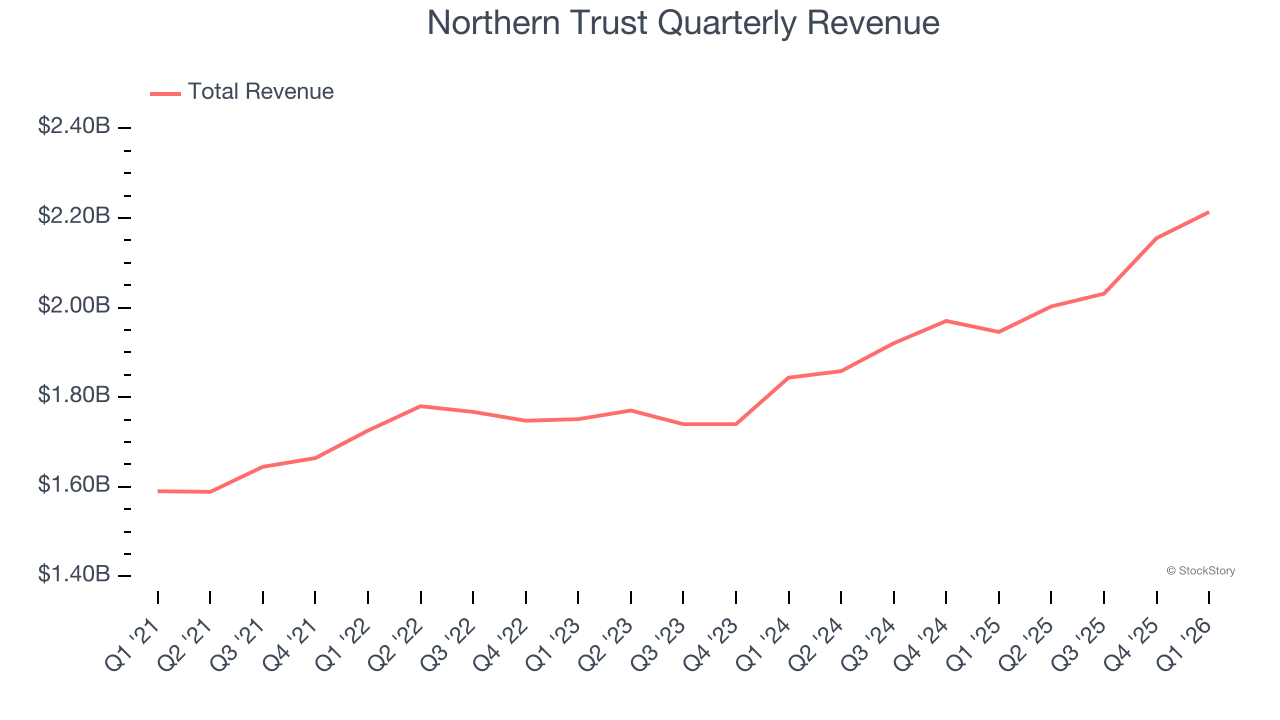

Financial services company Northern Trust (NASDAQ: NTRS) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 13.8% year on year to $2.21 billion. Its GAAP profit of $2.71 per share was 16.1% above analysts’ consensus estimates.

Is now the time to buy Northern Trust? Find out by accessing our full research report, it’s free.

Northern Trust (NTRS) Q1 CY2026 Highlights:

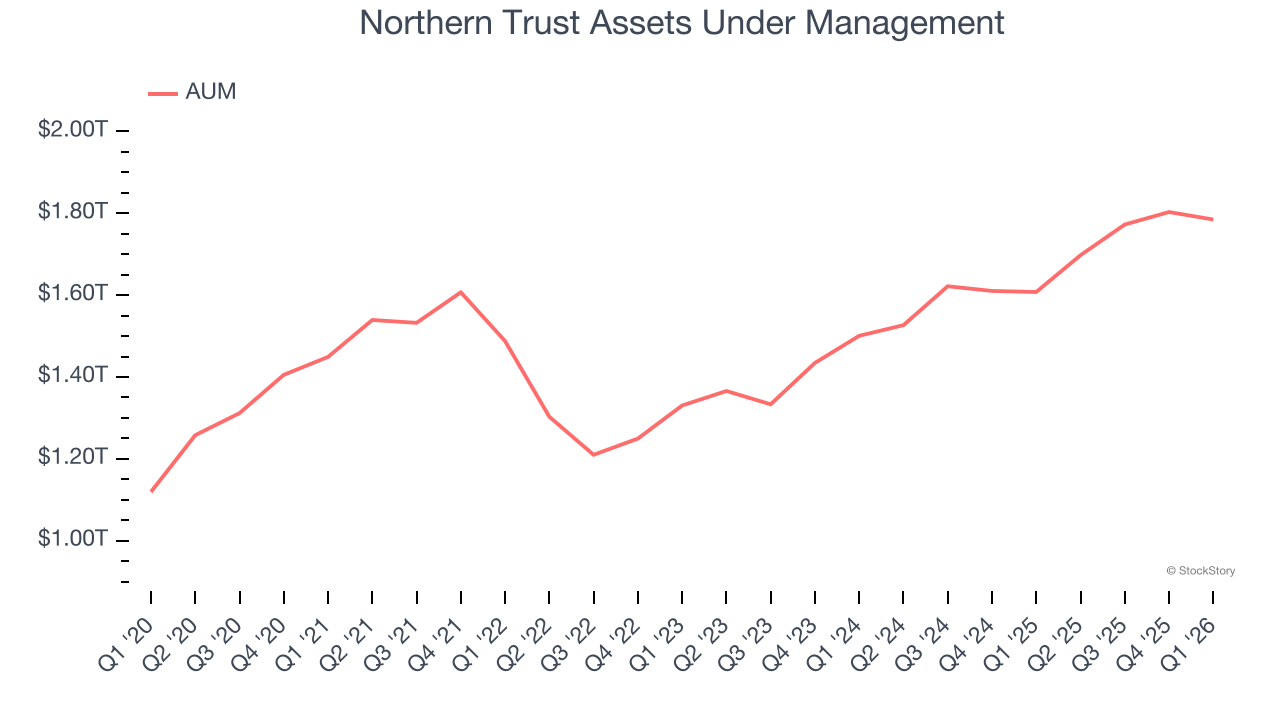

- Assets Under Management: $1.78 trillion vs analyst estimates of $1.82 trillion (11% year-on-year growth, 2.1% miss)

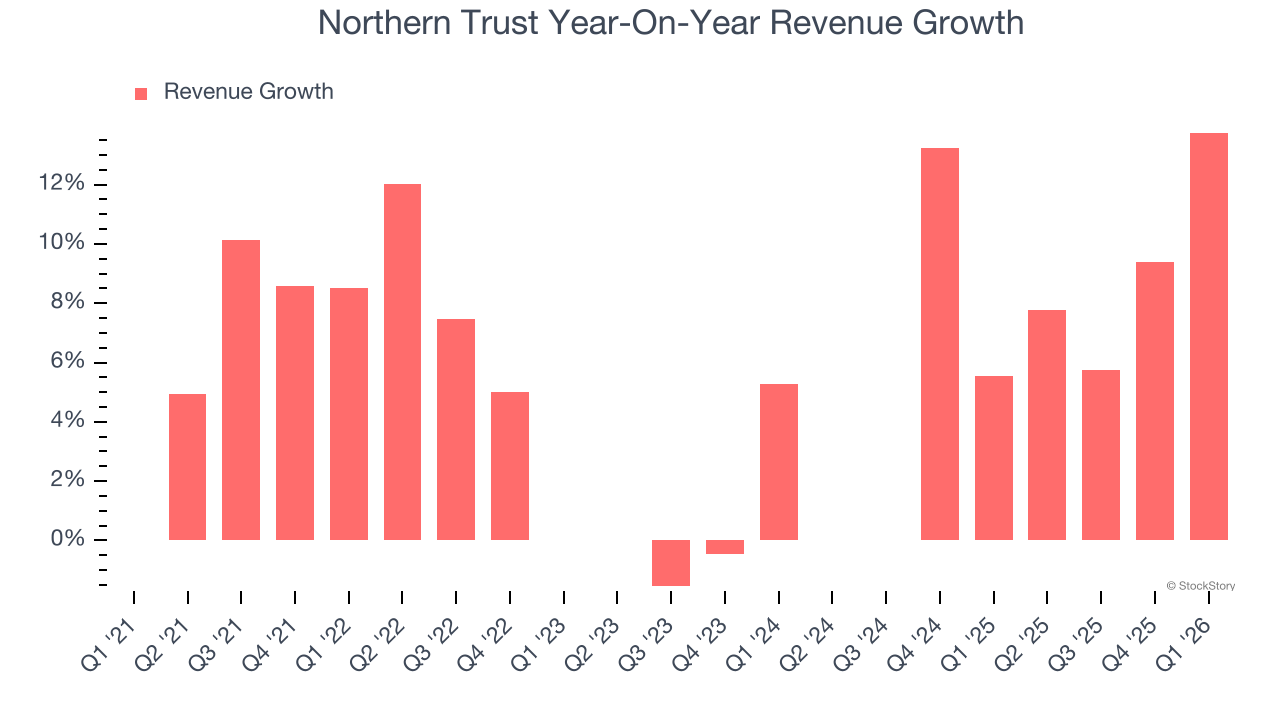

- Revenue: $2.21 billion vs analyst estimates of $2.13 billion (13.8% year-on-year growth, 4% beat)

- Pre-tax Profit: $708.2 million (32% margin)

- EPS (GAAP): $2.71 vs analyst estimates of $2.33 (16.1% beat)

- Market Capitalization: $29.46 billion

Company Overview

Founded in 1889 during Chicago's post-Great Fire rebuilding boom, Northern Trust (NASDAQ: NTRS) provides wealth management, asset servicing, and banking solutions to corporations, institutions, families, and high-net-worth individuals globally.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Northern Trust’s revenue grew at a mediocre 6.5% compounded annual growth rate over the last five years. This fell short of our benchmark for the financials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Northern Trust’s annualized revenue growth of 8.8% over the last two years is above its five-year trend, suggesting some bright spots.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Northern Trust reported year-on-year revenue growth of 13.8%, and its $2.21 billion of revenue exceeded Wall Street’s estimates by 4%.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Assets Under Management (AUM)

Assets Under Management (AUM) represents the total value of investments that a financial institution manages for its clients. These assets generate steady income through management fees, creating predictable revenue streams that remain stable so long as clients remain invested with the firm.

Northern Trust’s AUM has grown at an annual rate of 5.4% over the last five years, worse than the broader financials industry and slower than its total revenue. When analyzing Northern Trust’s AUM over the last two years, we can see that growth accelerated to 11.9% annually. Fundraising or short-term investment performance were net contributors for the company over this shorter period since assets grew faster than total revenue. Keep in mind that asset growth can be erratic and seasonal, so we don't rely on it too heavily for our business quality analysis.

In Q1, Northern Trust’s AUM was $1.78 trillion, falling 2.1% short of analysts’ expectations. This print was 11% higher than the same quarter last year.

Key Takeaways from Northern Trust’s Q1 Results

It was good to see Northern Trust beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its AUM missed. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 2.7% to $163.25 immediately after reporting.

Northern Trust put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).