue the music.

Buy now and pay later (BNPL) online purchase financing platform Affirm (NASDAQ: AFRM) is trying to maintain a foothold in a mudslide. The BNPL leader is facing a complete consumer paradigm shift as rising inflation hurts spending and a recession raises default risk. Consumer spending is getting toppled by inflation and its being felt across the board from retailers including Target (NYSE: TGT), Walmart (NYSE: WMT), and Best Buy (NYSE: BBY). Affirm is partnered with many of these big brands and relies heavily on some of its largest e-commerce partners like Amazon (NASDAQ: AMZN), Peloton (NASDAQ: PTON), and Shopify (NASDAQ: SHOP. It also faces stiff competition with other BNPL players including Afterpay (NASDAQ: SQ) and PayPal (NASDAQ: PYPL). With shares down (-76%) on the year, our hero has been all but left for dead. Shares have not been able to get one spur out of the grave as threats surround it from all fronts. It’s like a spaghetti western and Affirm is the (beaten down) underdog about to get ambushed (again). Cue the music.The Good

Affirm posted strong growth in its fiscal Q4 2022 earnings report. Revenues grew 39% year-over-year (YoY) to $364.1 million to beat $354.88 million consensus analyst estimates. The general merchandise value (GMV) rose 77% YoY to $4.4 billion. GMV for the fiscal full-year 2022 rose 87% to $15.5 billion. The Company added 29,000 more active merchants most through Shopify’s Shop Pay Installments adoption. This brings total active merchants to 235,000 in Afterpay’s network. Active customers grew 96% YoY to 14 million and rose 10% or 1.2 million sequentially. While consumer discretionary spending takes a hit in a recession, the option to spread out payments becomes more appealing to customers.

The Bad

Affirm still lost (-$0.65) per share in Q4 2022. Even though it’s selling more, it’s losing more money in the process as adjusted operating margins were (-8%), down from being up 5.4% in the year ago Q4 2021 period. The challenge faced by Affirm is the impact of rising inflation on consumer spending as higher prices met by flat wages result in less spending on discretionary purchases. Rising interest rates may be good for Affirm as a financier, but it generally hurts consumers as debt and mortgage payments rise. This also cuts into discretionary spending.

The (Downright) Ugly

Affirm slashed its fiscal Q1 2023 guidance expecting revenues to come in between $345 million to $385 million versus $390 million consensus analyst estimates. GMV is expected between $4.2 billion to $4.6 billion. It expects adjusted operating margin to drop further to the (-12%) to (-14%) range. It further slashed its fiscal full-year 2023 guidance with revenues expected between $1.625 billion to $1.725 billion versus $1.9 billion consensus analyst estimates. GMV is expected between $20.5 billion to $22 billion. Adjusted operating margin is expected to be (-6.5%) to (-4.5%). A recession increases default risk as lenders tighten borrowing restrictions. BNPL customers mostly tend to range from the 18 to 24 Gen-Z and 35 to 44 Millennial demographic. The latter group also tends to have the highest consumer default risk, while the younger group is new to credit. Default risk starts to rise from 25 years to peak around 44 years and starts to fall off after 45 years of age.

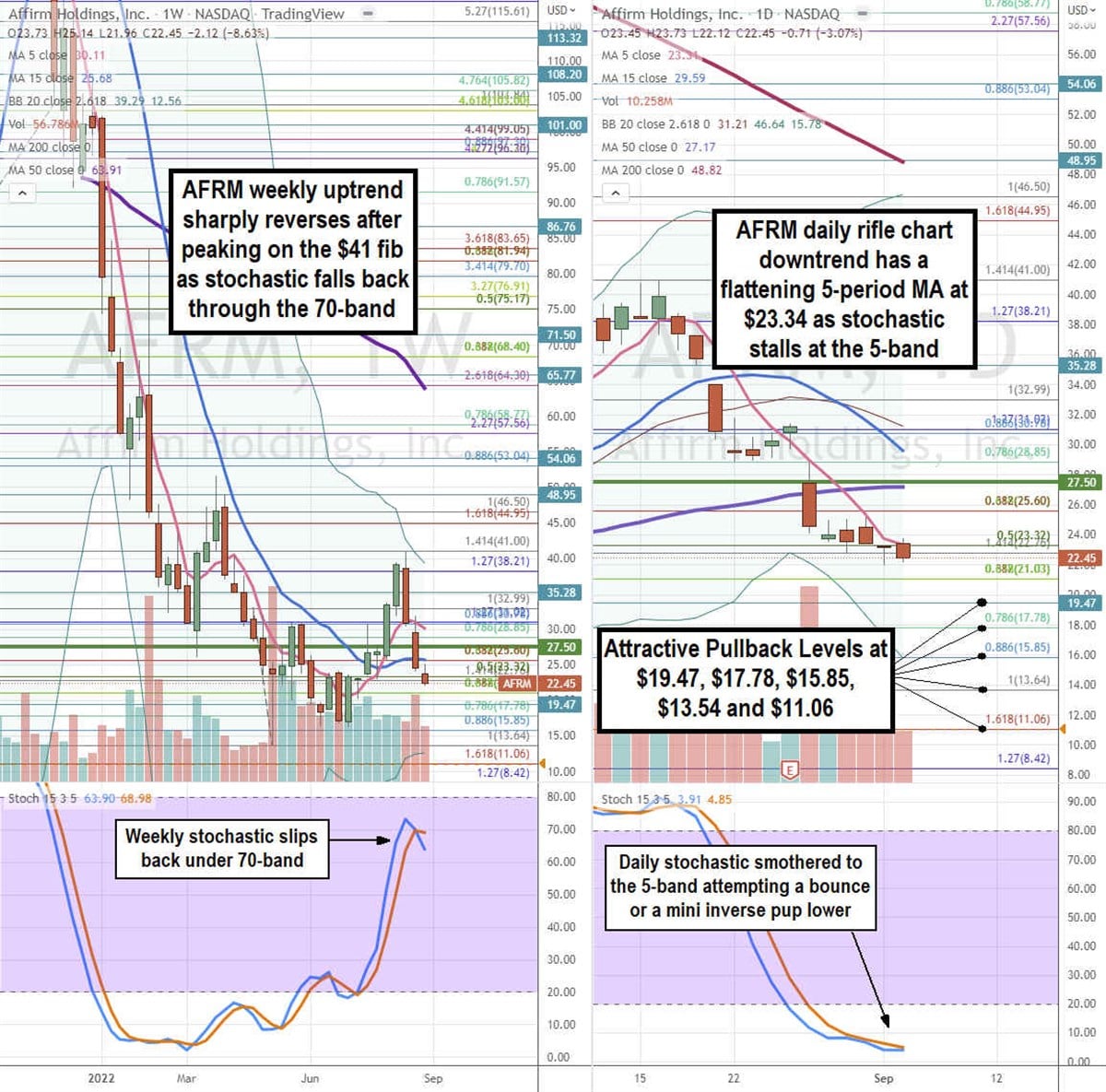

Here’s What the Chart Says

Using the rifle charts on the weekly and daily time frames provides a mid-term interpretation of AFRM’s stock price. AFRM peaked right at the $41 Fibonacci (fib) level on the most recent rally to sharply collapse on the reversal. Shares fell through the weekly 5-period moving average (MA) support at $30.11 and through the 15-period MA support at $25.68. The stochastic reversed sharply back under the 70-band as it fell through the weekly market structure low (MSL) buy trigger at $27.50. The weekly lower Bollinger Bands (BBs) sit at $12.56. The daily rifle chart has been downtrend ahead of an accelerated lower after its earnings report on slashed guidance. The daily 5-period MA resistance sits at $23.31 followed by the daily 15-period MA at $29.59. The daily lower BBs sit at $15.78. The daily stochastic formed a mini inverse pup through the 10-band and resting below the 5-band for a bounce or an even further drop on a mini inverse pup. Attractive pullback levels sit at $19.47, $17.78 fib, $15.85 fib, $13.64 fib, and the $11.06 fib.

The Outcome

Affirm CFO Michael Linford commented, “In light of the uncertain macroeconomic backdrop, we are approaching our next fiscal year prudently while maintaining our focus on driving responsible growth and continuing to invest in strengthening our leadership position. We continue to expect to achieve a sustained profitability run rate, on an adjusted operating income basis, by the end of fiscal 2023.” The Company sees the continued expansion, diversification, and scaling of active merchants to grow GMV is the key to outrunning the bad guys, aka inflation, rate hikes and recession. Time will tell in fiscal 2023 heading into the holiday season. Exit stage left.