Optical networking company Lumentum Holdings (LITE) is set to join the S&P 500 index ($SPX) on March 23, before the market opens. As quarterly rebalancings like this lead to short-term buying and selling, Lumentum’s stock gained 14.73% intraday on March 9, after the news was released on March 6.

The stock has skyrocketed, making it a pioneer of the artificial intelligence (AI) supply chain. The company’s optical networking equipment is in high demand, driving a significant surge in the stock over the past year.

This can also be seen in Lumentum's recent landing of a multiyear strategic agreement with chip industry leader NVIDIA Corporation (NVDA), which includes a multibillion-dollar purchase commitment and future access rights to advanced laser components. NVDA would also invest $2 billion in Lumentum to fund R&D, expand future capacity, and support operations as it develops U.S.-based manufacturing at a new facility.

Therefore, as Lumentum faces tailwinds, we look more deeply into the company at this juncture…

About Lumentum Stock

Lumentum Holdings Inc. is a leading designer and manufacturer of optical and photonic products that enable optical networking, laser applications, 3D sensing, and advanced manufacturing worldwide. Headquartered in San Jose, California, Lumentum drives innovation in cloud infrastructure and photonics. The company has a market capitalization of $45.75 billion.

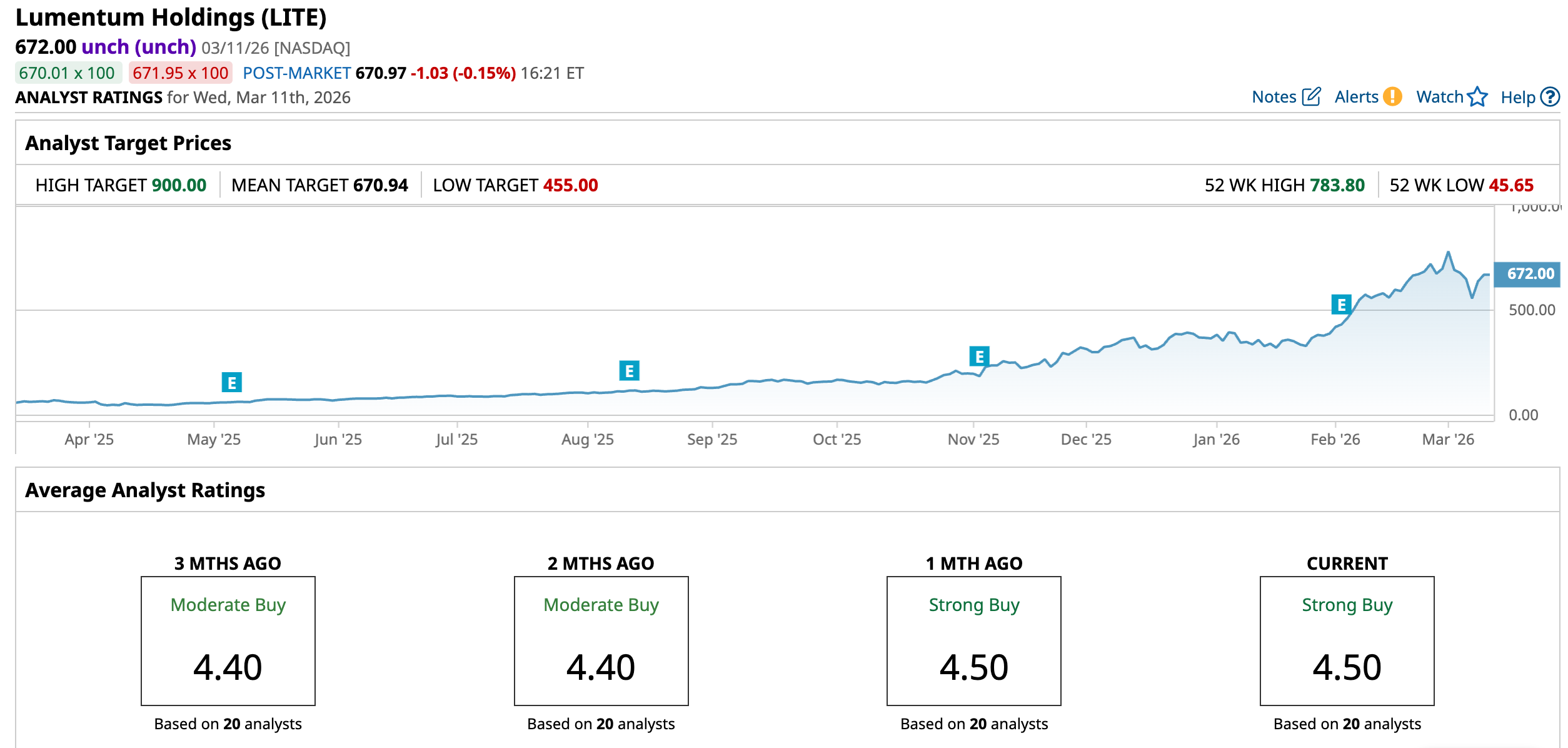

On the backs of explosive demand for its optical and photonic components in AI infrastructure and data centers, Lumentum’s stock has skyrocketed over the past year. Over the past 52 weeks, the stock has gained 976.83%, while it has been up 81.28% year-to-date (YTD). Just for comparison, the S&P 500 index is up 21.57% over the past 52 weeks and is down marginally YTD. The stock reached a 52-week high of $783.80 on March 2, but is down 14.3% from that level.

The hefty rise in stock price has also inflated Lumentum’s valuation. On a forward-adjusted basis, its price-to-earnings ratio of 88.44x is significantly higher than the industry average of 21.46x.

Lumentum’s Q2 Results Were Better Than Expected

For the second quarter of fiscal 2026 (quarter ended Dec. 27), Lumentum’s net revenue increased by 65.5% year-over-year (YOY) to $665.50 million, which is higher than the $653.40 million that Wall Street analysts had expected.

Non-GAAP gross margin grew from 32.3% to 42.5%, and non-GAAP operating margin grew by 1,730 basis points to 25.2%. Non-GAAP EPS increased significantly to $1.67, surpassing the $1.41 that analysts had expected.

Lumentum’s forward guidance assumes over 85% YOY revenue growth, although the company is only just at the starting line for optical circuit switches (OCS) and co-packaged optics (CPO). OCS has already driven a backlog well beyond $400 million and received a multi-hundred-million-dollar order in CPO.

Wall Street analysts expect the company’s EPS to climb by 706.7% YOY to $1.82 for Q3 FY2026. For fiscal 2026, EPS is projected to surge significantly to $5.90, followed by a 128.6% growth to $13.49 in the next fiscal year.

Here’s What Analysts Think About Lumentum Stock

Following Lumentum's purchase commitments from NVDA for high-power lasers, analysts at Needham raised the stock's price target from $550 to $850 while maintaining a “Buy” rating. According to Needham analysts, the purchase commitment might be incremental to a multi-hundred-million-dollar range of orders from the chip giant.

Citing insights from investor meetings with CEO Michael Hurlston and VP Investor Relations Kathy Ta, Stifel analysts maintained a “Buy” rating on the stock and raised the price target from $480 to $800. The firm noted that Lumentum's EML lasers have recently been qualified by Fabrinet, and that NVDA's latest performance in the networking segment signals strong medium-term growth potential for Lumentum.

Barclays analyst Tom O'Malley maintained an “Equal-Weight” rating while significantly raising the price target from $475 to $750, indicating renewed confidence in the company’s stock and future potential. Last month, Mizuho analyst Vijay Rakesh reiterated an “Outperform” rating for Lumentum’s stock and increased the price target from $525 to $645.

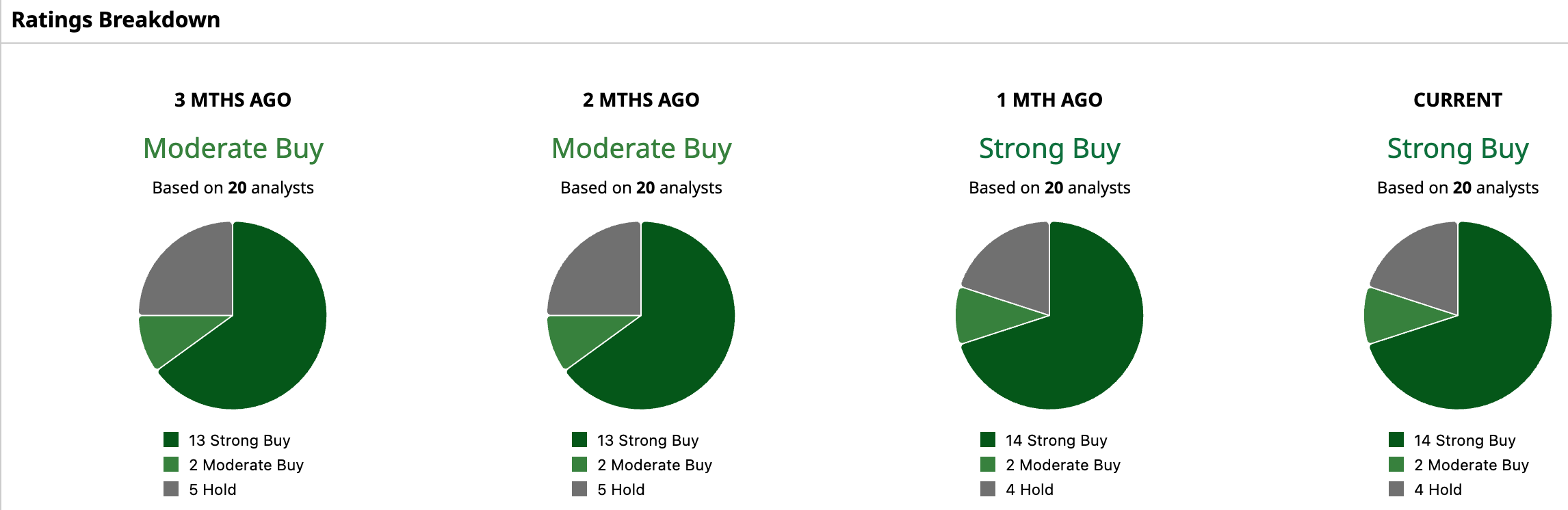

Lumentum has become a popular name on Wall Street, with analysts awarding it a consensus “Strong Buy” rating overall. Of the 20 analysts rating the stock, a majority of 14 analysts have given it a “Strong Buy” rating, two analysts rated it “Moderate Buy,” while four analysts are taking the middle-of-the-road approach with a “Hold” rating. Already passing the consensus price target of $670.94, LITE can grow 33.93% from the Street-high price target of $900.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Dear Lumentum Stock Fans, Mark Your Calendars for March 23

- Should Risk-Takers Roll the Dice on These 3 Penny Stocks at 52-Week Lows?

- As Archer Aviation Joins a DoT Pilot Program, Should You Buy, Sell, or Hold ACHR Stock?

- Analysts Are Still Betting That Oracle Stock Can Gain 150% Over the Next 12 Months. Should You Buy ORCL Here?