Atlanta, Georgia-based Delta Air Lines, Inc. (DAL) provides scheduled air transportation for passengers and cargo. With a market cap of $43.5 billion, the company offers flight status information, bookings, baggage handling, and other related services.

Shares of this global airline leader have outperformed the broader market over the past year. DAL has gained 57.5% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 28.3%. However, in 2026, DAL stock is down 4.5%, compared to the SPX’s 4.2% gains on a YTD basis.

Zooming in further, DAL’s outperformance looks more pronounced compared to the U.S. Global Jets ETF (JETS). The exchange-traded fund has gained about 26.2% over the past year. Moreover, the stock’s single-digit dip on a YTD basis outshines the ETF’s 11.2% losses over the same time frame.

Delta beat expectations on strong premium and loyalty demand, not just passenger volume. Premium fares grew about 14% YoY and loyalty revenue rose around 13%, showing pricing power and recurring brand value that help offset higher fuel costs. In addition, corporate and leisure demand stayed broad-based, with double-digit growth in premium cabins, the American Express Company’s (AXP) AmEx card portfolio, and Transatlantic/corporate routes. Furthermore, Delta is managing capacity, renewing its fleet, and adding routes like JFK to Orange County to capture higher fares.

On Apr. 8, DAL shares closed up by 3.8% after reporting its Q1 results. Its revenue stood at $14.2 billion, up 9.4% year over year. The company’s adjusted EPS of $0.64, grew 42.2% from the year-ago quarter.

For the current fiscal year, ending in December, analysts expect DAL’s EPS to decline 8.9% to $5.30 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

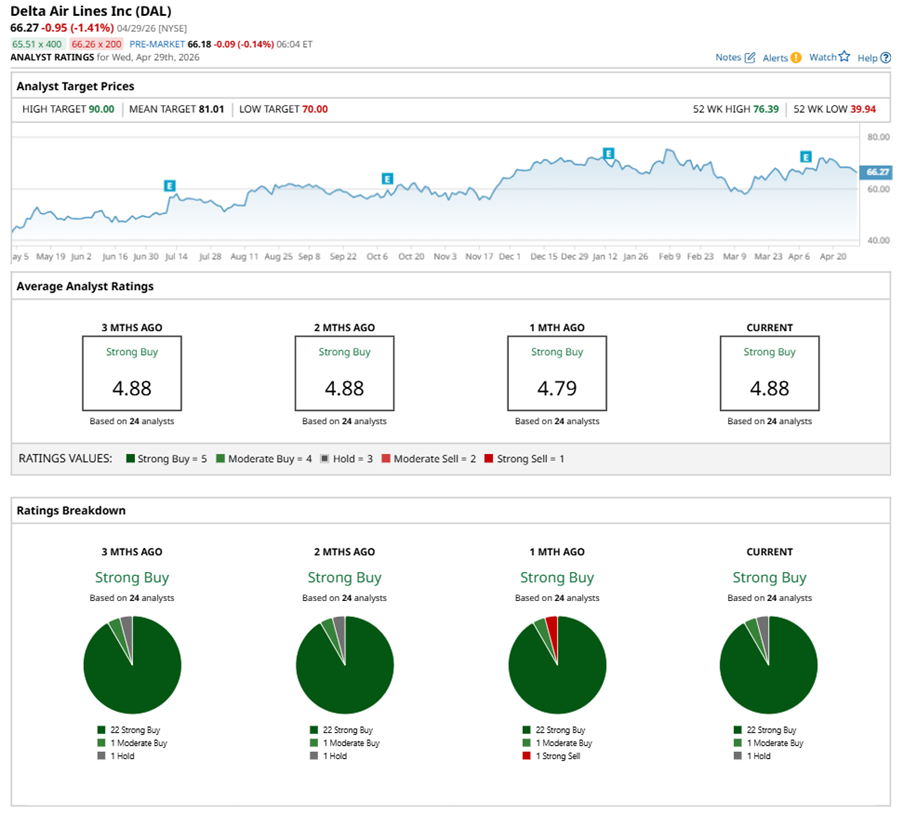

Among the 24 analysts covering DAL stock, the consensus is a “Strong Buy.” That’s based on 22 “Strong Buy” ratings, one “Moderate Buy,” and one “Hold.”

This configuration is less bearish than a month ago, with one analyst suggesting a “Strong Sell.”

On Apr. 17, Evercore ISI analyst Duane Pfennigwerth kept an “Outperform” rating on DAL and raised the price target to $85, implying a potential upside of 28.3% from current levels.

The mean price target of $81.01 represents a 22.2% premium to DAL’s current price levels. The Street-high price target of $90 suggests an ambitious upside potential of 35.8%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart