Shareholders of Zevia would probably like to forget the past six months even happened. The stock dropped 47.3% and now trades at $1.25. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Zevia, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Zevia Not Exciting?

Even though the stock has become cheaper, we're cautious about Zevia. Here are three reasons you should be careful with ZVIA and a stock we'd rather own.

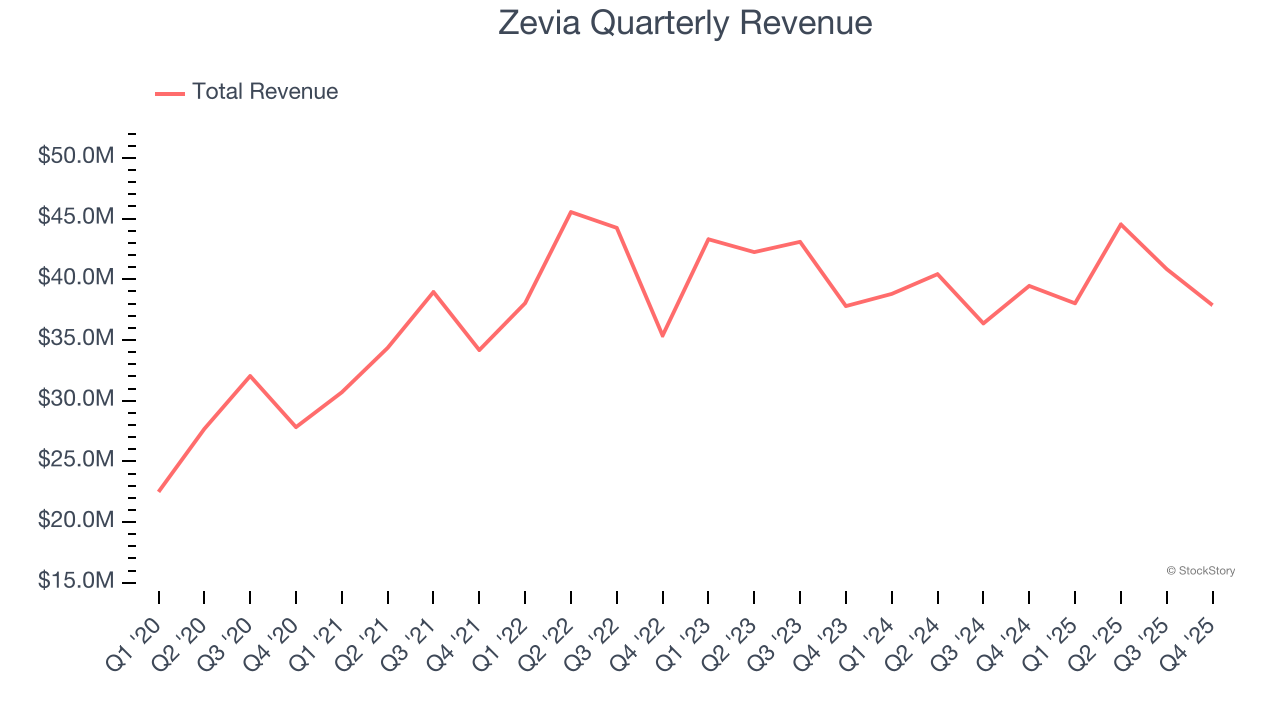

1. Long-Term Revenue Growth Flatter Than a Pancake

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Zevia struggled to consistently increase demand as its $161.3 million of sales for the trailing 12 months was close to its revenue three years ago. This wasn’t a great result and signals it’s a lower quality business.

2. Fewer Distribution Channels Limit its Ceiling

With $161.3 million in revenue over the past 12 months, Zevia is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

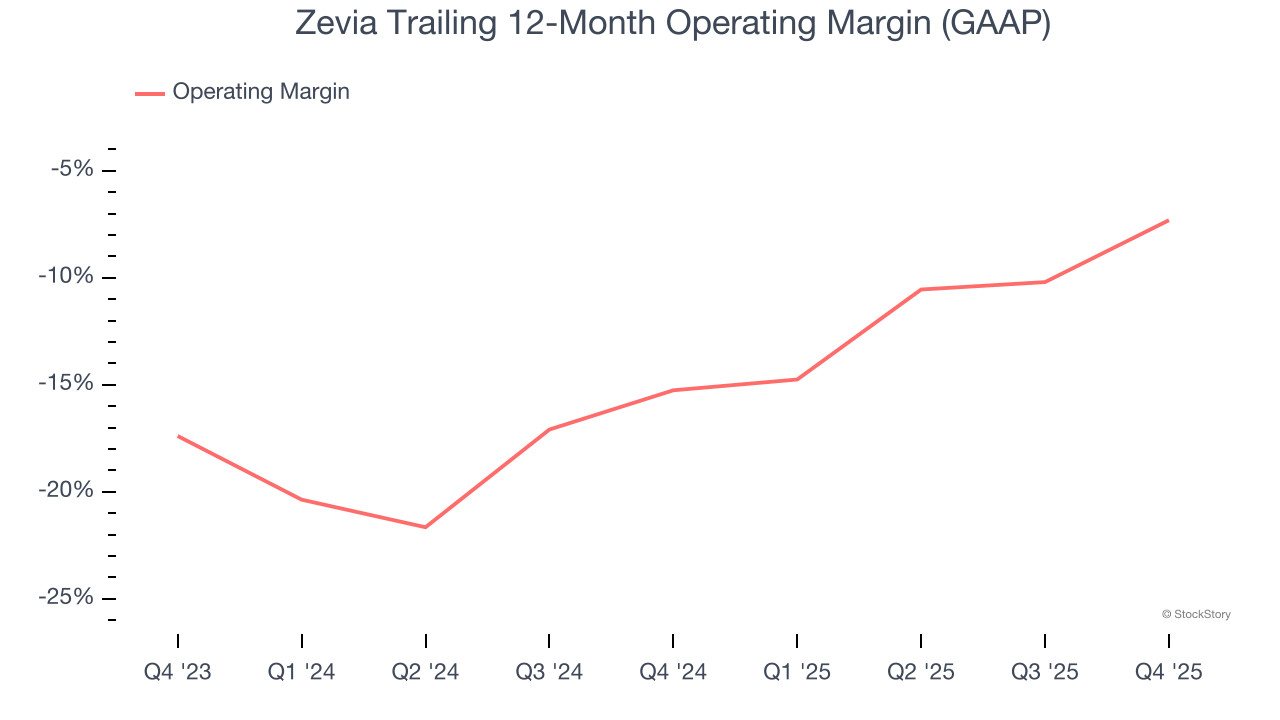

3. Operating Losses Sound the Alarms

Operating margin is an important measure of profitability accounting for key expenses such as marketing and advertising, IT systems, wages, and other administrative costs.

Unprofitable public companies are rare in the defensive consumer staples industry. Unfortunately, Zevia was one of them over the last two years as its high expenses contributed to an average operating margin of negative 11.2%.

Final Judgment

Zevia isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at $1.25 per share (or a forward price-to-sales ratio of 0.5×). The market typically values companies like Zevia based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy. Let us point you toward the most entrenched endpoint security platform on the market.

High-Quality Stocks for All Market Conditions

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.