The Federal Reserve Board's October 2025 Discount Rate Meeting Minutes, released just weeks before the end of the year, have sent clear signals of a central bank navigating a complex economic landscape. The minutes reveal a unanimous decision to lower the primary credit rate and a second consecutive cut to the federal funds rate, indicating a continued, albeit cautious, effort to support economic activity. Crucially, the Fed also announced the impending conclusion of its balance sheet reduction program, known as quantitative tightening, by December 1, 2025, marking a significant pivot in its post-pandemic monetary policy.

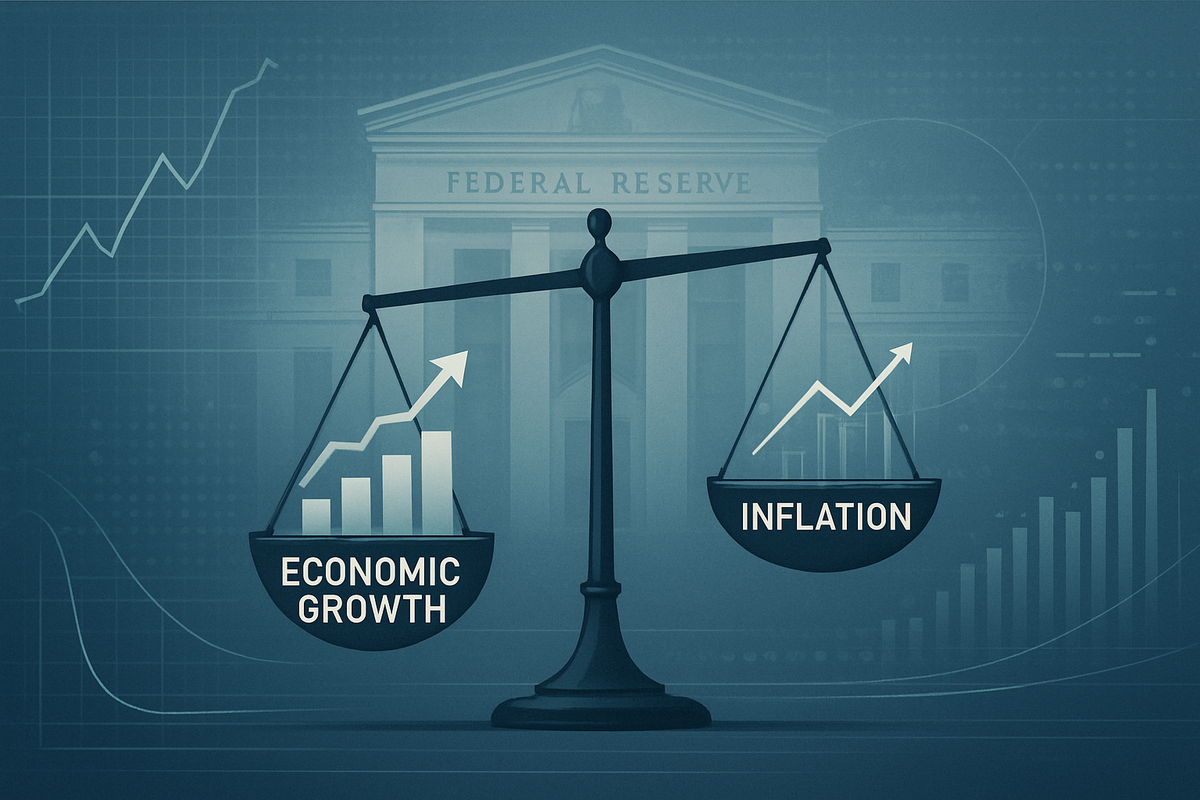

These decisions come amidst an improved GDP forecast but persistent inflation concerns and a softening labor market. While the immediate implication for borrowers is slightly lower interest rates, the overarching message from the Fed, particularly from Chair Jerome Powell, suggests a data-dependent approach with a "hawkish" lean against aggressive future rate cuts, pushing back against market expectations for further easing in December. This nuanced stance creates a delicate balance for markets, which are now grappling with the implications of reduced quantitative tightening alongside a more cautious approach to further rate reductions.

Fed's Double-Edged Sword: Rate Cuts and Quantitative Tightening's End Define October 2025

The October 28-29, 2025, Federal Open Market Committee (FOMC) meeting culminated in a 25-basis-point reduction in the federal funds rate, establishing a new target range of 3.75%-4.00%. This followed a similar cut in September, signaling the Fed's intent to provide further accommodation to the economy. Concurrently, the Federal Reserve Board of Governors, acting on recommendations from various regional Federal Reserve Banks, unanimously voted to decrease the primary credit rate (the discount rate) by 1/4 percentage point to 4.0 percent, effective October 30, 2025. These moves reflect the Fed's assessment of increasing downside risks to employment and a desire to ensure economic expansion continues at a moderate pace.

A pivotal announcement from the minutes was the decision to cease the reduction of the Fed's aggregate securities holdings on December 1, 2025. This move, which effectively ends the quantitative tightening program, aims to stabilize the size of the Fed's balance sheet, a policy tool that has significantly influenced market liquidity and long-term interest rates since its inception. The timeline leading up to this moment has seen the Fed gradually unwind its massive balance sheet built during and after the pandemic, making this cessation a landmark shift towards a more stable monetary base.

Key players involved in these decisions include the Federal Reserve Board of Governors, the twelve regional Federal Reserve Banks, and the members of the FOMC, led by Chair Jerome Powell. While the rate cuts provided some relief, Chair Powell adopted a notably "hawkish" tone in his post-meeting press conference, tempering market expectations for an almost certain December rate cut. This created initial ripples in the financial markets, with some short-term bond yields adjusting as traders recalibrated their expectations for future policy. The divergent views among FOMC participants on the appropriateness of a December cut further underscored the internal debate and the data-dependent nature of future policy.

Despite an upgraded full-year 2025 GDP growth forecast from 1.0% to 1.5% and an expected rebound to 1.8% in 2026, concerns about inflation remained elevated, with the Consumer Price Index (CPI) rising to 3% for the 12 months ending September 2025. The labor market also presented a mixed picture, with slowing job gains and an edging up of the unemployment rate, though it remained low. A federal government shutdown further complicated the assessment by delaying the release of official government data, creating "low visibility" for some key indicators and adding another layer of uncertainty to the economic outlook.

Market Movers: Who Wins and Who Loses from the Fed's Latest Moves

The Federal Reserve's recent decisions are set to create distinct winners and losers across various sectors of the financial market, reflecting the interplay of interest rates, inflation, and economic growth prospects. Companies that are highly sensitive to borrowing costs and consumer spending are likely to see the most immediate impacts.

Potential Winners:

- Housing and Real Estate: Lower interest rates, even marginally, tend to stimulate demand in the housing market. Companies like D.R. Horton (NYSE: DHI) and Lennar Corporation (NYSE: LEN), major homebuilders, could benefit from increased affordability for prospective homebuyers, potentially boosting sales and order backlogs. Real estate investment trusts (REITs) like Prologis (NYSE: PLG), focused on logistics, may also see improved financing conditions for expansion and acquisitions.

- Consumer Discretionary: With potentially lower borrowing costs for consumers and a somewhat improved economic outlook, sectors tied to discretionary spending could see a boost. Retailers such as Amazon (NASDAQ: AMZN) and Target (NYSE: TGT) might experience higher sales volumes as consumers feel more confident to spend. Companies in the automotive sector, like General Motors (NYSE: GM), could also benefit from lower financing costs for vehicle purchases.

- Growth Stocks and Technology: Growth-oriented companies, particularly in the technology sector, often thrive in lower interest rate environments as their future earnings are discounted at a lower rate, increasing their present value. Tech giants like Microsoft (NASDAQ: MSFT) and Apple (NASDAQ: AAPL), which often rely on innovation and long-term projects, could find their valuations supported by these conditions.

- Companies with High Debt Loads: Businesses that carry significant debt could see their interest expenses decrease as existing variable-rate loans adjust or as they refinance at more favorable fixed rates. This could improve profitability and cash flow, particularly for highly leveraged firms across various industries.

Potential Losers/Those Facing Headwinds:

- Banks and Financial Institutions: While lower rates can stimulate lending, a sustained period of declining rates can compress net interest margins (NIMs), the difference between what banks earn on loans and pay on deposits. Major banks like JPMorgan Chase (NYSE: JPM) and Bank of America (NYSE: BAC) might face challenges in maintaining profitability if NIMs continue to shrink. However, the end of quantitative tightening could provide some stability to bond markets, which might mitigate some negative impacts.

- Companies Sensitive to Inflation: Despite the rate cuts, inflation remains elevated. Companies that cannot easily pass on rising input costs to consumers could see their profit margins squeezed. Sectors reliant on commodities or with high labor costs, if wage inflation persists, could face headwinds.

- Yield-Sensitive Investments: While not a "company" in the traditional sense, investors seeking high yields from fixed-income instruments might find returns compressed in a lower interest rate environment, pushing them into riskier assets.

The Fed's "hawkish" pushback against further immediate rate cuts suggests that while the current environment is more accommodative, the path to significantly lower rates is not guaranteed, requiring companies to remain agile in their financial planning and operational strategies.

Wider Significance: A Delicate Dance Between Growth and Inflation

The Federal Reserve's October 2025 decisions hold broader significance, fitting into the ongoing narrative of central banks worldwide attempting to engineer a "soft landing" – bringing inflation down without triggering a severe recession. The cessation of quantitative tightening (QT) on December 1, 2025, marks a major inflection point. Since its aggressive expansion during the pandemic, the Fed's balance sheet has been a dominant force in financial markets. Ending QT signals a move towards a more stable, albeit still large, balance sheet, which could reduce volatility in bond markets and provide greater clarity on the availability of reserves within the banking system. This move could also alleviate some of the upward pressure on long-term interest rates that QT inherently created.

The ripple effects of these decisions will be felt across competitors and partners. For instance, international central banks, particularly those in developed economies, often monitor the Fed's actions closely. A more stable U.S. monetary policy, even if cautious, could provide a degree of predictability for global financial markets. However, if the Fed's fight against inflation proves more challenging, it could lead to renewed currency volatility and capital outflows from emerging markets. Domestically, the improved GDP forecast, coupled with rate cuts, could encourage business investment, benefiting suppliers and partners across various industries.

Regulatory and policy implications are also noteworthy. The Fed's continued focus on data-dependency, particularly regarding inflation and employment, underscores the flexibility embedded in its current policy framework. This approach means that future decisions will be heavily influenced by incoming economic data, potentially leading to quicker shifts in policy direction than previously observed. The "low visibility" due to the federal government shutdown impacting labor data highlights a systemic vulnerability that could influence future policy decisions if similar disruptions occur. Regulators will be keenly watching how banks manage their balance sheets and lending practices in an environment where the Fed is no longer actively shrinking its holdings.

Historically, periods of monetary policy transition, such as the end of quantitative easing or tightening cycles, have often been accompanied by increased market volatility. While the current situation isn't a complete reversal, the shift from active balance sheet reduction to stabilization is a significant one. Comparing this to past cycles, such as the tapering tantrum of 2013 or the initial phases of QT in 2017, the Fed appears to be attempting a more gradual and communicative approach to minimize market disruption. However, the persistent inflation, even with rate cuts, presents a unique challenge not seen in previous easing cycles, making historical precedents only partially applicable. The balancing act between supporting growth and taming inflation remains the central theme, with the Fed seemingly prioritizing a cautious approach to avoid reigniting inflationary pressures.

What Comes Next: Navigating Uncertainty and Strategic Pivots

Looking ahead, the Federal Reserve's October 2025 minutes lay the groundwork for a period defined by cautious optimism and heightened data dependency. In the short term, markets will closely scrutinize upcoming economic reports, particularly those on inflation, employment, and consumer spending, for any signs that might sway the Fed towards or away from further rate adjustments. The "sharply divergent views" among FOMC participants regarding a December rate cut suggest that any future moves will likely be met with considerable debate, indicating a potential for increased market volatility around Fed announcements. Companies and investors should prepare for a period where economic data releases will have an outsized impact on market sentiment and asset prices.

In the long term, the cessation of quantitative tightening (QT) on December 1, 2025, signals a shift towards a more stable, albeit still substantial, Federal Reserve balance sheet. This could lead to more predictable liquidity conditions in the financial system, potentially reducing some of the upward pressure on long-term interest rates that QT exerted. However, the fight against elevated inflation (CPI at 3% in September 2025) remains a critical challenge. If inflation proves more stubborn than anticipated, the Fed might be forced to reconsider its current cautious stance on rate cuts, potentially leading to a more restrictive monetary policy later in 2026. Conversely, a significant deterioration in the labor market or a sharper-than-expected economic slowdown could prompt the Fed to accelerate its easing cycle.

Potential strategic pivots for businesses include re-evaluating capital expenditure plans in light of potentially more stable, though not necessarily much lower, borrowing costs. Companies in interest-rate-sensitive sectors, such as real estate and automotive, may need to adapt their sales and marketing strategies to reflect the nuanced interest rate environment. Market opportunities may emerge in sectors that can demonstrate resilience to inflation or those that benefit from sustained, moderate economic growth. For instance, businesses with strong pricing power or efficient supply chains could outperform. Challenges include navigating persistent inflationary pressures and the ongoing uncertainty surrounding the global economic outlook, which could impact consumer and business confidence.

Several potential scenarios could unfold. In an "optimistic soft landing" scenario, inflation gradually recedes towards the Fed's 2% target without a significant economic downturn, allowing the Fed to maintain a stable policy or even implement further gradual rate cuts. A "stagflationary" scenario could see inflation remaining elevated while economic growth falters, forcing the Fed into a difficult choice between supporting growth and fighting inflation. Finally, a "recessionary" scenario, triggered by unforeseen shocks or an overly restrictive policy, would likely lead to more aggressive rate cuts and potentially a resumption of quantitative easing. The Fed's commitment to data dependency means that the actual path taken will be a dynamic response to evolving economic conditions.

Wrap-Up: A Cautious Horizon for Markets and Investors

The Federal Reserve's October 2025 Discount Rate Meeting Minutes underscore a central bank treading a careful path, attempting to balance the imperatives of fostering economic growth with the persistent challenge of elevated inflation. The key takeaways are clear: a second consecutive interest rate cut signals continued support for the economy, while the impending end of quantitative tightening by December 1, 2025, marks a significant shift towards balance sheet stabilization. However, Chair Powell's "hawkish" stance against immediate further rate cuts, despite market expectations, injects a note of caution, emphasizing a data-dependent approach for future policy adjustments.

Moving forward, the market will be characterized by a heightened sensitivity to economic data, particularly inflation and employment figures. The improved GDP forecast offers some optimism, but the sustained 3% CPI in September 2025 highlights that the battle against inflation is far from over. This delicate balance means that investors should anticipate continued volatility and a nuanced policy response from the Fed. Companies that can demonstrate agility in managing costs, adapting to evolving consumer demand, and maintaining strong balance sheets are likely to be best positioned to navigate this environment.

The lasting impact of these decisions will hinge on the Fed's ability to successfully guide the economy towards its 2% inflation target without triggering a significant downturn. The end of quantitative tightening is a landmark event, signaling a return to a more conventional monetary policy framework, but the path ahead is fraught with challenges. What investors should watch for in the coming months are not just the headline inflation and employment numbers, but also the Fed's commentary for any shifts in tone or forward guidance, as these will be critical in deciphering the future direction of monetary policy and its implications for asset markets.

This content is intended for informational purposes only and is not financial advice