Over the last six months, Booking’s shares have sunk to $172.95, producing a disappointing 19.1% loss - a stark contrast to the S&P 500’s 10.9% gain. This might have investors contemplating their next move.

Following the pullback, is now a good time to buy BKNG? Find out in our full research report, it’s free.

Why Does Booking Spark Debate?

Formerly known as The Priceline Group, Booking Holdings (NASDAQ: BKNG) is the world’s largest online travel agency.

Two Positive Attributes:

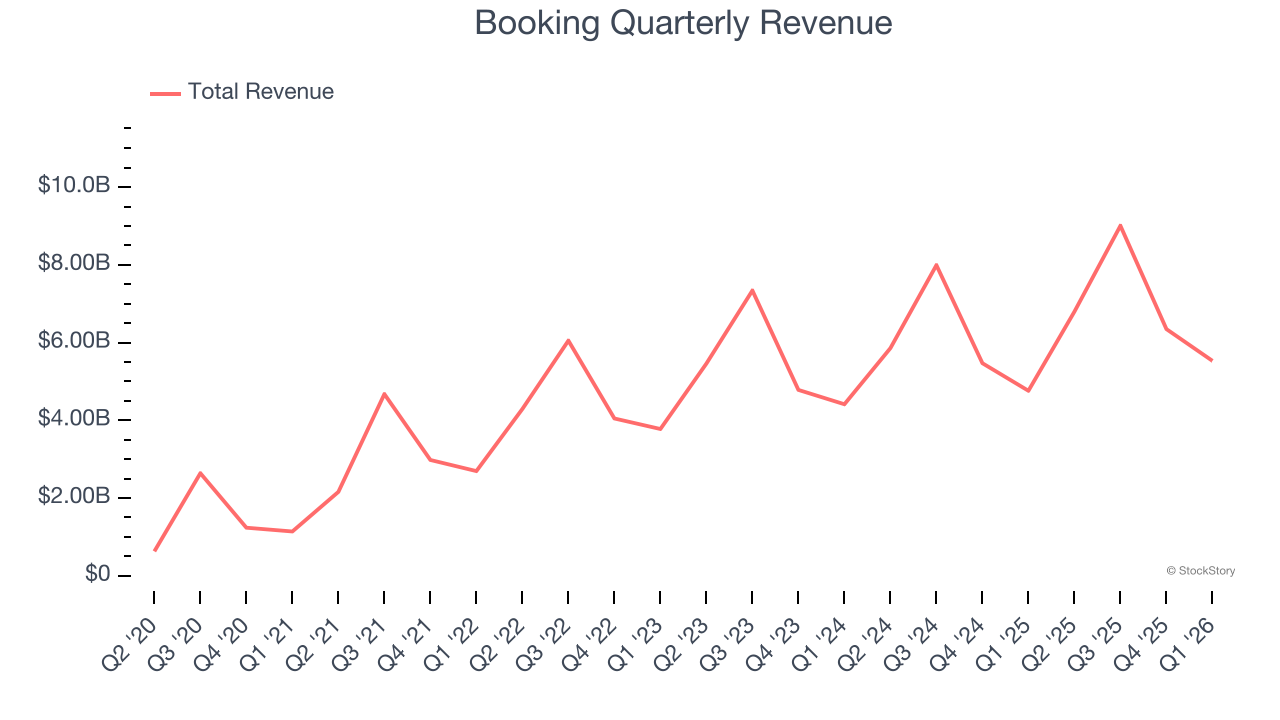

1. Long-Term Revenue Growth Shows Strong Momentum

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Booking’s sales grew at a solid 15.1% compounded annual growth rate over the last three years. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers.

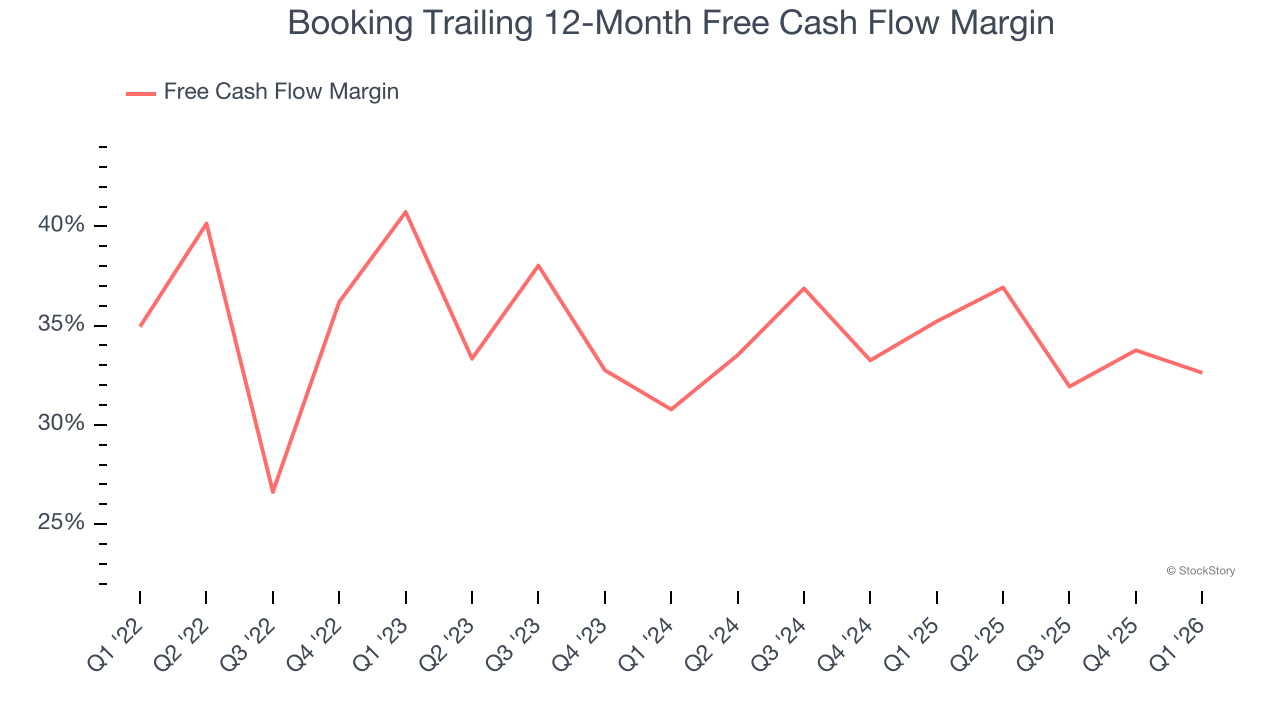

2. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Booking has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the consumer internet sector, averaging an eye-popping 33.8% over the last two years.

One Reason to Be Careful:

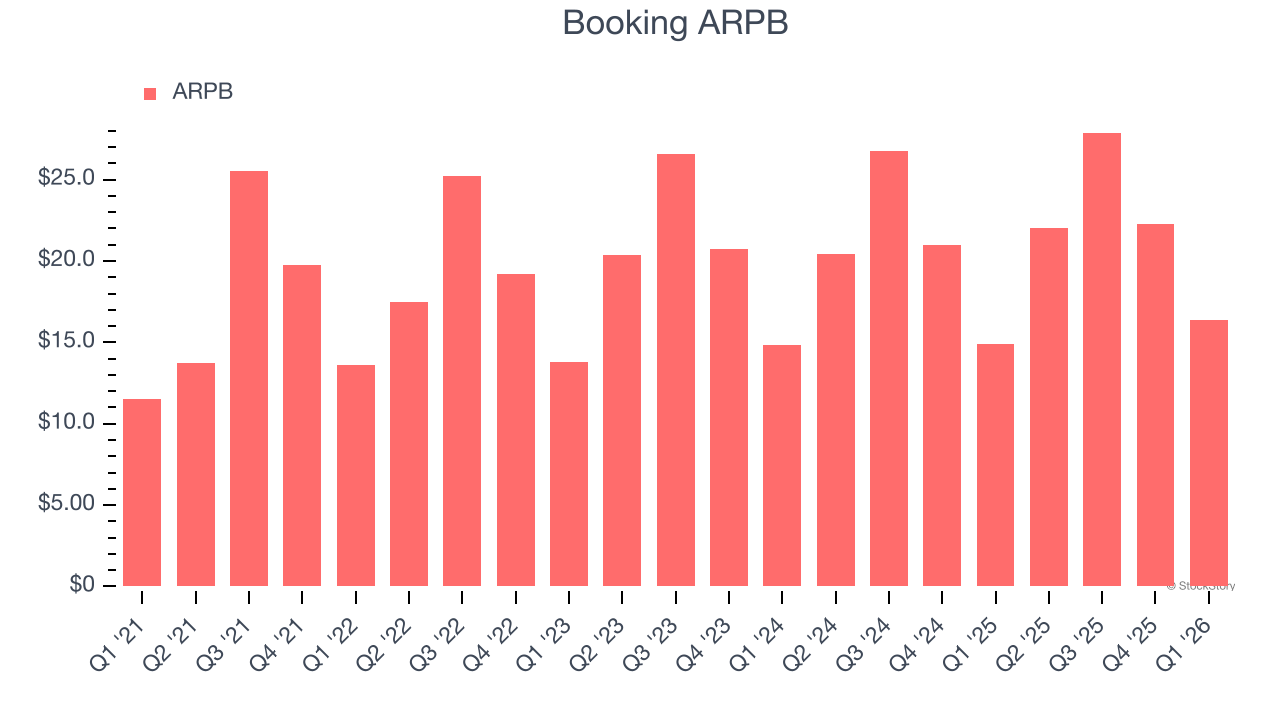

Growth in Customer Spending Lags Peers

Average revenue per booking (ARPB) is a critical metric to track because it not only measures how much users book on its platform but also the commission that Booking can charge.

Booking’s ARPB growth has been mediocre over the last two years, averaging 3.8%. This isn’t great, but the increase in room nights booked is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Booking tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether bookings can continue growing at the current pace.

Final Judgment

Booking’s merits more than compensate for its flaws. After the recent drawdown, the stock trades at 12.8× forward EV/EBITDA (or $172.95 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.